US gasoline demand moulds the Atlantic MR market

The recent drop in US refinery throughput following the North American winter storm has strengthened transatlantic gasoline flows, while exerting pressure on Medium Range (MR) tankers operating in the Americas. But looking forward, the tables could be turned.

The recent drop in US refinery throughput following the North American winter storm has strengthened transatlantic gasoline flows, while exerting pressure on Medium Range (MR) tankers operating in the Americas. But looking forward, the tables could be turned.

Crude processing by US refineries during the last week of February fell to lows last seen in 1982 according to EIA. Meanwhile, domestic gasoline demand has increased in the aftermath of the February ice storm, pushing refining margins to levels last seen when hurricane Harvey hit the US shores in September 2017. The 3-2-1 crack spread against WTI Houston – a proxy for US refineries’ total refining margins – crude averaged $16.80/bbl for the week ending March 5, according to Argus Media, up by 42% from the first week of February.

Depressed crude processing activity in PADD 3 has on one hand weighed on the region’s gasoline exports, and on the other hand boosted PADD 1 and PADD 3 gasoline imports, our data show.

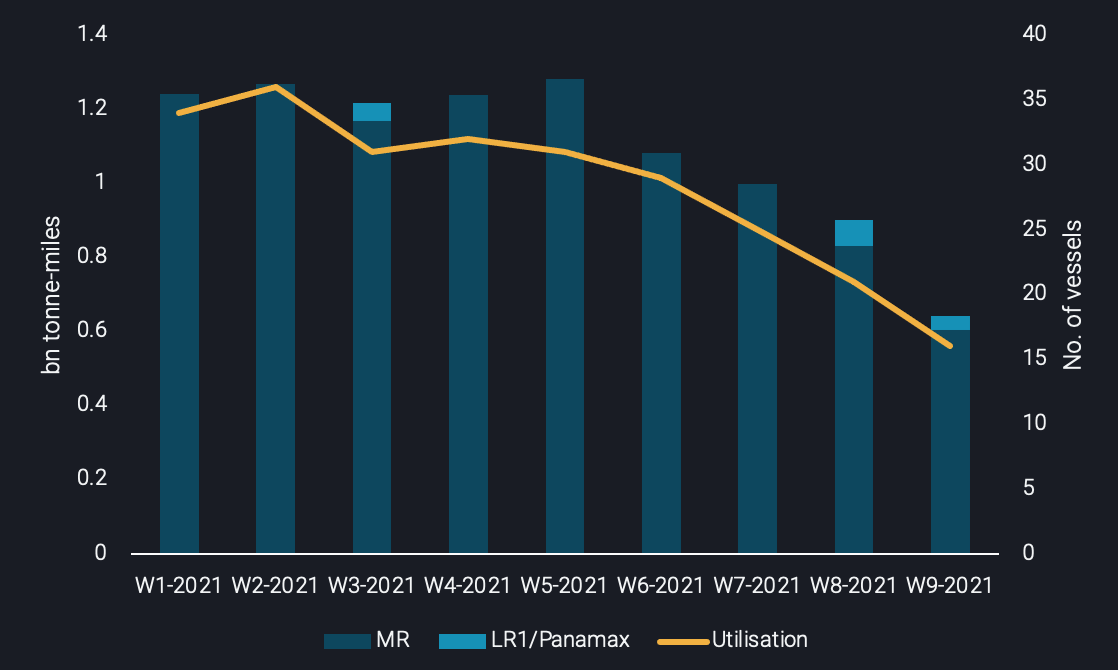

Weak PADD 3 exports to Latin America pressures rates downwards

- Gasoline/blending components departures from USGC to Latin America in February thinned on a m-o-m basis by 40%. The limited supply, however, is only one part of the equation. For countries such as Mexico, historically the largest importer of US gasoline, ailing demand for refined products has exacerbated the decline in flows.

- As a result, utilisation for tankers – predominantly MRs – carrying gasoline from PADD 3 to Latin America has been declining steadily since the start of the year. The trend has continued in March, as utilisation fell by 15% w-o-w for the week ending on March 7.

-

The drop in cargo volumes across this route has added downward pressure on the freight market, which for the USGC – North Brazil route has dropped by 10% from the start of February to March 8, according to Argus Media. But as Texas refineries are gradually coming back online and supply normalises, an uptick on gasoline flows out of PADD 3 and, freight rates, is expected.

MR and Panamax tonne-miles (billion) vs. Utilisation (no. of vessels)

Rising Transatlantic utilisation for MRs could reignite rates

-

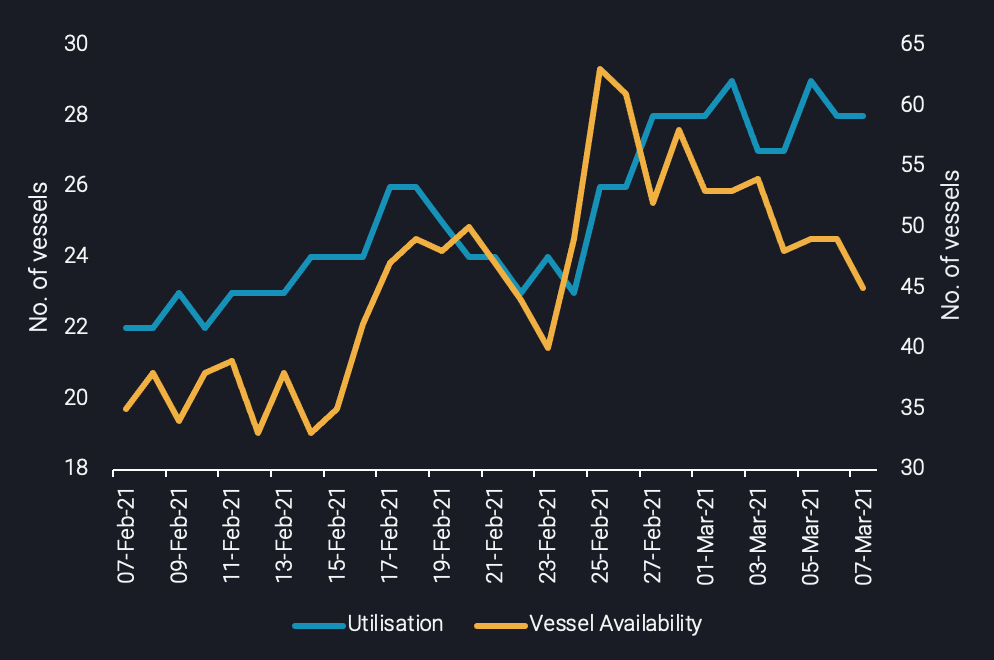

Conversely, global gasoline arrivals into PADD 1 and PADD 3, predominantly on MRs, spiked during the week ending in March 7 while similar volumes are expected for next week, as gasoline inventories are currently below the 5-year average figure, according to EIA. This has a positive knock-on effect on the freight market, as MR utilisation for the Europe – US Atlantic route reached the highest point since the start of May 2018, according to our data.

- On the supply side, vessel availability for clean MR tankers basis Rotterdam is down 13% w-o-w for the 5-9 days window on the back of heavy fixing along the Europe to PADD 1 route. Freight rates for MRs on the East-West transatlantic route slumped in the aftermath of the Texas storm, yet a rebound could be on the cards. A firm arbitrage from northwest Europe to the US Atlantic for gasoline should keep loadings firm, which could trigger higher rates.

- Still, this development could prove to be short-lived as PADD 3 refinery throughput will naturally rise to capture higher refinery margins, eventually closing the arbitrage, while vessel supply could increase from MR tankers ballasting from the Americas towards Europe seeking better employment conditions.

Europe – PADD1 & PADD 3 MR tanker utilisation (LHS) vs Vessel Availability (RHS) (no. of vessels)

Want to get the latest updates from Vortexa’s analysts and industry experts directly to your inbox?

{{cta(‘cf096ab3-557b-4d5a-b898-d5fc843fd89b’,’justifycenter’)}}

More from Vortexa CPP Analysis

- 4 March 2021, Infographic: The freeze on Texas refined product exports

- 23 February 2021, Altona’s refinery closure: implications on trade flows and freight

Vortexa In the News – CPP

- Bloomberg, 5 March 2021 – European Gasoline Diverted to Texas to Ease Supply Crunch

- Bloomberg, 8 March 2021 – Asian Diesel Glut to Swell as Indian Oil Refiners Boost Exports

- Reuters, 9 March 2021 – Diesel storage in Scandinavian caverns unwinding