Q&A: Russian oil exports are starting to recede

Following up on our APAC Webinar, we are answered questions on Russian oil exports, and the implactions on European and Asian crude and product flows, as well as repercussions for clean and dirty shipping.

Inspired by the interesting questions asked by our audience in today’s APAC Webinar, we have compiled key questions and answers about the latest trend in Russian supplies and the related reshuffling of crude and product flows and implications for clean and dirty shipping. You can still register and watch the recording:

{{cta(‘8350dfe4-77b3-4c24-bd38-52bb3e67dc5d’,’justifycenter’)}}

Question: Is it still true that Russian oil exports are flowing normally?

David Wech (Chief Economist): the monthly averages for crude, diesel and light distillates are still in the normal range for March-to-date. But as the month progresses it becomes clearer by the day how strong the resistance of so many buyers is to take Russian cargoes. Dirty product exports are already down to 600kbd March-to-date and 400kbd for the last week, which compares to usual levels above 900kbd.

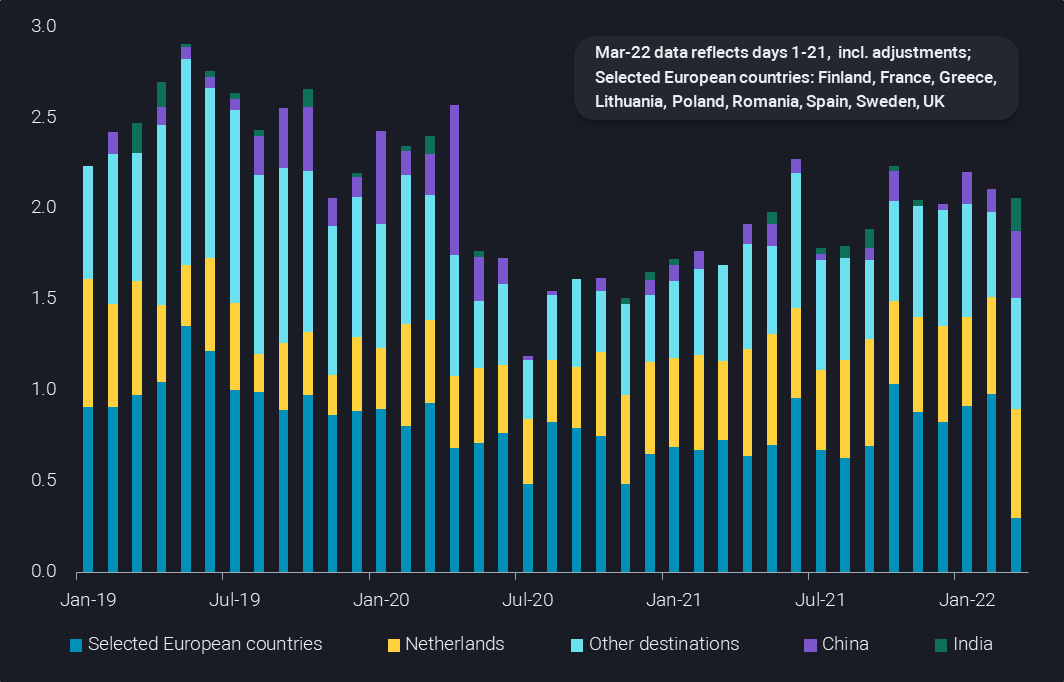

While exports are generally continuing to flow, there is a big reshuffling going on in terms of destinations. Nine key European countries have cut their imports for March-loading Russia crude to 300kbd from 1000kbd in Feb. For diesel, Europe except for six key importers has cut arrivals by more than 50% of 300kbd. And this is all for cargoes that have surely been booked before the Ukraine war started. So it can only be expected that Russian exporters will struggle much more once fresh barrels need to be placed.

Departures of Russian crude from the Baltic, Black Sea and Arctic by destination (mbd)

Question: Is Asia and/or somebody else soaking up the Russian barrels?

David Wech (Chief Economist): So far there are no indications that anybody is strongly soaking up unwanted Russian cargoes. India has opportunistically taken some cargoes but this is too little to really make a difference for the unpopular Russian market. Trading houses are compiling VLCCs to move Urals in large quantities to the Far East, but it does not appear that there are firm final buyers behind these moves. Chinese players are largely staying on the sidelines so far.

Also for diesel signs are growing that some cargoes may leave European markets, with some vessels signaling STS areas in the Mediterranean. But no clear trend is observable so far.

Question: Why do dirty freight rates stay depressed if Russian crude is rerouted to Asia?

Ioannis Papadimitriou (Senior Freight Analyst): Russian volumes going to Asia would be beneficial for VLCCs and Suezmaxes at the expense of Aframax tankers – at a first glance that is. The question remains as to how Europe then replaces these lost Russian barrels. The most suitable candidates are located in the Atlantic Basin. Hence some of these barrels from the Atlantic will end up going to Europe instead of Asia at the expense of VLCCs. Thus, although the long-haul Russia-to-East Asia trade does boost demand for VLCCs, the lost Asian-bound cargoes from the US Gulf Coast and North Sea for instance, will negate this effect. Meanwhile Aframaxes, which were expected to be negatively impacted from lower Baltic-to-UKC and Black Sea-to-Mediterranean flows – will actually be compensated from this change in flows. Ultimately, the overall tanker tonne-mile demand changes per vessel class will remain negligible.

Moreover a potential build-up in floating VLCCs with Russian crude in Asia will be small in comparison to vessel oversupply, with tonne-mile demand still being down by 10% from the 2019 average.

Question: The global diesel market seems to be experiencing much higher volatility compared to the other refined products in recent weeks. Is this mainly driven by changes in Russia’s diesel trade flows or are there other factors at play?

Serena Huang (Head of APAC Analysis): The lack of transparency and clarity on how much Russian diesel will land itself in Europe has created much uncertainty on Europe’s diesel balances in recent weeks. Initial fears of a severe tightening of diesel supplies in Europe were allayed when the European Union (EU) announced that no energy sanctions would be imposed on Russia. We continue to see Russian diesel cargoes discharging in Europe over the last two weeks, although the key difference lies in a rise in volumes seen discharging in six European countries, among them, the Netherlands, Germany, Italy and Poland, and a corresponding decline to the rest of Europe. More Asian diesel cargoes are also heading to Europe this month, further boosting supplies.

Diesel cracks are on the rise again this week, in anticipation of tighter global supplies with several Asia and European refiners entering planned maintenance and peak seasonal demand in LatAm next quarter. Global diesel inventories remain at multi-year low, offering limited buffer to supply disruptions. The Europeans that are shunning Russian diesel have to surge for alternative supplies from the Middle East, Asia and potentially the US, which would create a reshuffle of global diesel flows, and exacerbate volatility in the market. Reflecting the urgency for some of these resupplies, a number of tankers has left New York harbor with diesel for Europe, reversing the flow from just a few weeks and months back.

Extraordinarily high diesel cracks are surely supported by all these fundamental factors, with a tough battle between the East and the West for Wider Arabian Sea cargoes likely to materialise.

Departures of Russian-loading diesel (excl. Far East & tiny tankers) by destination (kbd)

Question: Will a reshuffle of global diesel flows create any clear winners and losers in the clean tanker segment?

Ioannis Papadimitriou (Senior Freight Analyst): We see two options of a global diesel trade reshuffle which could both play out at the same time. In the first scenario, Europe draws diesel supplies from Asia and the Middle East, while Russian barrels head to Asia. This would boost LR1 (MEG/India-to-Europe) and LR2 (Russia-to-Southeast Asia/Far East) tonne-mile demand, at the expense of MR demand from Baltic-to-UKC.

In the second scenario, Europe increases diesel imports from the US Gulf Coast, while Russian barrels head to LatAm. In this case, MR demand would benefit from the longer haul Baltic-to-Latam route, as short-haul Baltic-to-UKC volumes evaporate. So, yes, clean tankers, especially in the LR segments will benefit from Russian developments.

Question: China used to be the big bull factor in the oil market for decades. What are the perspectives right now?

Emma Li (China Market Analyst): The bullish contribution at this point of time comes from the lack of clean product exports, with diesel being crucial. This is unlikely to change in the coming months, as refiners are guided to refill product stocks, while the current Covid-wave and upcoming maintenance cycle keep refining operations and in extension crude procurement at pretty low levels, especially in the teapot segment in Shandong, where crude stocks have been building for weeks.

The country is likely to ultimately take more Russian oil, but so far the approach is pretty cautious. It does not look like China will just soak up any unwanted Russian barrel, as it has to balance its interests and ties with Russia and the western world, with the latter receiving and paying for most of its exports.

China clean product exports (kbd)

Question: Do you foresee Russia’s naphtha supplies to continue heading to Asia?

Serena Huang (Head of APAC Analysis): It is interesting to see that Russia’s naphtha exports from its Baltic and Black Sea ports to Asia had registered a sharp fall in February even before the country’s invasion of Ukraine. Naphtha exports from the aforementioned ports totaled 320kt in February, almost half the volumes in January.

The reality is that Asia’s cracker operators had already been gradually cutting runs in lieu of weak margins since late last year, as the downstream plastic derivative prices have failed to catch up with the surging naphtha feedstock costs. LPG’s wide discounts against naphtha in the recent months have also encouraged cracker operators to switch a part of their feedstocks from naphtha to LPG. Only one LR1 naphtha cargo has loaded from Russia’s Tuapse port this month.

Considering the poor economics and heightened risks of handling Russian cargoes, Asia’s cracker operators, at least in key markets South Korea and Japan are likely to halt imports of Russian naphtha.

More from Vortexa Analysis

- Mar 17, 2022 The case behind rising East CPP rates

- Mar 16, 2022 How quickly can Europe pivot away from Russian gas

- Mar 15, 2022 The reshuffling of Russian diesel flows offers some surprises

- Mar 10, 2022 Russian oil sanctions set to deal a hard blow on Asia’s economy

- Mar 9, 2022 Current reality to weigh on crude tanker earnings

- Mar 8, 2022 Too many unknowns in “Zeitenwende”, but prices are set to rise

- Mar 3, 2022 What would a reshuffle in flows mean for tanker demand?

- Mar 2, 2022 European refiners can live without Russian Urals

- Mar 1, 2022 New world order = new oil trade order?

- Feb 24, 2022 Light-sweet crude prices soar amid Europe’s thirst

- Feb 23, 2022 European diesel market stuck in tightness