The case for higher refinery margins

A step higher in demand and the need to compensate for rising feedstock and energy costs calls for higher refinery margins, as even the weaker players need to be encouraged to run

Inspired by today’s webinar (on-demand here) this blog summarises the rationale for even higher refinery margins down the road.

Fundamentals point to a substantial tightening of crude and product markets from here onwards. Based on unsustainable stockdraws in Q3 above 3mbd, and a likely step higher in demand of close to 2mbd, the market calls for up to 5mbd of additional supply. But OPEC+ exports, excluding Saudi Arabia and UAE, have actually declined by 1mbd since April. This is despite quotas allowing for an increase of 1.5mbd over the same period.

Our conclusion is that these countries do not hold relevant spare capacity and that of Saudi Arabia and the UAE is probably limited to 3mbd by now. Upstrean production decline rates are strongly feeding through amid a lack of investment, driven by Covid-19 repercussions, difficult financing against the energy transition background, and mis-management.

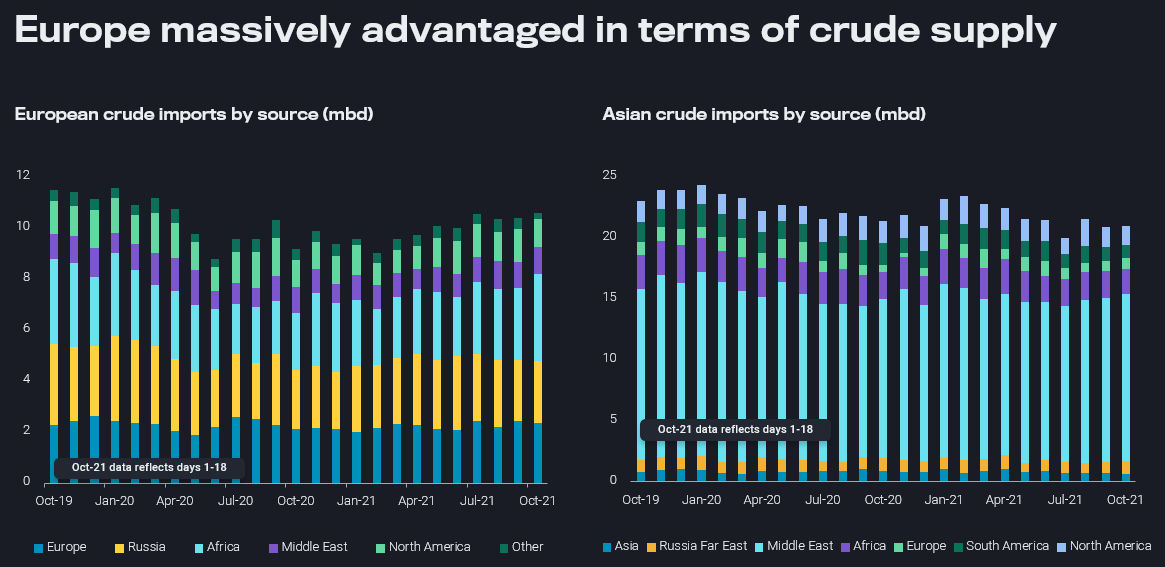

Crude prices are likely to rise further, and crude procurement will get more challenging, especially as Asian demand recovers. But Europe is well positioned in this contest. On the one hand, the crude slate is so much more diverse by origin, with Asian procurement being dominated by Middle Eastern barrels.

That makes Europe better sheltered against specific outages or shortfalls. European supplies are mostly coming from within or very close to the region, limiting freight costs. In contrast, Asia has to import nearly everything, with Middle Eastern barrels being the relatively short-haul ones (with a voyage time from Kuwait to Japan of typically close to one month). The proximity and diversity of European crude supplies is a particularly welcome feature in a spiky market on both the feedstocks and refined product side, with short planning horizons being feasible.

Product demand is looking strong across segments

Refined product demand across most of 2021 to date was driven by naphtha and gasoline, with lofty LPG providing a booster to both. But now diesel, as versatile back-up fuel, and jet/kero (air travel recovering) are staging a strong comeback. As heating fuels, both jet/kero and diesel are underpinned also by some standard seasonality.

Even fuel oil looks promising right now as the cheapest hydrocarbon to produce power, if technicalities and regulations are accommodating. Overall, we are set for gas-to-oil switching at an unprecedented scale, as incentives are viable across regions, sectors and products. The regularly mentioned 0.5mbd figure could easily turn out as too low, as quite a share of that could come from the refinery fuel sector alone. Meanwhile, gasoline and naphtha are reluctant to take a back seat as illustrated by multi-year high product cracks in Singapore last week.

So products are strong and competing across the barrel, and the same is likely to materialise on a regional basis. The US and Europe are struggling to fully meet domestic demands, and as a crucial factor, Asia is likely to re-emerge as a stronger consumer after spending the last six months in a Covid trough. More intense cross-product and inter-regional competition will serve as regular price drivers.

Higher refinery margins are required to lift operation levels

The last two years have seen a slowdown in new refinery start-ups and an acceleration in announced and quiet refinery consolidation. Similarly to the OPEC+ situation, spare capacity is way more limited than most people think, especially with China changing the course of its domestic refining fleet to self-sufficiency. The expected near-term surge in the call on refinery operations of up to 3.5mbd is easily dwarfing potential new start-ups, which are regularly pushed back anyway. So one big boost to refining margins comes from the demand side.

The other is a cost factor. The IEA sees hydrogen adding up to $5/b to the cost of processing a barrel of crude, while other energy costs are soaring as well. As this market cannot afford to lose currently operating refining capacity, margins need to appreciate to the level where the weakest link is lured into full service.

Against these two factors, the improvement of European refining margins over the last couple of months looks pretty tiny. Further stockdraws will be more costly, requiring stronger backwardation and higher front-end pricing across the board as well. Expect a solid upside for refining margins, even if it may not be a plain sailing all the time – volatility will naturally arise on the back of rising prices and choppy demand destruction.

More from Vortexa Analysis

- Oct 20, 2021 A last hurrah for global gasoline cracks? Probably not

- Oct 19, 2021 Flow highlights (EMEA): Supplies pick up on record pricing

- Oct 14, 2021 Scrubber-fitted VLCCs quietly gain market share

- Oct 13, 2021 Middle distillates take centre stage in Q4

- Oct 12, 2021 Reality check: Are surging oil and gas prices aligned with fundamentals?

- Oct 8, 2021 Event highlights: Redefining trading strategies with China’s new oil regime

- Oct 7, 2021 Q3 Freight Update: Momentum killed