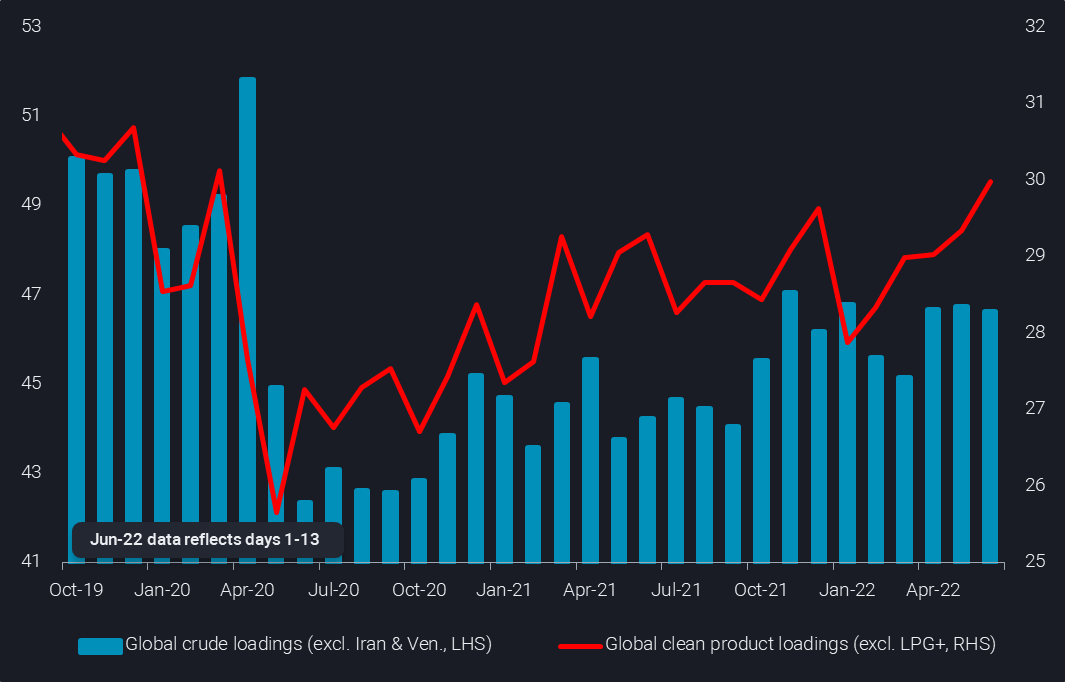

Transportation fuel cracks have been exceptionally strong ever since March and so far there are only limited indications that sufficient additional barrels are hitting the market to meet seasonal peak demand over July and August. Seaborne global clean product liftings (incl. intra-country flows) have been steadily rising since a very low point in January, but even the higher Mar-May average of 29.1mbd is barely up from the respective 2021 levels and nearly 1mbd lower than Mar-May 2019 figures.

Refining capacity shortfall to blame for record pump prices

In this context it is very important to remember that various million b/d of refining capacity have shut down since Covid struck, creating loads of additional markets for seaborne product imports, such as for instance in Australia and US East and West Coasts. So seaborne fuel imports should not just catch up with pre-Covid levels, but easily outpace them by a sizable margin, to rightfully say that the oil market is back in a normal setting.

Looking at global seaborne crude loadings it is even clearer how far we are away from a normal market situation, including pre-Covid demand levels. Excluding Iran and Venezuela, global crude loadings hit a post-Covid peak of 47.1mbd in Nov 2021 and have been lower than that ever since. And relative to Q4 2019, crude liftings in Q2 2022 are on track to fall short by more than 2.5mbd. Nevertheless, global floating-roof inventories have been building at a rate of 1.5mbd in the ten weeks to Jun 2, mostly but not exclusively in China. The coincidence of record refining margins and substantial crude stockbuilds amid lacklustre crude supply clearly calls out the culprit of sky-high fuel prices at the pump: the lack of spare refining capacity.

Global crude (excl. Iran & Venezuela, LHS) & clean product (excl. LPG+, RHS) loadings (mbd)

Now, there are some clear signs that the crude market is picking up strength: the steady increase in outright prices since early May, the comeback of steep backwardation, record premia for some grades, especially in West Africa (Argus), China coming out of Covid lockdowns, and the first global stockdraw in our data in 11 weeks. Will crude prices now finally follow the track of product cracks and appreciate to nominal record levels of above $150/b? A growing number of market commentators appears to hold this belief.

Russian seaborne oil supplies remain strong

In the early days of the Russian invasion, the author of these lines was amongst the biggest bulls. But Russia has largely defied individual and government sanctions, continuing to export oil at pretty high levels. Especially seaborne crude exports towards Europe, via Arctic, Baltic and Black Sea ports, are up by 500kbd q-o-q in Q2 2022, also outpacing the levels observed in late 2019 or early 2020 (“price war” in March/April 2020). What has happened is that Russia has struggled to place exports in non-essential products such as fuel oil or naphtha, forcing domestic refinery run-cuts, and freeing up crude for exports.

But there are signs that Russia is overcoming some of the product export difficulties, and the overall level of crude and product exports is anyway speaking against the idea of persistent domestic crude supply cuts. Maybe domestic consumption is down to a certain extent, some pipeline flows are curtailed (however Kozmino exports to the Far East are also at record highs), and Sakhalin production is suffering, but overall there is very little support for domestic supply losses anywhere close to 1mbd, let alone 2-3mbd. Of course overall export levels may change (or not) towards the end of the year and early 2023, when the latest EU sanctions come into play. But this should not strongly affect prompt crude and product prices in late spring or summer 2022.

Short-term outlook may not anymore be that bullish

Coming back to the short-term outlook, crude procurement indications suggest increased refining interest, and a step higher in global product liftings in early June implies a certain, albeit not massive, reaction by the refining system in the peak operational season. At the same time there is not much seasonal demand upside left in mid June, especially from a procurement perspective. Also some new refining capacity is coming in and a series of recent outages across the globe may come to an end with some luck. Taken together, this suggests that rather than crude prices getting a persistent lift from record product cracks, the situation could reverse, leading to weaker refining margins and range-bound crude prices.

However, we are far away from a consistent and deep correction lower, both for crude and product pricing, as high energy prices have without question eaten into consumption levels. But such adjustments are usually only transitory, especially if prices ease somewhat. With Russia further curtailing gas supplies to Europe, oil will also remain en vogue as back-up fuel. Only a deep recession would have the potential to cool prices more meaningfully and persistently.