Russia vs China – a bull or a bear market?

Russian crude oil exports are rising strongly in April, adding pressure on oil prices on top of China’s Covid nightmare and SPR release. But a number of factors speak for a renewed tightening of markets.

WTI futures have started the week in double-digit territory – somewhat surprising given IEA expectations of a loss in Russian oil supply of up to 3mbd next month. Of course, China and its uphill struggle to contain Covid is a huge bear factor, while SPR releases also help to cool prices. And not even Russia is a clear bull story, given surging crude oil exports over April, accompanied now by the resumption of normal CPC Blend exports.

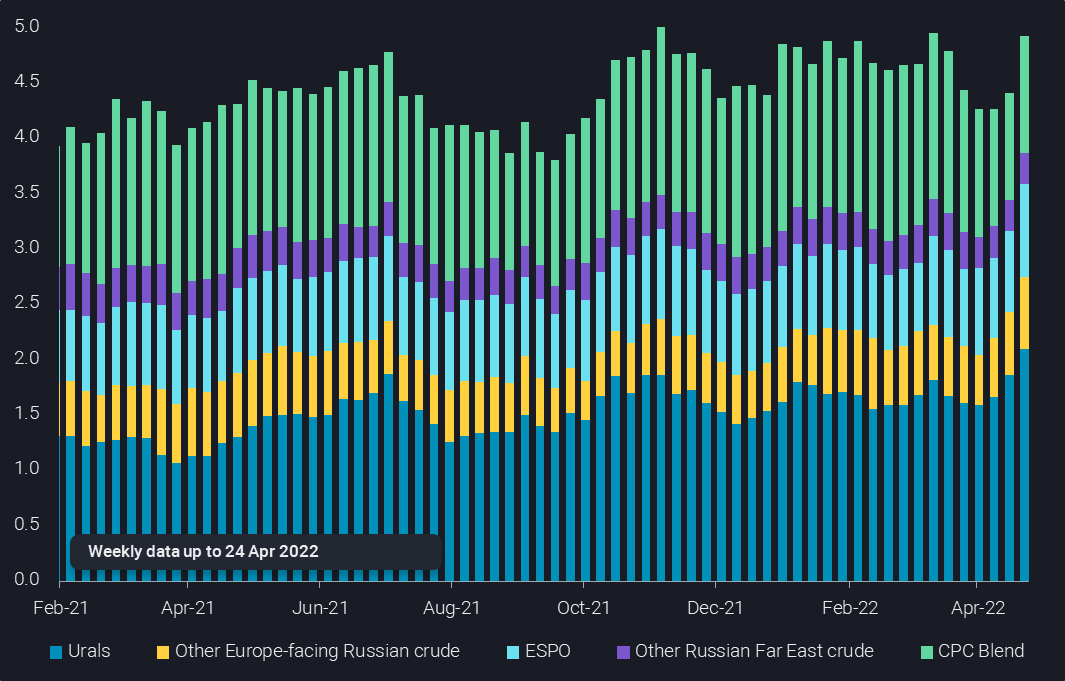

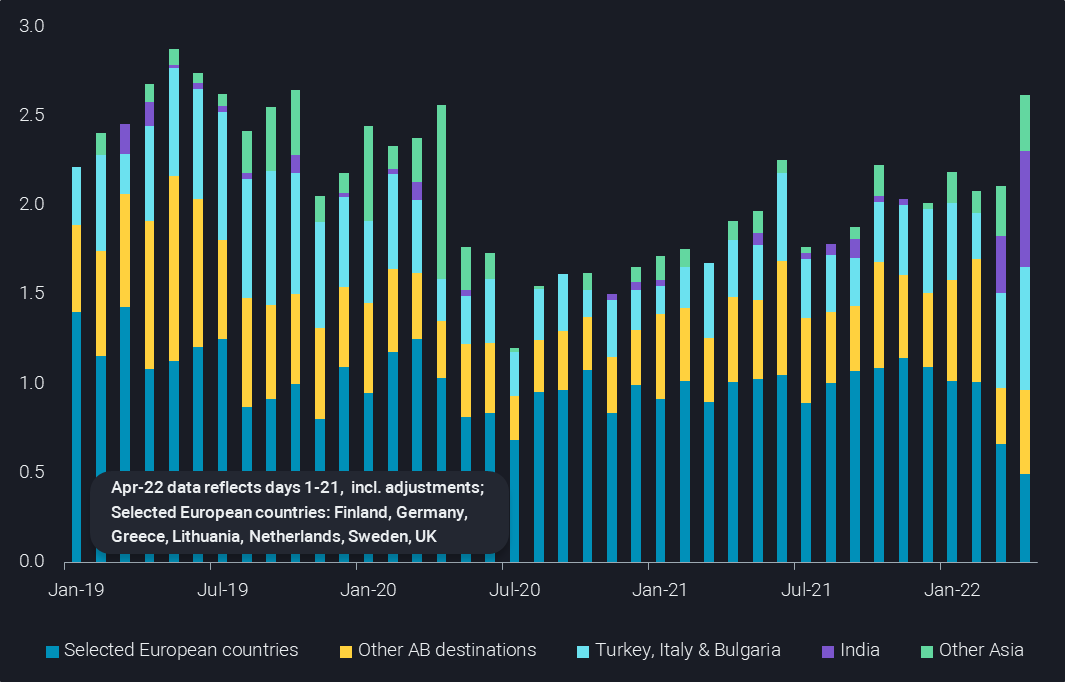

More than two months after Russia’s invasion of Ukraine, crude exports from Russian ports are close to 5mbd on a 4-week average basis to 24 April, very much at the top end of the range established over the last year. And exports of Russian crude only towards Europe, excluding CPC Blend and Far East exports, are on track for the highest monthly reading since October 2019 (see second chart).

Most of the drop in crude exports from Russian ports since mid-March has actually been due to the outages at the CPC Blend loading terminals in Novorossiysk, taking out 600kbd in the four weeks to 17 April, vs the average level before in 2022. And over recent days, we saw CPC Blend exports resuming normal levels, providing further upside to oil supply.

This means that currently the global crude balance is very roughly 2mbd longer than anticipated ahead of the Ukraine war, made up of about 1mbd of demand losses in China and 1mbd of SPR stock draws. As stated above, Russia-loading crude supplies are roughly unchanged. From that perspective, it is not that much of a surprise that crude prices came under pressure. Also, the financial market is clearly aligned with the physical one, as crude differentials around the world are under pressure, and the market structure has become much weaker, including even some front-end contango in Brent CFDs.

What is happening right now is always of relevance for oil market participants, but the crucial question is what will happen next. And from a trend perspective, a lot of indications do suggest that markets will tighten over the coming months, including:

- Latest political developments around Russia do not give any hope for a quick path to peace/normalisation; rather steady escalation is at play, including Russia cutting pipeline gas supplies to Poland as one of the latest examples

- European politicians are slow on energy sanctions, but the signs are intensifying by the day that some sort of oil export ban is coming, and even existing EU sanctions coming into full effect on 15 May may provide a framework to scale down Russian oil imports formally

- Recent reports on Russian oil export tenders suggest very limited interest from global buyers, but of course, this needs to be taken with caution as the very most deals will happen on a private and confidential basis; nevertheless, the April export spike still benefited from deals concluded ahead of the war, and the more time passes the more difficult it will get for Russia to sustain export flows, given in particular the limited Chinese interest

- Seasonally there is still quite some upside from the demand side, as refiners conclude maintenance work and look forward to peak travel demand

- Furthermore, immediate price effects on consumption usually subside relatively quickly, while outright prices have rather eased than risen further over recent weeks; this implies some additional demand upside in the coming months

- High refining margins across world regions indicate that operations have some consistent need to scale up, requiring more primary feedstock (crude) along the way, amid other reasons as Russian secondary feedstocks are missing

- As Covid comes in waves at some point in time the situation in China is also set to improve, albeit that does not look to be imminent

If the above fails to materialise, some type of wider demand destruction and economic recession is likely at play, potentially in combination with additional supplies from some markets like the US or perhaps even Iran. An end to the Ukraine war within a few months, meanwhile, is not a bet a lot of experts would take. But neither can it be excluded. In the meantime, there is no alternative to regularly keeping a close eye on actual Russian oil exports for guidance on the oil market’s direction.