Without question, Omicron is a game-changer. The Covid variant spreads extremely fast, forcing change in responses along all parts of the system. Ultimately, experts appear to agree that Omicron marks the transition from a pandemic to an endemic disease (like influenza), and some governments have started to adopt this view. But in no way does this mean the next couple of months will be easy, especially not for constantly exhausted healthcare workers. In this insight piece we share our broader views but quickly move onto the repercussions on oil demand, supply, stocks and prices.

Big-picture Omicron impact assessment

The initial assessment on Omicron was that the speed of transmissions and the ability of reinfections and breakthrough infections would overpower the relative benefit of reduced severity in individual cases. Observations from the countries hit early on, South Africa, Denmark, Norway and the UK, suggest that the lower severity is the decisive feature of Omicron. As we learn more, what is tilting the balance the other way is now a type of ‘triple feature’ in lower severity for Omicron: 1) lower hospitalisation relative to infection rates; 2) fewer hospitalisation cases passed onto ICU care; 3) within ICU care, much less artificial ventilation is needed. Evidently, the hospitalisation periods are getting shorter and much less people are dying, as a result.

However, we are still in the very early stages of Omicron waves from a global perspective. And it is important to remember hospitalisations numbers come with a sizable lag. This is especially the case for countries that have so far kept infection levels low and have furthermore limited shelter from the vaccination side – either because people refuse to get vaccinated or the vaccines used are sub-par. Germany and China, among others, are falling into this category. In conclusion, there are some good reasons for the relatively optimistic views on the repercussions of Omicron (e.g. as laid out by OPEC), but hiccups and setbacks may pop up down the road.

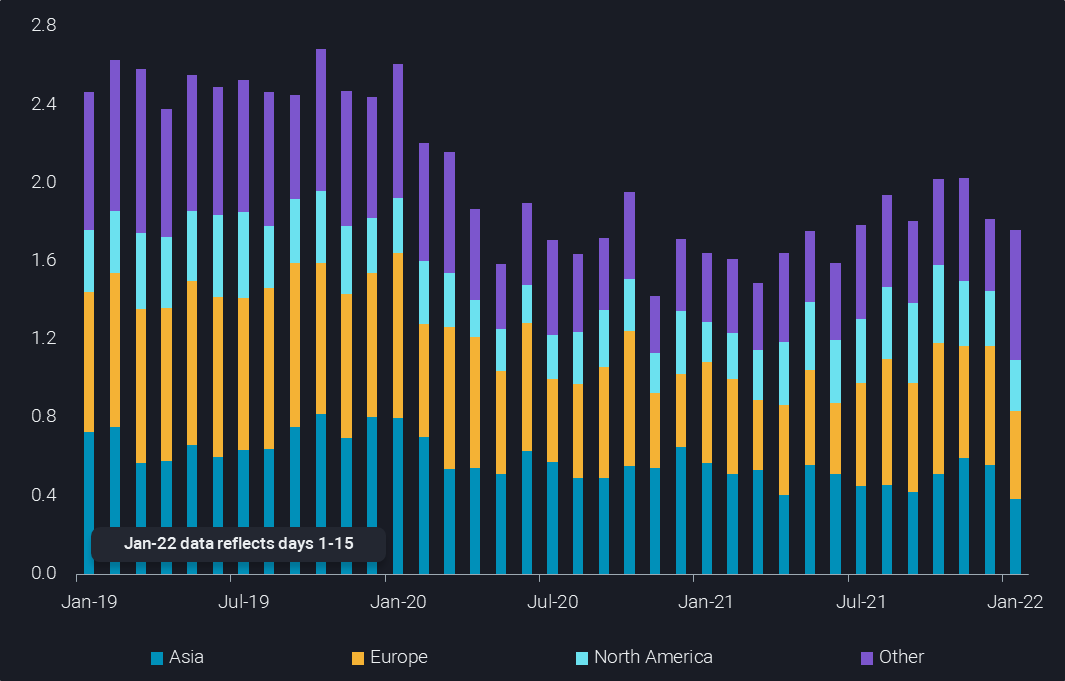

Global jet/kero arrivals by destination region (incl. Intra-country flows, mbd)

A very rough guide on oil demand repercussions from Omicron so far is that road fuels may partially benefit from renewed social distancing leading to more individual transport, while other fuels continue to benefit somewhat from high gas and electricity prices, albeit not to the extent expected previously. What is pretty clear is that jet fuel consumption is going down, as governments’ restrictions are hitting cross-border traffic over intra-national mobility.

Pre-emptive supply cuts may be happening

We may very well arrive at a situation, where oil demand is not as curtailed as was expected by the more cautious market watchers. But these expectations are very important, because they are set to lead to action. It is pretty intriguing that global jet/kero cracks and regrades appear to be moving from strength to strength at a time demand and imports are in decline (see chart). The possible explanation: refiners anticipated a strong jet fuel demand decline and shifted yields into the diesel and naphtha pools, making use of practices established in earlier Covid phases.

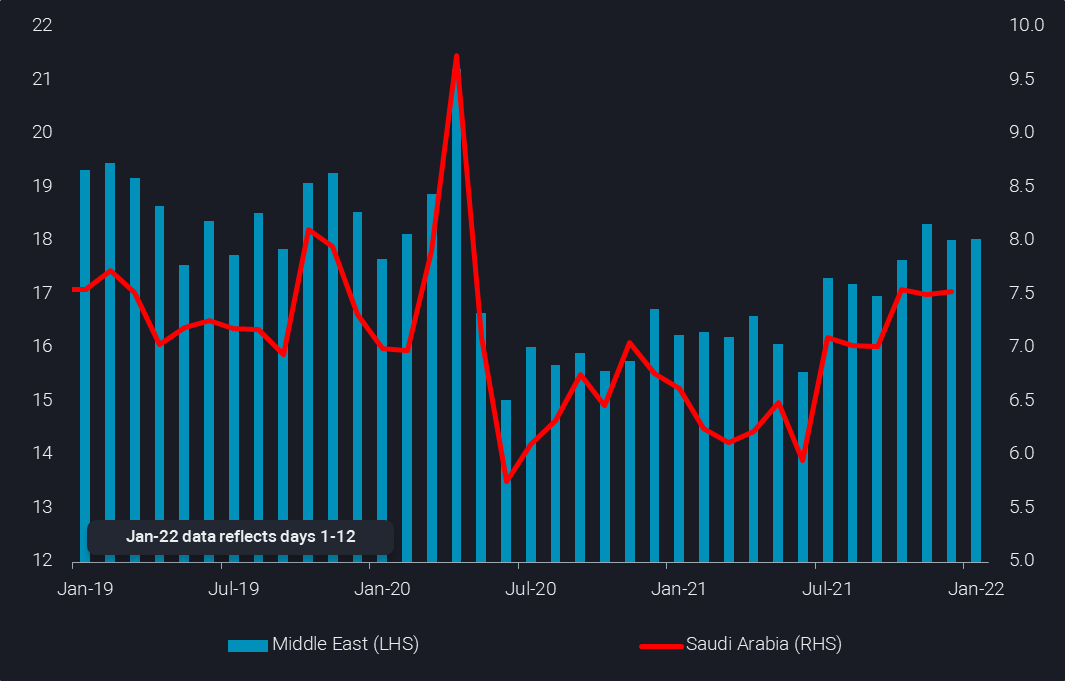

Crude/condensate loadings from the Middle East (incl. Intra-country flows, mbd)

Moving onto the oil supply side, there is only one region in the world that may be prepared to cut back supplies without wider OPEC+ arrangements – the Middle East. In fact, our data for liftings (incl. Intra-country flows) shows lower volumes in December, down by about 300kbd m-o-m, and stagnation in early January (see chart). What also stands out is that Saudi liftings have been slightly down in November and December, relative to the October level.

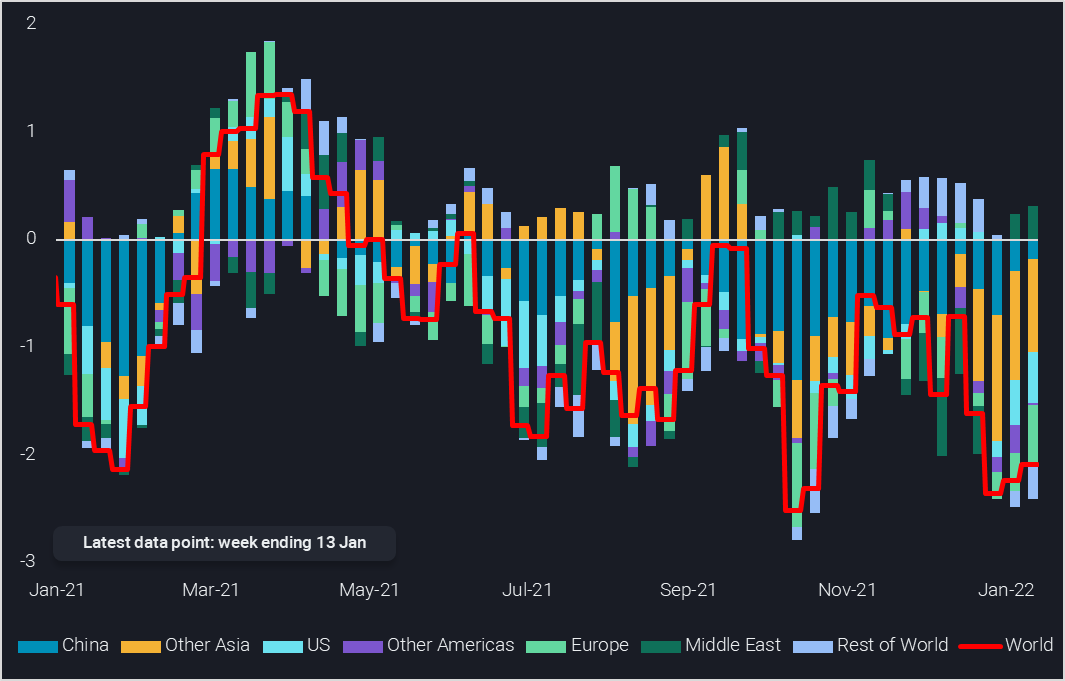

Onland crude inventories are falling again strongly

The takeaway from the above is that any demand decline can easily be counterbalanced by the supply side, with potential pre-emptive cuts joining forces with numerous unplanned outages (Libya, Ecuador, Kazakhstan). In fact, the newest gem in our service portfolio, onland crude inventories, suggests that early 2022 could be prolonging the short-fall pattern hallmarking the year of 2021. Observed global onshore crude stocks have drawn by more than 2mbd (4-week average) in the weeks up to 13 Jan, well aligned with the rate observed in the five weeks to 21 Oct 2021. However, the very latest reporting period, the seven days ending on 13 January, do show a sizable build of 13 million barrels.

Change in world onshore crude inventories (4-week average, mbd)

The two spikes in crude stockdraws fit very nicely with oil prices that are back to $85 per barrel (ICE Brent), only slightly below the 2021 spike observed in late October. Nevertheless, there is a crucial difference in pricing now to that three months ago: the backwardation observed currently is only about half the previous level, using M1-M4 time-spreads for reference.

More upside for oil prices?

What does that mean? One possible answer is that while the front end of the market may face some uncertainty on the S/D balance, further down the line the bets are on tightness rather than oversupply (with the latter being generally indicated by the main agency forecasts). Apart from a fuel demand recovery due to the hopeful end of Covid as a pandemic, it is likely OPEC+ will struggle to add barrels anywhere close to the pace required by the official production target path. In other words, the number of people betting on similar supply-side restrictions in oil this year as observed in natural gas and many other commodities last year is growing?

More from Vortexa Analysis

- Jan 12, 2022: Mediterranean light crude: volumes limited and sold locally, weighing on freight demand

- Jan 11, 2022: China sets tone for refiners with tight oil quotas in the new year

- Jan 6, 2022: Global crude exports end 2021 on a high

- Dec 31, 2021: Making Waves: Looking back at a year of Freight

- Dec 22, 2021: Omicron infiltrates tankers in the Atlantic basin

- Dec 21, 2021: Asian refiners find silver linings amidst an ominous Omicron outlook

- Dec 16, 2021: Volatile global flows and hydrogen economics leave Europe short in naphtha

- Dec 14, 2021: 2022: The Freight Forecast

- Dec 9, 2021: Big oil producers shine as refiners

- Dec 8, 2021: Russia and Ukraine: What’s at Stake for Oil?

- Dec 7, 2021: LPG flood reaches Asia and Europe in December