Oil prices in 2022 have steepened in their ascent, hitting $89/b in intra-day trading, up by $20/b from the start of December. The increase of nearly 30% is remarkable considering that it has materialised in around seven weeks.

Most commentators discuss two main drivers behind this:

- Strong demand recovery, or at the very least much healthier demand than expected at the start of the Omicron wave;

- Growing concerns about OPEC+ spare capacity and the group’s ability to match demand later in the year

We raised the latter issue regularly in our client reports in recent weeks and also in a well-noted blog more than two months ago. Both points are surely valid, but our real-time market analytics also points to a (continued) supply shortfall right now.

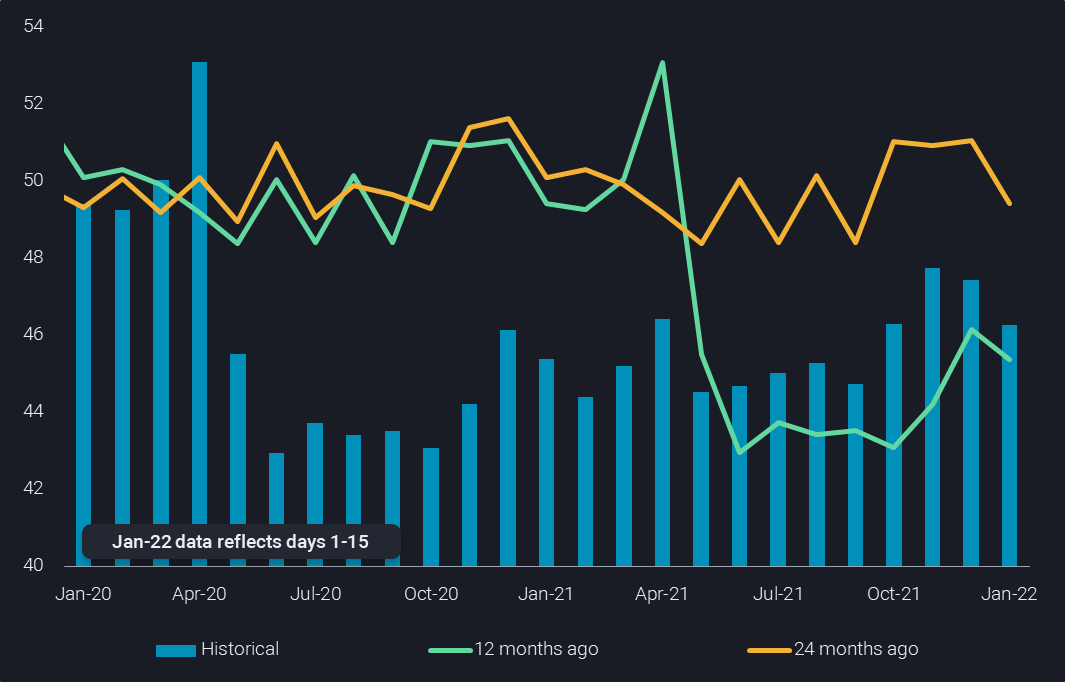

World crude oil liftings (including intra-country flows) (mbd)

OPEC+ increases are simply not enough

Global crude loadings surged in Q4 2021 vs the previous quarter, and December recorded departures of close to 47.5mbd, including intra-country flows (see chart). However, relative to H1 2021, this was an increase of just 2.3mbd. Over the same time span, we observed a combined increase of 2.4mbd in crude exports from the top five OPEC+ contributors (Iraq, Kuwait, Russia, Saudi Arabia, UAE), while OPEC reported an increase of production of 2.7mbd for these five countries. In other words, the rest of the world’s crude exports declined (at least in terms of seaborne supplies), despite sizable increases from the US.

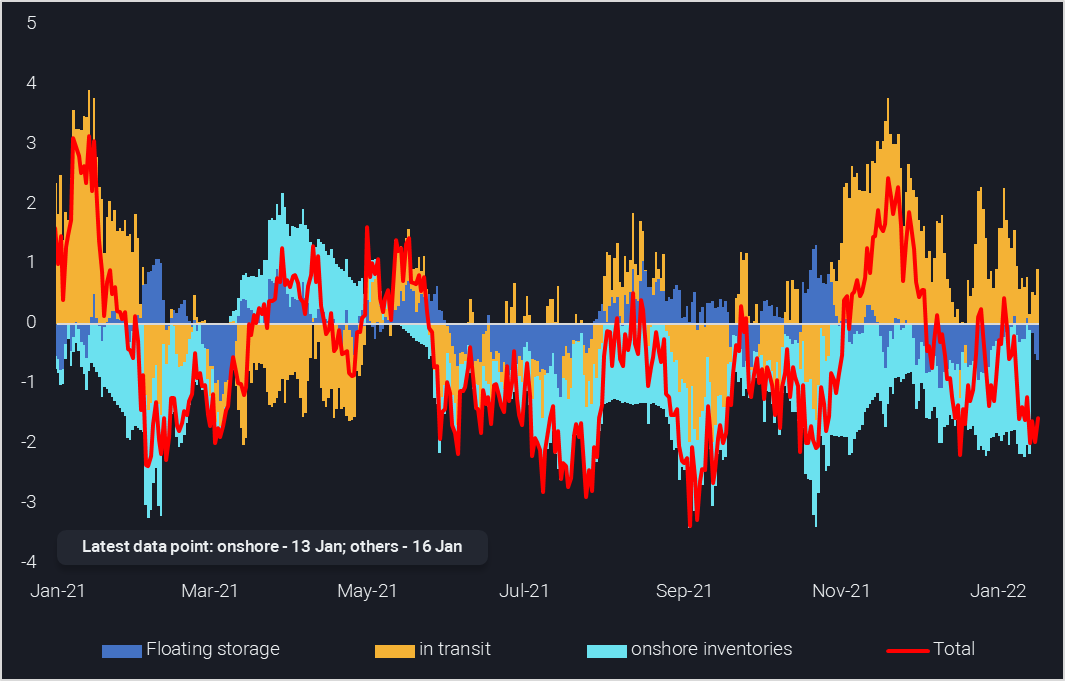

Our freshly released onshore crude inventory data shows that the market has been consistently undersupplied, as evidenced by persistent stockdraws ever since May last year, at an average rate of 1.15mbd. And despite the efforts made by OPEC+ to boost supplies, the shortfall rose further in Q4 2021 to around 1.6mbd.

Floating storage has been drawn by a further 170kbd over Q4 2021, as China finally unloaded previously booked cargoes. Only the oil in transit measure saw sizable builds over the previous quarter, reflecting the step higher in OPEC+ exports and rising US exports – the latter including long-haul supplies to Asia. But this trend is now also coming to an end.

World crude inventory change for onshore stocks, floating storage, crude in transit (4-week avg, mbd)

World crude oil liftings on track for 3-month low in January

Another concerning observation is that global crude liftings are set for a marked decline in January, having already fallen m-o-m in December. In the first half of January, we see loadings falling back to 46.3mbd, the same level as in October. The y-o-y growth across the Dec 21 to Jan 22 period is coming down to a meagre 1.1mbd, only half of the level observed in the previous six months. At the same time, the gap to pre-Covid levels remains wide: in Nov-Jan, crude oil loadings were 3.3mbd below the levels seen two years earlier, and not much of an improvement from the 4mbd y-o-y shortfall observed over Q2 and Q3 last year.

Outlook remains rather bullish

Apart from the big-ticket items of rising oil prices, falling crude liftings and drawing stocks, there are a number of further observations underpinning the perception of increasingly tight markets. These include, among others:

- Rising spot crude differentials for Atlantic Basin sweet crudes and Urals (Argus Media)

- Widening backwardation over recent weeks

- Solid refinery margins with further upside amid low product inventories

- The end to long standing difficulties (seen over autumn 2021) in placing Forties barrels

- Iran onshore crude inventories falling by an average of 150kbd over the last three months, suggesting that the strong export demand is tapping into stored barrels rather than fresh production, somewhat questioning any significant upside in short term exports in case sanctions are relaxed

With all of the above, plus increased sensitivity to outages – Kazakhstan, Libya, Botas pipeline issues to name just a few – and barely any additional downside to Chinese crude imports, the call on OPEC+ to add even more barrels will be strong in the coming weeks and months. The group’s success may only moderate the further upside to oil prices, as the lack of spare capacity appears to be set in stone as a market feature for 2022.

More from Vortexa Analysis

- Jan 18, 2022: Global diesel market pricing in tighter supplies ahead

- Jan 13, 2022: Omicron: pre-emptive supply cuts & resilient demand draw stocks and lift prices

- Jan 12, 2022: Mediterranean light crude: volumes limited and sold locally, weighing on freight demand

- Jan 11, 2022: China sets tone for refiners with tight oil quotas in the new year

- Jan 6, 2022: Global crude exports end 2021 on a high

- Dec 31, 2021: Making Waves: Looking back at a year of Freight

- Dec 22, 2021: Omicron infiltrates tankers in the Atlantic basin

- Dec 21, 2021: Asian refiners find silver linings amidst an ominous Omicron outlook

- Dec 16, 2021: Volatile global flows and hydrogen economics leave Europe short in naphtha

- Dec 14, 2021: 2022: The Freight Forecast

- Dec 9, 2021: Big oil producers shine as refiners