Russian diesel export ban’ s wider implications

We review the latest trends in seaborne diesel exports in light of the recent announcement to ban certain Russian product exports.

On September 21, the Russian government announced plans to ban (temporarily) exports of diesel and gasoline to international markets. Marine gasoil and high-sulfur gasoil were exempt from the ban after further clarifications, but the announcement sent October Ice gasoil futures up by 5% on the day before falling back down to previous levels, possibly a reflection that the market expects a temporary stoppage. Since Russia took over from the US as the world’s top diesel exporter in 2023, accounting for over 13% of the global supply, how will a reduction in flows impact the wider market?

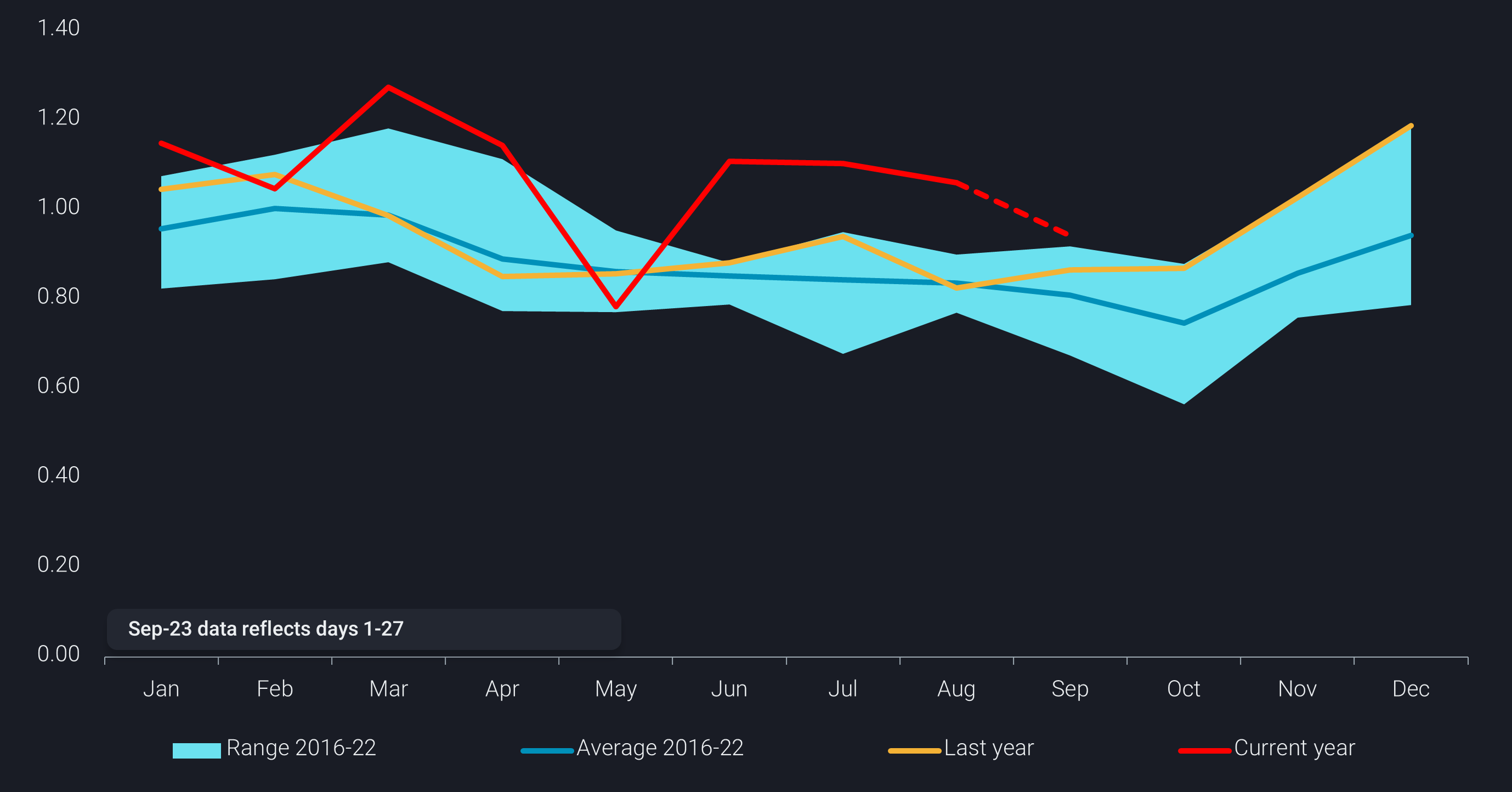

Have Russian diesel exports declined recently and if so how much?

Russian diesel exports on a monthly basis in September had already begun to decline, likely from maintenance on the Ryazan refinery (430kbd) and the Syzran plant (200kbd) (Argus Media) falling 25% in September (days 1-27) from the peak observed in March 2023 with the largest reduction coming from Baltic ports. However, total Russian diesel exports have soared 15% higher Jan-Sep 2023 compared to Jan-Sep 2022 likely to fund the wartime economy.

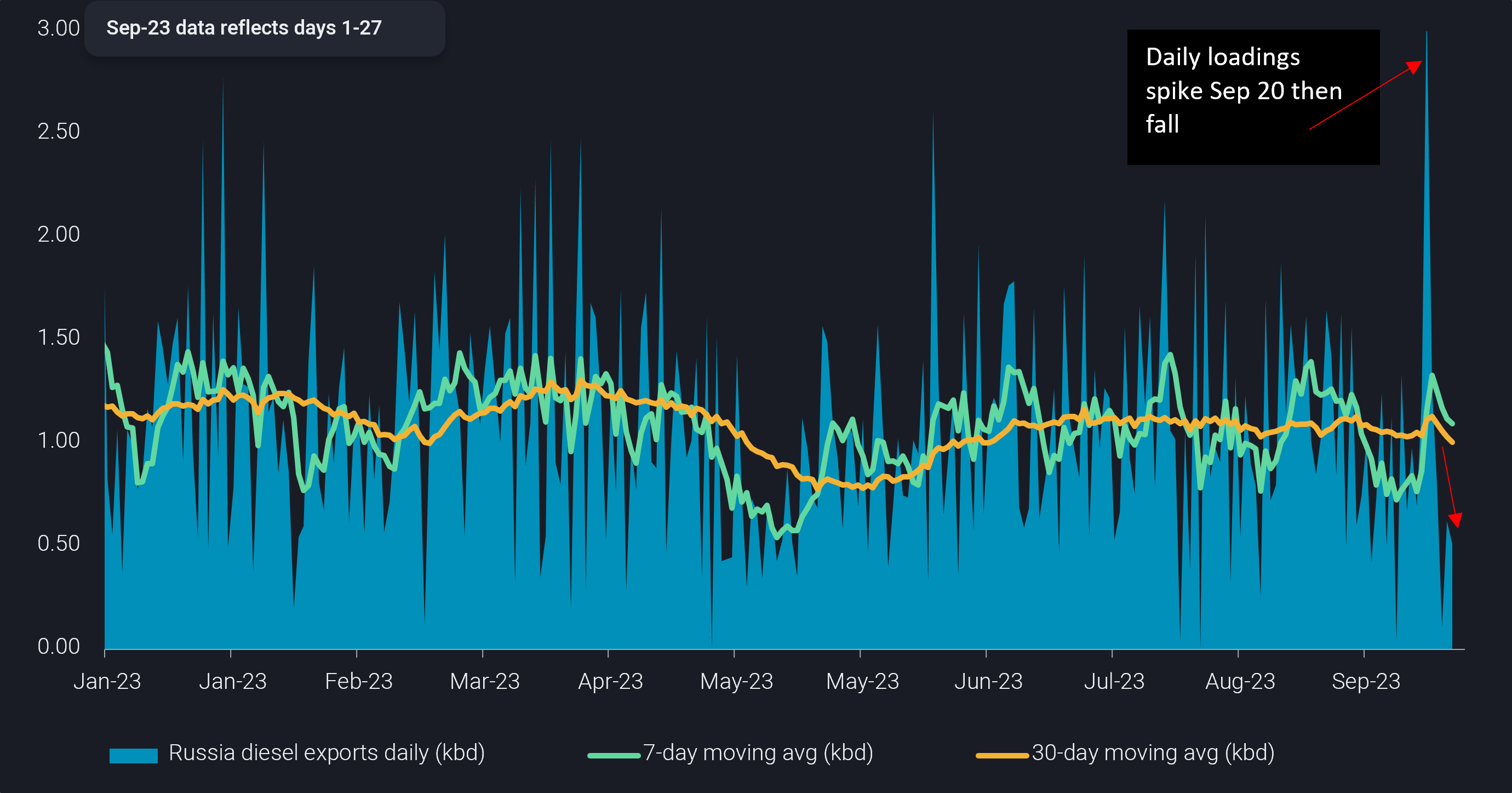

However, if we take a closer look at the daily diesel loadings, we have seen a significant slow down since Russia’s announced ban placing downward pressure on the daily and weekly moving averages.

Implications for the wider diesel market

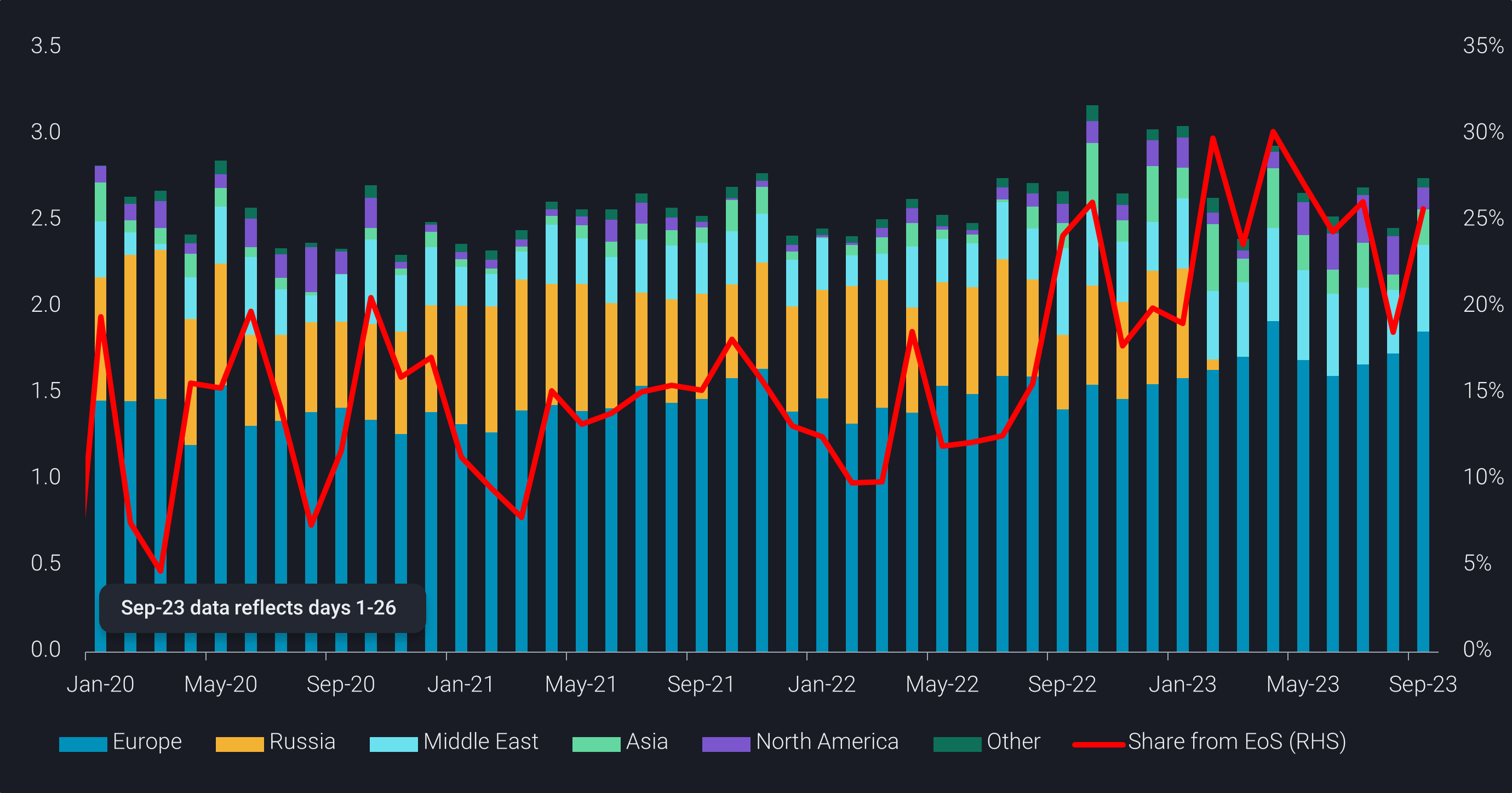

After Europe imposed its well known import ban, Russian diesel found new buyers in Turkey, Brazil, North Africa and the Middle East.

Before the ban, Russia supplied 40% of Turkey’s diesel, with India second at nearly 20%. However, over the past nine months, that share from Russia has jumped to 80%, redirecting flows from India elsewhere, mainly South Africa and Australia. Meanwhile, Turkey’s diesel exports have nearly doubled from Jan-Sep 2023 compared to Jan-Sep 2022, placing growing volumes into European countries including Italy, Spain, and Greece. If Russia’s ban on diesel exports is long lasting, Turkey will be again looking for a new supplier for diesel on the international market and likely unable to resupply Europe.

Brazil is the other market that will likely feel the pinch. Before the European ban on Russian diesel, Brazil imported on average 250kbd of diesel in 2022 with nearly 60% originating from the USGC and nearly 20% from India. After March, 50% of Brazil’s diesel imports came from Russia, backing out a large portion of the US flows and all of the barrels from India.

And while core Europe (EU 27+UK) have largely filled the diesel shortage by East of Suez suppliers, there could be more competition coming for those barrels if the Russian diesel export ban is prolonged.

Consequences to Russia

While a ban on diesel exports from the largest diesel exporter sounds precarious for the wider diesel market amid low stocks and heading into winter, in reality it could significantly harm Russia if prolonged. Tank storage is said to be only a few weeks away from tank tops and shutting down refineries and minimizing pipelines is normally tricky business from an operational perspective. Russia can export more gasoil and diesel with a higher sulfur content, but the market for these barrels is fairly limited and will fetch a much lower price than diesel.

Meanwhile, the ban on gasoline exports does not represent a material problem to the market. Russia typically only exports around 100kbd, 1% of the total export market and its quality is dubious.

How long Russia’s diesel export ban will go on is too soon to tell, if the ban is short lived, it would largely mean delays in the supply chain and less of a loss of barrels, which the market will likely cope up with.