PADD 3 diesel exports losing steam?

PADD 3 diesel exports losing steam?

28 September, 2020

September-loading diesel/gasoil exports from the US Gulf coast (PADD 3) are set to register the largest month-on-month decline since April. The drop means monthly exports are unlikely to surpass a monthly 1mn b/d level again in the rest of 2020, amid an outlook of weaker US refinery runs and a persistently weak European market.

September exports fall

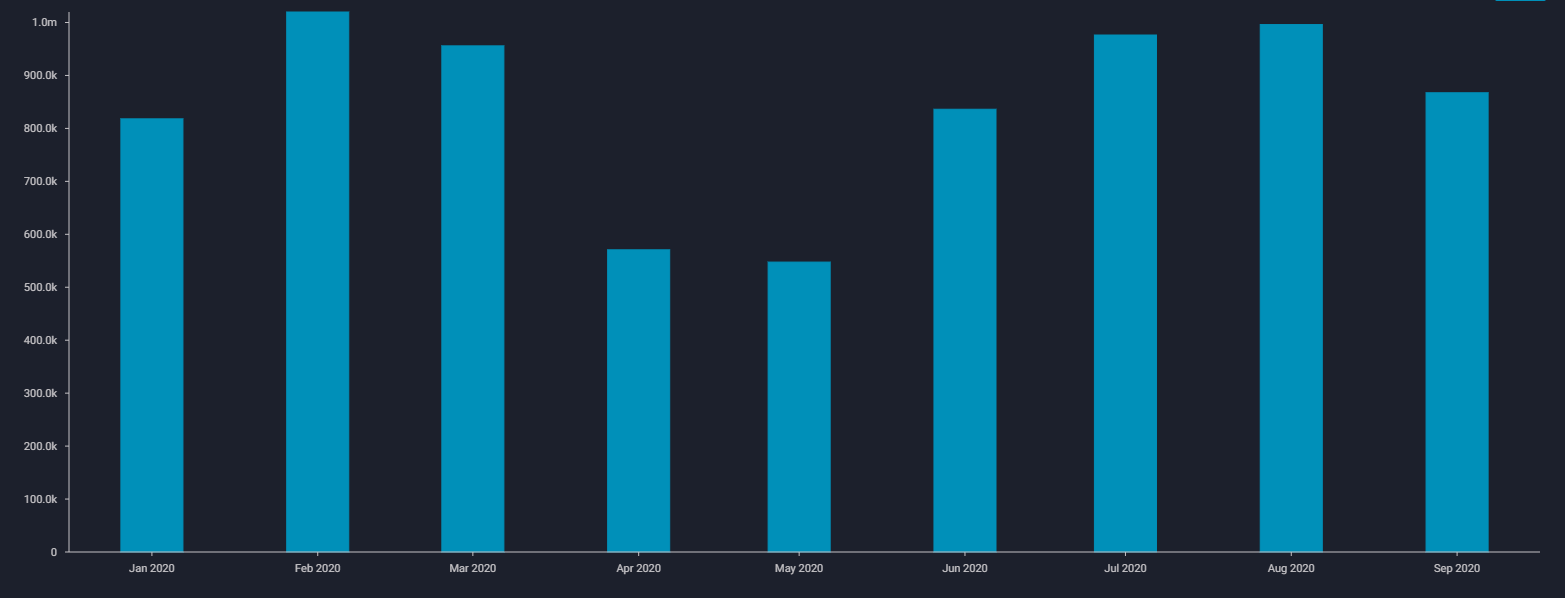

- PADD 3 diesel/gasoil exports are expected to fall to 870,000 b/d in September, down from around 1mn b/d in August, Vortexa data show.

- Preliminary September flows indicate the largest month-on-month decline in exports since April – when total exports almost halved from the previous month, in response to the Covid-19 related demand slump (see chart).

- Prior to September, PADD 3 diesel/gasoil exports had grown every month after May 2020, recovering from the 2020 low of 550,000 b/d that month.

- But given the elevated diesel stockpiles in the US and limited appetite for surplus diesel from key buyers in Europe and South America, PADD 3 refiners are under intense pressure to cut production.

- PADD 3 distillates production fell below 2.5mn b/d for the 4-week period ending 18 September, the lowest since March 2018, EIA data show. And gross inputs for PADD 3 refineries for the same 4-week period fell to lows last seen in September 2017.

PADD 3 Diesel/Gasoil exports (b/d)

See latest data in the Vortexa platform

European weakness

- The drop in PADD 3 total exports comes at a time where the European diesel market – a key importer of PADD 3 diesel, is weakening considerably.

- Transatlantic PADD 3 diesel/gasoil flows are little changed on the month at around 200,000 b/d in September, but down from the year-to-date high of 230,000 b/d exported in February and July.

- North west European diesel cracks to North Sea crude registered a 21 year low in September, reflecting the current depressed demand/high supply environment. The longer this persists, the less viable arbitrage flows from PADD 3 will become.

Want to know more about these flows?

{{cta(‘bed45aa2-0068-4057-933e-3fac48417da3′,’justifycenter’)}}