2022: The Freight Forecast

In last year’s freight forecast Vortexa described 2020 as one of the most volatile years on record. 2021 saw a more tepid year, with freight rates overall languishing at their lowest levels in years. Vortexa forecasts what 2022 has in store for freight markets.

In last year’s freight forecast we described 2020 as one of the most volatile years on record. 2021 saw a more tepid year, with freight rates overall languishing at their lowest levels in years. Whilst oil demand continued to recover, helped by a global vaccination drive and re-opening economies, this has not been sufficient to jumpstart a morose tanker market. Increasing volumes from OPEC+ have helped a pick up in activity but there is a question as to how far OPEC+ can go to support recovery in 2022 and beyond. Increased refinery runs and recovering demand have helped mostly clean tanker markets throughout 2021. However, endemic oversupply of tonnage has persisted and kept a lid on freight rates globally. It risks continuing to do so as a busy 2022 looms in terms of deliveries.

With a new variant of concern on everyone’s lips and fresh lockdowns again on the agenda, will 2022 be the year of recovery or are we in for an additional year of stagnating freight rates and low utilisation levels? We will review in more detail what happened in 2021 across tanker classes and product segments and aim to identify the main trends that will shape 2022 freight markets, through the lens of Vortexa data.

2021: A Year to Forget for Freight Markets

It is not an understatement to say that freight market participants were fairly optimistic that they had seen the worst of pandemic-related impacts in 2020 and that 2021 would bring about a strong recovery across tanker markets. It was uneven to say the least.

On one hand, crude tanker markets suffered from a recovering oil demand met primarily by stock withdrawals, on the back of record stock builds following cheap crude oil prices throughout 2020 and into early 2021. On the other hand, uneven re-openings and lockdowns across the world did contribute to some clear arbitrage opportunities for clean tankers but kept earnings volatile for owners. Q4 2021 started out on a positive note, with OPEC+ continuing to raise its output even in the face of falling crude prices, as well as a widespread demand recovery across sectors in Asia. However, increased traffic from the Middle East to Asia did not contribute enough to raise global tonne-miles as Atlantic Basin to Asia crude flows decreased in the face of a structural decline in volumes from West Africa especially and lower volumes from Caspian producers.

Demand at record-lows at the start of the year, a slow and uneven recovery for a largely oversupplied tanker market and rising bunker prices on the back of a recovering price of crude rendered 2021 largely as a year to forget for owners and operators in freight markets. We will now aim to forecast whether 2022 looks to be a repeat or if the year ahead augurs a better future.

A Positive Momentum for Freight Rates

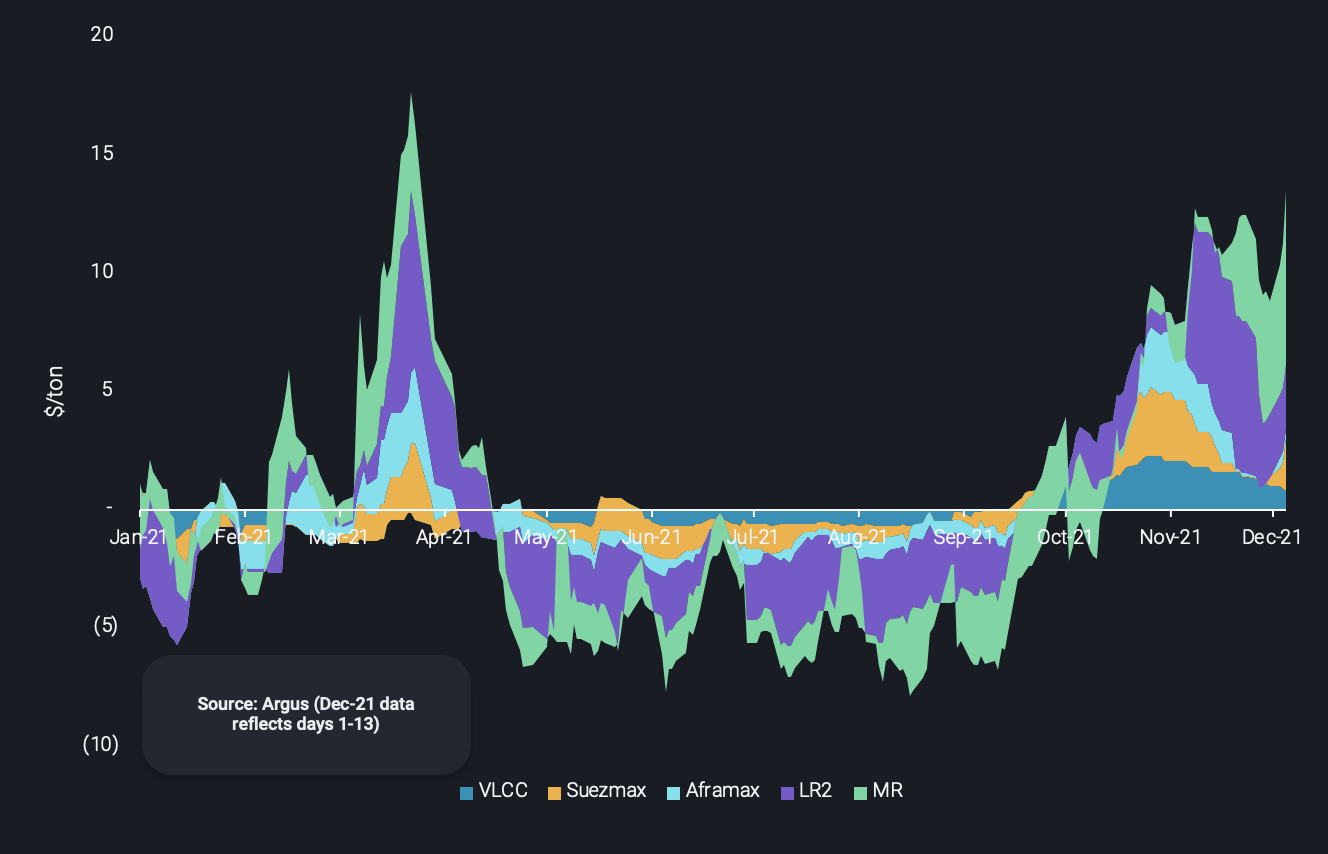

Freight rates vs. 2021 averages across major vessel classes benchmark routes

Throughout 2021, freight rates remained weak. One could easily think it was only a weakness compared to exceptional earnings during the first half of 2020, as well as the second half of 2019. But the reality is that average freight rates across the five major tanker classes have reached 5-year lows in some instances, as well as having been consistently below operating expenses in some segments, especially within crude tanker markets.

When comparing average vs. actual freight rates across vessel classes in the above chart, using pricing data from Argus Media, we can clearly see an uneven start to the year with a spike towards the end of Q1 followed by a very weak summer and autumn where rates suffered from prolonged lockdowns and inactivity. The picture has improved in Q4 and we can see above the positive momentum in rates across both crude/dirty and clean tanker classes. Q4 is seasonally a strong quarter for tanker markets and this statement seems to have held true, as OPEC+ hiked their output as planned and demand for heating fuels such as diesel rose. It is worth bearing in mind however that tanker rates are rising from what remains very low levels.

Looking ahead, we do expect that tanker rates have bottomed out in 2021. But that does not necessarily mean they will recover steadily throughout 2022. By now very low oil and refined product stocks coupled with recovering demand, especially in H2 2022 should be a positive. To confirm this is indeed the case, we will explore in the following section demand and supply dynamics across sectors.

Demand: Is there enough fuel for recovery left in the crude market?

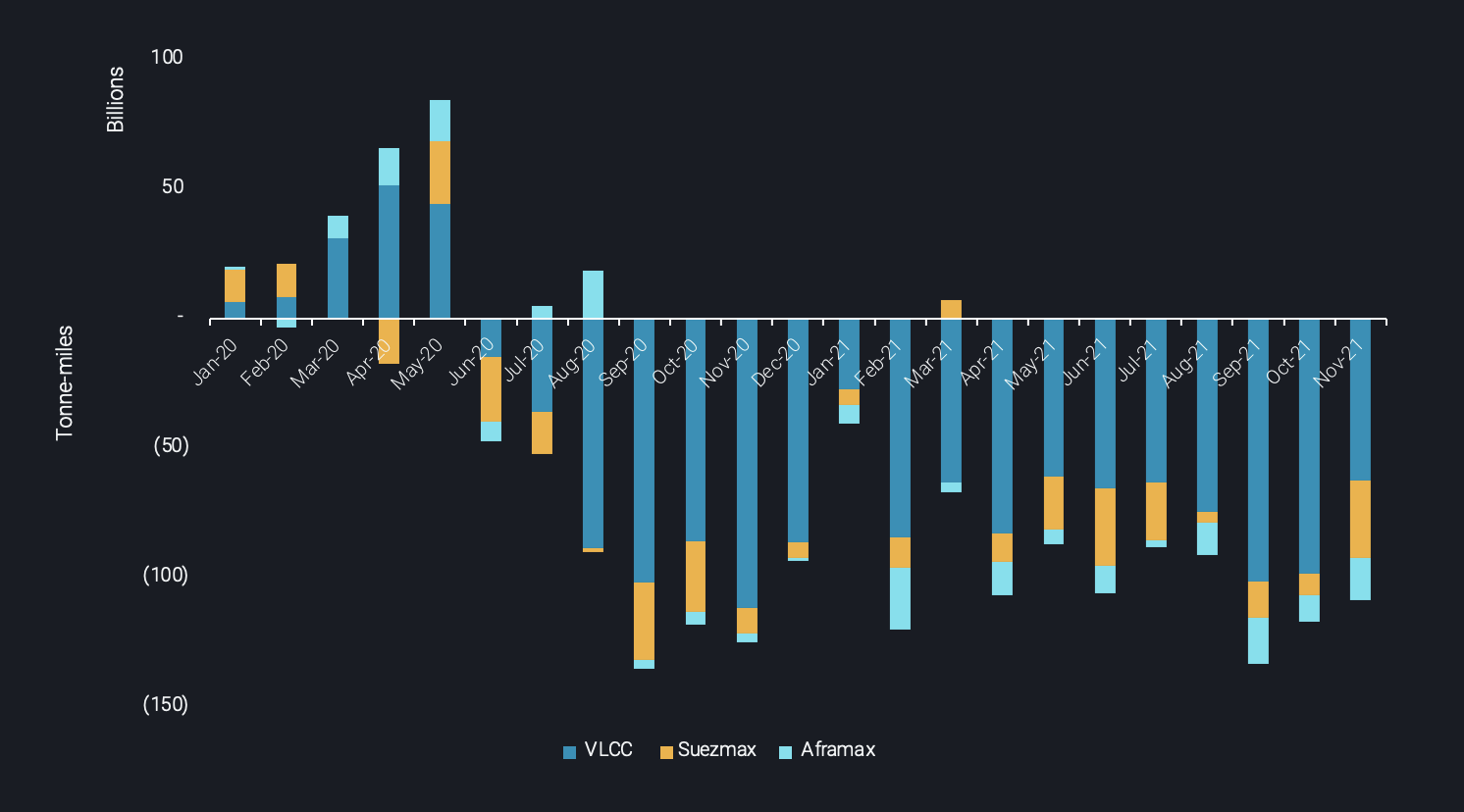

Crude/dirty tanker tonne-miles vs. 2019 average by vessel class

Without a doubt crude/dirty tanker segments have been hit the hardest in 2021. To see how much hope there is for 2021, we will tackle the outlook in four steps:

- What is the outlook for the underlying oil consumption?

- The role of stock changes

- Do market dynamics favour the shipment of feedstock or finished products?

- How far does the average barrel travel?

Some market commentators argued that around Oct/Nov, world oil demand has been back at 2019 levels. While we would argue that this may be somewhat too optimistic it is true that dynamics were very strong at this point of time, especially in the Atlantic Basin (North America, LatAm, Africa, Europe and Russia), but also Asian demand picked up, here in particular the Southeast Asian region, while somehow China may have been the biggest laggard in a highly unusual pattern. Then the triple whammy of 1) rising prices/inflationary pressures, 2) Delta waves and 3) Omicron struck the market. We think that the latter will lead to high-frequency waves all over the world in Q1 2022, based on its high rate of transmission and escape from existing immunisation. The result may well be overstrained health systems and related restrictions, potentially cutting Q1 2022 oil demand by about 2mbd. However, the rapid spreading may fast-track the world from a pandemic to an endemic state, finally allowing a more consistent and persistent oil demand recovery in H2 2022.

2021 taught us well on the difference between final consumption for refined products and marginal needs for shipping crude around the world. A lot of the demand upside was met by a combination of product and crude stockdraws, while OPEC+ has been slow to hike supplies. Apart from being motivated by steepening backwardation in crude and product prices, China added quite a lot to the development, with a clampdown on independent refiners on top of a domestic stockdraw campaign. This must change in 2022, as many inventory readings are by now close to operational minimum levels, while the much-discussed US-lead SPR release will change little when stretched out over time. In fact, the Omicron threat and changed pricing levels and patterns, possibly also an end to Iran sanction, could turn the market from a drawing into a flat and temporarily even building mode, underpinning shipping demand.

Another level of complexity is added by a certain optionality to send either crude or finished products around the world. November has seen a spike in product exports from the US, Russia and the Middle East, and we think there is a strong rationale to this development: a big advantage in feedstock, processing and energy costs in hydrocarbon-producing countries. Natural gas prices, and in extension hydrogen and overall energy costs at many refineries in consuming countries, are set to remain sky-high, at the very least in H1 2022, but likely throughout the entire year. At the margin, the US, Russia, the Middle East, but possibly also countries like Brazil and Mexico, are likely to churn out more refined products, leaving less crude and more clean barrels for the export markets. At the other end of the chain, Asia and Europe may struggle particularly to export surplus products in this setting, leading to lower crude runs and import requirements, at least at the margin.

A final and crucial question is how far the average crude barrel will travel. Vortexa data shows that, bar one minor exception, all vessel classes have seen their tonne-miles remain below 2019 averages for the whole of 2021, with months September to November seeing the largest differences. Even as utilisation overall improved during those months led by an increase in exports from OPEC+ members driven mainly by Saudi Arabia and the UAE, this hid a diverging picture with the rest of the group seeing a decrease in crude exports, specifically out of West Africa. The result of years of underinvestment has left some exporters unable to ramp up crude oil production. West African crude exports were consistently above 4mn bpd up to Q2 2020 and have since plummeted 20-25% to current levels of between 3-3.3 mn bpd in recent months. And the trend is likely to continue in 2022.

In conclusion, 2022 may prove to be a year of two divergent halves. H1 may see strong repercussions from Omicron, reducing overall activity levels. OPEC supplies out of the Middle East could be largely sufficient to supply dented Asian crude oil needs, suffering in that phase particularly from its refinery margin disadvantage. The demand shortfall will be well anticipated, leaving only some room for stockbuilding, which will dampen the impact on the dirty tanker segment somewhat. But H2 2022 could see an industry in full swing, with demand being met from fresh production, given limited inventory coverage. OPEC may struggle to meet all requirements, and Asia may particularly resort to US-stemming barrels, which are boosted by a combination of shale growth and significantly higher Canadian supplies. The latter enjoy much better accessibility after recent infrastructure improvements. The very long-haul US barrels could prove to be a boon for the VLCC segment. More light-sweet crude barrels from the Atlantic Basin could also move eastwards, motivated by lower processing costs.

Demand: Refined products demand kept clean tankers afloat

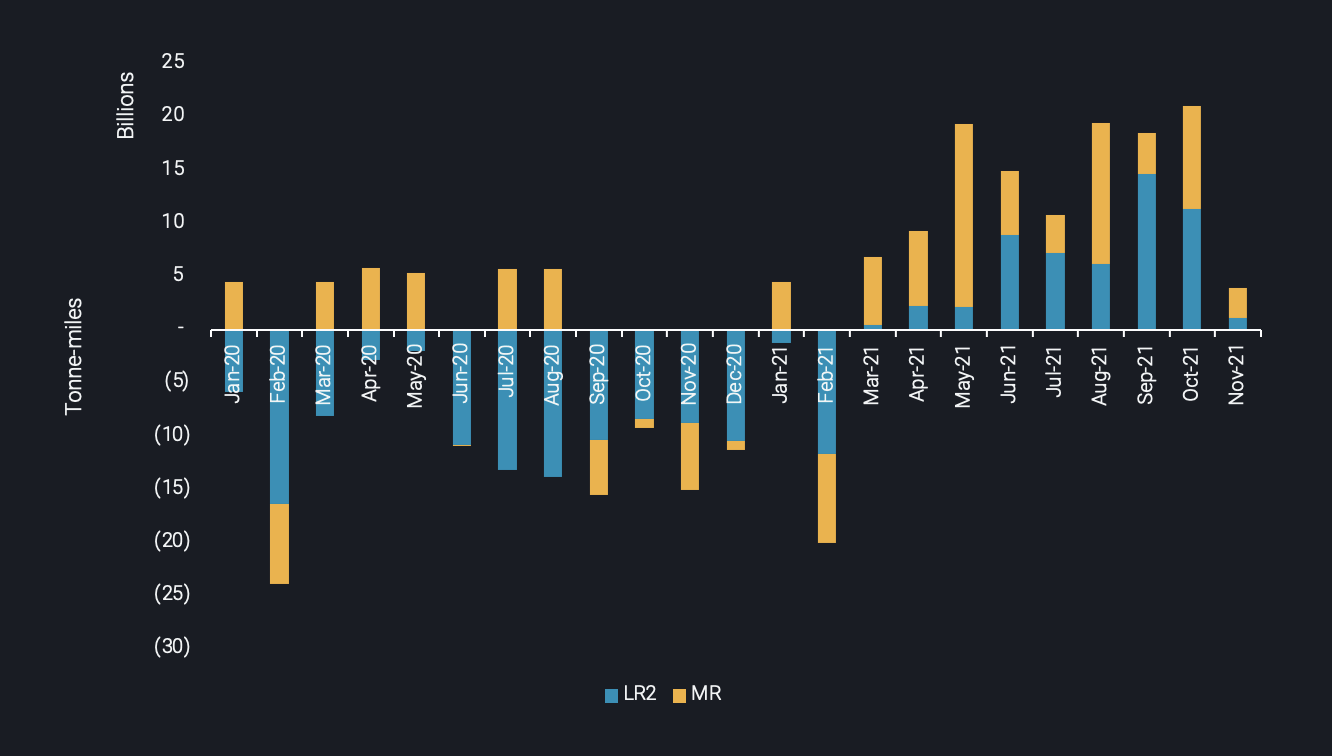

CPP tanker tonne-miles vs. 2019 average by vessel class

Clean tanker segments have fared better throughout 2021 than their dirty counterparts. Through the lens of Vortexa’s freight data, we can see that CPP tanker tonne-miles were above their 2019 levels for both vessel classes by March 2021 and remained that way, seeing strong support in Q2 and Q3 specifically. A global surge in diesel requirements has benefited clean tankers, especially originating from the East of Suez, also contributing to higher tonne-miles within the LR category. Gasoline and diesel flows have already returned to pre-pandemic demand levels in Q4, helping fuel a recovery in the MR tanker market segment specifically, whilst strong demand for naphtha as a petrochemical feedstock from Asia helped LR2 rates gain momentum in the second half of 2021. It is worth mentioning that we witnessed a number of LR2 tankers cleaning up throughout 2021 to exit the crude/dirty trade and benefit from stronger freight rates in clean markets.

The outlook for 2022 appears to be a mixed bag, related to the line of argumentation in the dirty segment above. The anticipated Omicron repercussions do not bode well for clean activity, especially in Q1. Things may then look much better in H2 2022, with perhaps even some room for jet/kero demand to zoom in toward pre-pandemic levels. Approximately 10% of the LR tanker fleet is used in jet fuel transportation, with the majority heading to Europe.

Higher refinery runs in oil producing countries should support MR needs in the Atlantic Basin (US-stemming products) and LR utilisation East of Suez (Middle Eastern products). However, long-haul EoS/Atlantic Basin shipments may suffer somewhat. Further refining consolidation cannot be excluded in this context. Throughout 2021 we have witnessed an increase in LR employment from Asia to Australia, as domestic refinery closures have led to an increase in seaborne CPP volumes of the country, leading buyers to chase for greater economies of scale and cannibalising what has traditionally been an MR hunting ground. More of these changing dynamics are likely to emerge as refineries come into play in areas like the Middle East and shutter in regions such as Europe or Asia. However, MRs specifically are due a record number of deliveries in 2022, which could weigh down on rates as supply increases which leads us to looking at the supply equation of our freight forecast.

Supply: Overcapacity will keep a lid on rates in 2022

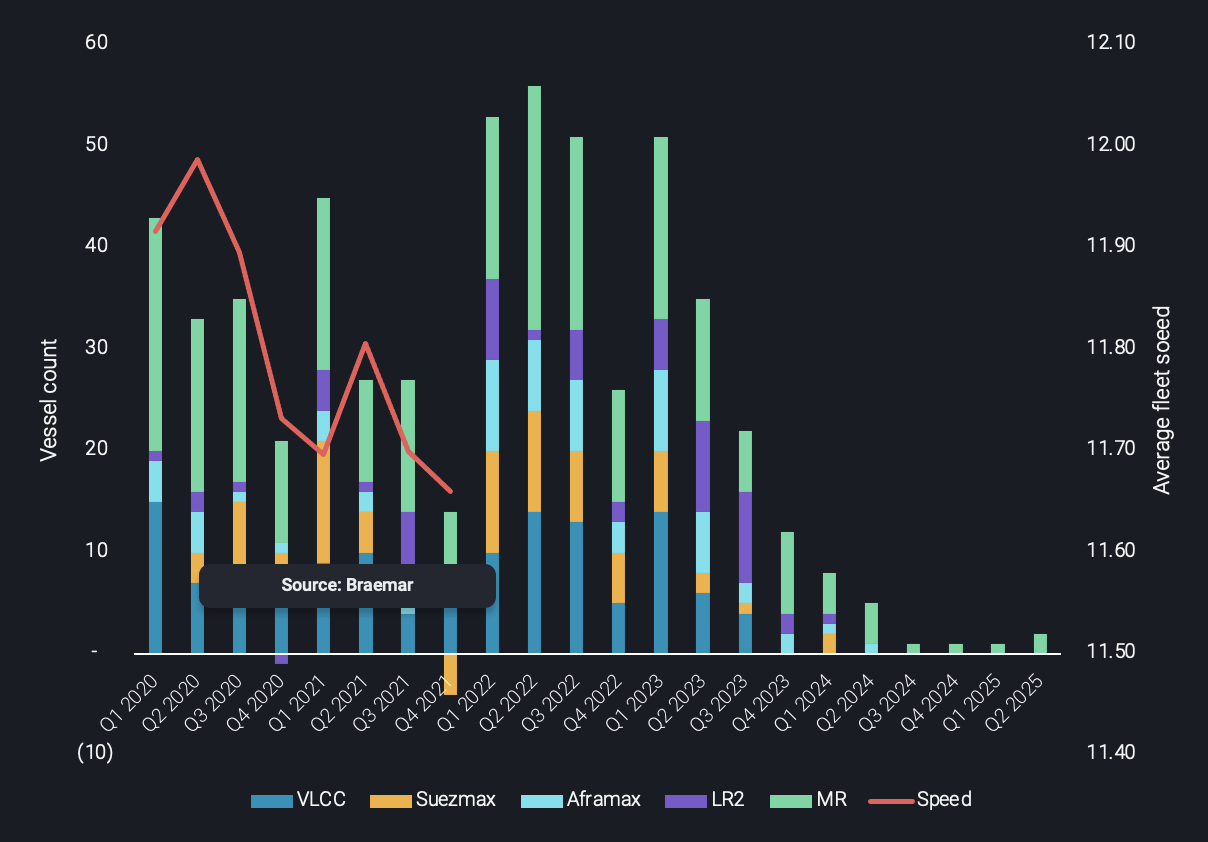

Net fleet additions by class vs. average fleet speed

When it comes to fleet supply, 2021 saw a net addition of 109 vessels across the 5 main tanker classes in focus, equivalent to approximately 3% of total fleet growth. The data in the chart above takes into account newbuild deliveries as well as demolitions and losses. The 2021 net addition is about a quarter lower than the levels experienced in 2020. Whilst all tanker segments saw their fleet size grow, Suezmax tankers saw a net decrease in Q4 of this year as scrapping accelerated slightly at the end of the year, as prices of scrap steel remained at decade-highs and freight rates low.

Whilst scrapping has started to show some promise with the number of tankers scrapped in the second half of 2021 accelerating, it would have to dramatically accelerate to counter the tsunami of newbuilds expected in 2022. A total of 186 tankers are expected to be delivered according to Braemar Research in 2022 across all tanker classes. The 3 largest crude/dirty tanker classes are all expected to see fleet growth in excess of 5% in 2022. Combined with market fundamentals that herald only limited demand upside and pre-existing overcapacity, we are about to witness a battering ram to any hopes of a strong recovery in the year ahead. When it comes to LR2s and MRs, similar numbers are expected as a percentage of their total fleet segment size.

Tanker market participants have resorted to slow steaming in a low rate environment as expected. Vortexa average speed data shows a drop in average speed of 2% across the global fleet. As the industry readies for a number of rapidly approaching deadlines to make ships more efficient and meet environmental guidelines, slow steaming could gather more “steam” as a practice, mitigating somewhat the impact of an increasing supply of vessels in the market.

One potential silver lining from the above chart lies in the indication that tanker deliveries are already expected as far out as Q1 2025. This is a direct result of the fact that shipyards are filled with newbuild orders from across the shipping spectrum, mainly containerships and dry bulkers, as strong market conditions have caused orders to skyrocket, utilising precious yard capacity and relegating tanker orders to 2025. If scrapping were to dramatically accelerate, with prices of steel remaining strong and market rates weak, this could provide a welcome push to tanker markets in 2023 and beyond. Until then, we forecast that H1 2022 will remain challenging for tanker markets, maybe more so for crude than clean segments. We do however believe there is light at the end of the tunnel and predict a recovery in freight rates and a more balanced market by H2 2022.

Review the year in Freight through Vortexa Market Intelligence

2021 Vortexa Freight Insights

Jan 20: LNG freight rates follow surge in exports

Feb 23: Altona’s refinery closure: Implications on trade flows and freight

Mar 4: Johan Sverdrup: Contrasting fates for crude tanker classes

Mar 11: US gasoline moulds the Atlantic MR market

Mar 19: Middle East LR2 tankers: Naphtha provides a lifeline

Apr 29: Oil markets on track to recovery? Only time (and freight) will tell

May 12: Mega shipments cannibalising the LR2 market

May 17: Crude tanker delays as cyclone hits WC India

May 26: Diverging trends behind stable supertanker utilisation

May 27: European naphtha exports boost LR2 demand

Jun 2: Suezmax tankers infiltrate Europe-bound transatlantic crude flows

Jun 10: Planned storm still only a breeze in tanker markets

Jun 16: Question marks for freight rates in a largely supportive global LNG picture

Jun 23: $100 barrel of crude: boon or bust for tanker markets?

Jul 8: The curious case of declining VLGC rates – a blip or a trend?

Jul 14: LR2s keep “cleaning” up throughout 2021

Jul 22: OPEC+ decision: a zero-sum game for VLCCs

Aug 11: Crude tonne-miles: SE Asia & India pick up the slack where China left off

Aug 25: Naphtha persistence lifts LR1 tanker rates in the Middle East

Sep 2: VLCC clean maiden voyages: a trend coming to an end?

Sep 8: Collapse in West African supplies hits dirty freight segment hard

Oct 14: Scrubber-fitted VLCCs quietly gain market share

Nov 11: Tonne-miles need to pick up to sustain rally in dirty freight rates

Nov 25: Clean tankers battle it out in the Atlantic and the Middle East

Dec 2: Omicron obscures outlook for tanker markets

2021 Vortexa Freight Events & Reports

Jan 28: Opportunities in crude freight and storage markets

Feb 10: Stranded at sea: The forgotten victims of the COVID crisis

Feb 24: Driving freight forward presented by Reuters Events & Vortexa

Feb 25: Identifying trading opportunities through oil tanker shipping routes

Apr 7: Q1 2021: Freight market update

Apr 28: The Rise of freight analytics with Argus, Windward and ZE Powergroup

Jun 16: Diving into energy shipping dynamics with Vortexa freight analytics

Jul 1: Q2 2021: Freight market update

Jul 12: The effects of analytics on the maritime industry

Sep 22: Freight markets – a recovery atop a house of cards

Sep 23: Shipping is navigating through uncharted and uncertain territories

Oct 7: Q3 2021: Freight market update

Oct 8: Redefining trading strategies with China’s new oil regime