Are tankers bound to take a breather, or will the party continue post-Posidonia?

As Posidonia 2024 kicks-off and we approach the second half of the year, we examine key trends that have influenced the tanker markets and draw conclusions about the future from Vortexa flows, freight and inventory datasets.

Dark/grey trades, high CPP exports and longer voyages are leaving idle counts low for all vessel classes but one

The summer season is upon us, and the shipping community celebrates by gathering at Posidonia after a turbulent first half of the year. This turbulence looks to have left shipowners and ship operators largely net-positive when looking at freight rates. Geopolitical developments triggering longer voyages, record-high clean exports and the persistent utilisation of “grey” old vessels in opaque trades, are all factors that have kept idle tankers low and hence kept fleet requirements quite tight.

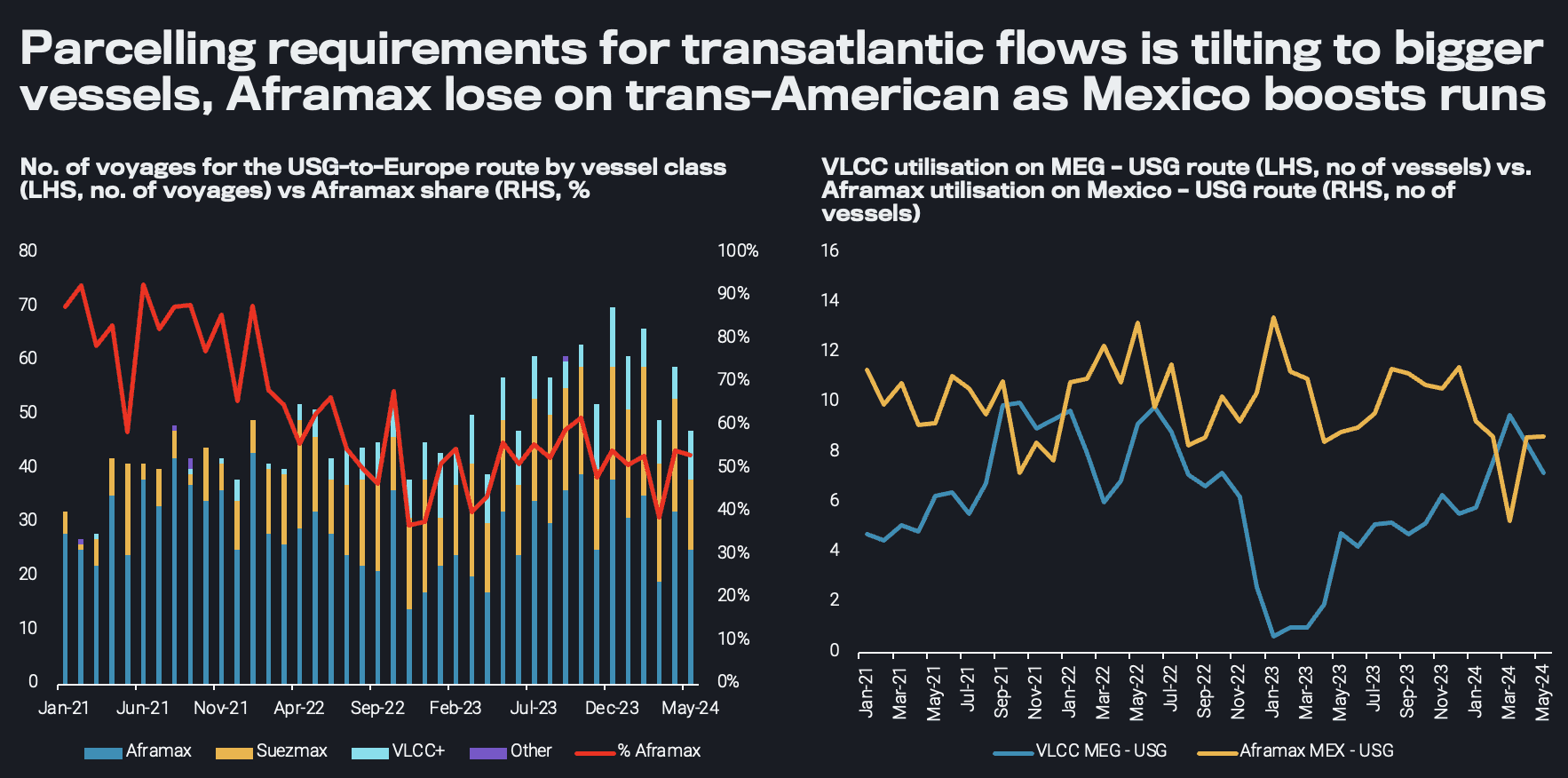

This is true for all main tanker classes bar one – Aframaxes. It is not a coincidence that this is the only segment where freight rates hover below 2023 levels currently. The reasons for the fall are varied:

- There are structural changes on trade patterns as Suezmaxes have eaten up Aframax market share not only for flows towards Europe where parcelling requirements are increasing, but also out of Russia since the Russian-Ukrainian conflict.

- Increasing sanctioning activity on the crude side is driving Western Aframax operators away from the long-haul Russian voyages.

- More recently, the vessel class has taken a hit on Intra-Americas voyages as Mexican refineries have ramped up runs, reducing exports to the US, which in turn sources Middle Eastern crude on VLCCs as a replacement. Whether this is a long-lasting or a short-term effect driven by the Mexican elections as the country seeks to become energy self-sufficient remains a question mark. Recent outages in the Mexican refinery system highlights the country’s difficulty in sustaining high refinery utilisation rates, yet the current drop in Aframax employment could be also seen as a sneak preview for the prospective start-up of the Olmeca refinery.

This makes the TMX expansion paramount for the support of Aframax employment. According to our base case scenario, we expect 12-16 Aframaxes to be laden per month, mainly operated in the Vancouver-to-PADD 5 route. But if most voyages are short within the US West Coast, then the uplift on ton-miles would be limited (read more here). For now, however, only 7 vessels are signalling toward Vancouver to load, which nevertheless is a record-high.

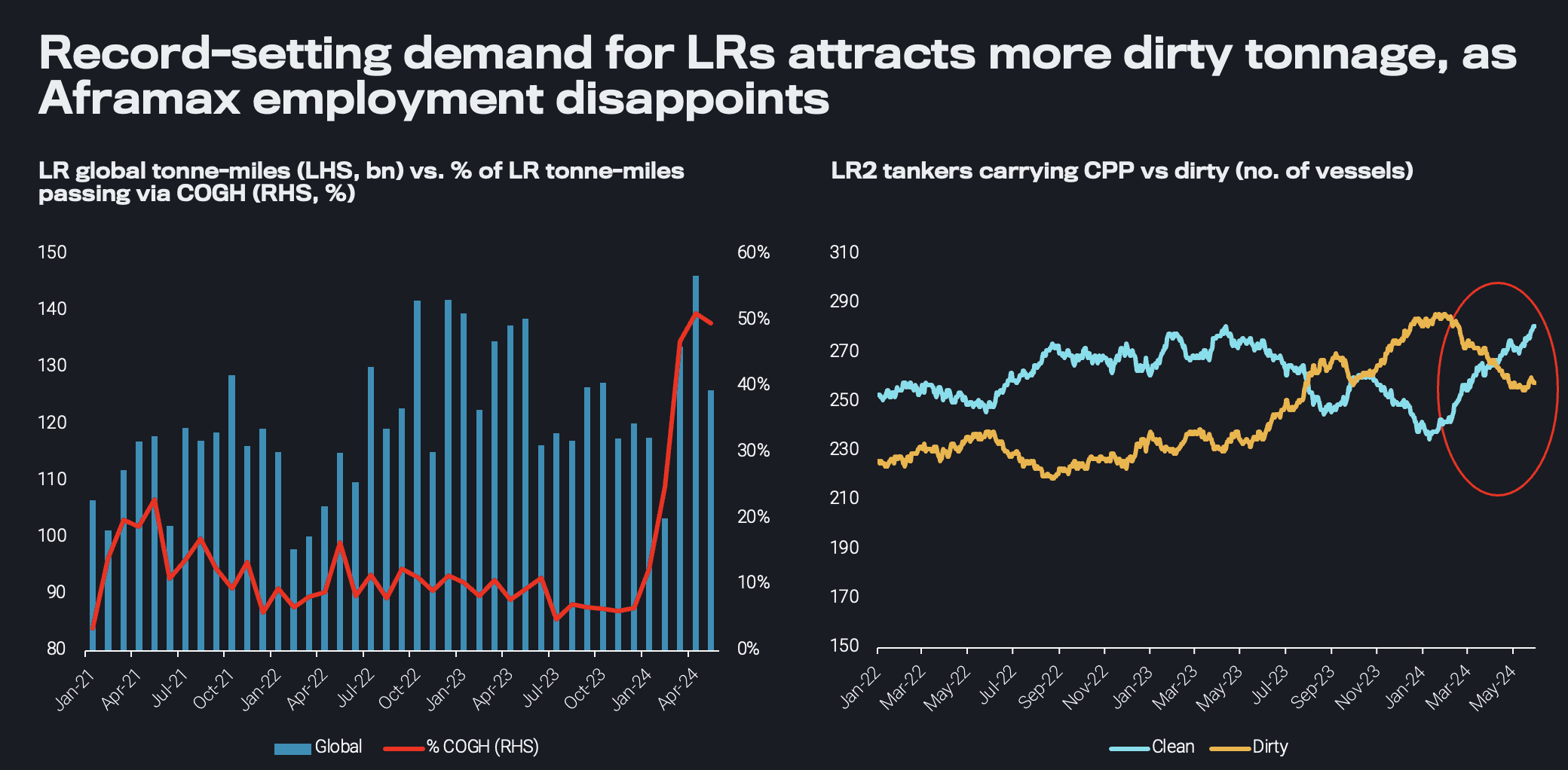

LRs thrive on reroutings, but ample CPP supplies will likely cap a further upside

Undoubtedly the vessel classes that have taken the spotlight from the beginning of the year have been LRs. The segment found its strength from the onset of the Red Sea attacks which triggered sailings via the Cape of Good Hope (COGH). The segment continued its momentum as the Middle East ramped up exports to the Atlantic Basin post-seasonal refinery maintenance, which led to record highs of East of Suez exports to the Atlantic Basin for March and April.

As a result, almost 50% of the global tonne-mile contribution for LRs is generated from these COGH routings. Moreover, the lack of traditional LR cargoes in the Atlantic Basin are forcing long ballast backhauls, tightening availability and keeping rates high. The replenishment of this supply at a time where deliveries are remaining at historical lows, is coming from “cleaning” up Aframaxes/LR2s operating in the dirty sector. This makes economic sense for owners as long as Aframax earnings are faltering in comparison to their clean tanker counterparties.

Nevertheless, East to West volumes can be the Achilles heel of LR2 rates, as the sector increases its reliance on these flows. In May, motor fuel exports have subsided from record levels, pointing towards an oversupplied Atlantic Basin reflected by weaker cracks, and a closed East/West arbitrage at a time where new refineries such as Dangote could further affect available demand in the region. Although unlikely, a prospective ceasefire between the Houthis and the West could mark the resumption of LR transit via the Suez, which would bring LR average voyage mileage down by around 20% from April levels, shrinking transportation requirements and causing rates to plummet. While currently there is not an indication of a ceasefire with CPP tanker transits remaining at their lowest, this underpins the fragility of current high levels of LR tanker rates.

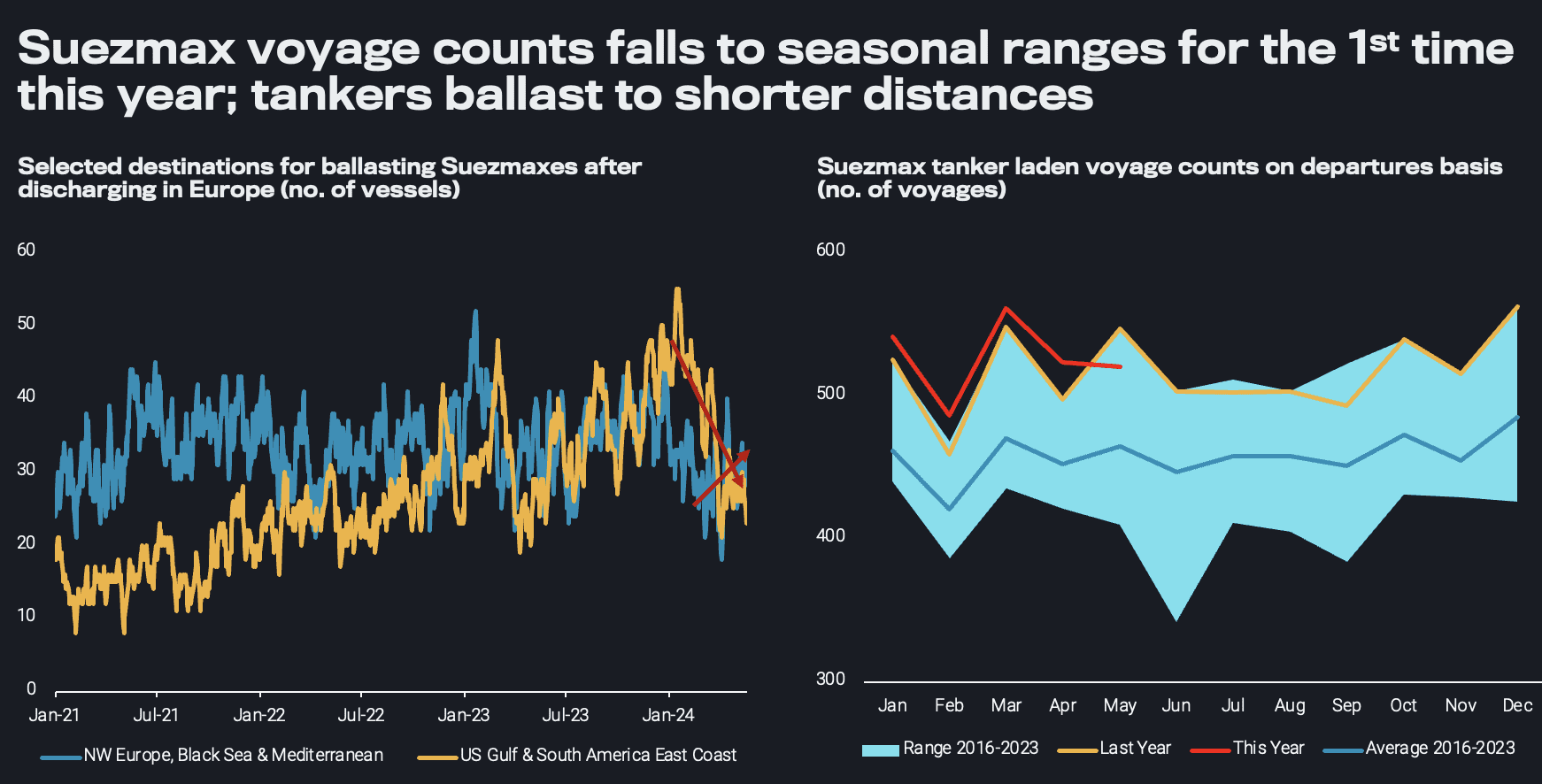

Non-OPEC supplies have stepped up, but Atlantic Basin supplies might take a breather for the remainder of the year, limiting Suezmax gains

OPEC’s meeting – unsurprisingly for many – resulted in the extension of the cuts with crude prices falling from 91$/bbl 2 months ago to 81 $/bbl currently, as declining refining margins are picturing a softer demand outlook. However, the eight countries contributing additionally via voluntary cuts met in Riyad, discussing amid others compliance. There is a scaled unwinding of these cuts and extra quotas for the UAE, resulting in a target level for Saudi Arabia and the UAE that is nearly 1.5mbd higher in September 2025 than in September 2024. Looking at the supply-side of OPEC member countries, these ones with relatively new and efficient refineries (Oman, Kuwait, Nigeria) are converting their production to CPP exports, thus bringing crude exports from these 3 countries down by 600 kbd since the start of 2023 when Al Zour commenced export.

Conversely, non-OPEC supply has stepped up production with exports of 3 countries (the US, Brazil and Guyana) playing a key role in providing a boost to Suezmax voyages (especially after the unwinding of Europe’s dependence on Urals) and support for VLCC mileage. Although potential growth from these three countries can provide further upside in tonne-miles in the long-term, the rampant increase of exports might pause for the remainder of 2024. This is illustrated by looking at the 3-month trend, following record exports in January of this year.

According to reports, Brazilian production is poised to remain flat y-o-y on 2024. In the US, the number of drillings are coming down, with production companies instead focusing on increasing dividends to provide shareholder values. In Guyana, not only will the extension of production units come online from 2025 onwards, but two out of there existing FPSOs (Liza and Unity Gold) will undergo maintenance in July.

On the other side of the Atlantic, European crude imports have come down in May (read more here) dropping Suezmax total voyages within seasonal ranges for the first time this year. Weak oil demand in the continent is also highlighted by the 2-year highs of North Sea crude. Lower transatlantic utilisation for the vessel class as wells more expensive Aframax Cross-Med rates has seen Suezmax operators increasingly looking for cargoes in proximity regions such as NW Europe, Black Sea, or North Africa (Med) instead of the Atlantic Basin, which in turn will force a decline in tonne-miles.

Chinese weak domestic demand, soft margins and a big portfolio of sources to choose from, might deter exposure on US crude, limiting tonne-miles for VLCCs

This leaves VLCCs, which have seen rates throughout a big part of May performing a mini-rally on the back of higher voyage mileage driven by lower European buying interest for WTI and favourable arbitrage economics coupled with tighter vessel supply in the Atlantic Basin. The first two points can provide a pocket of strength for VLCC owners going forward, especially for countries such as South Korea and Taiwan with refineries coming back online post-refinery maintenance season, although increased product arrivals in Asia-Pacific point to oversupply, which could bring more refining run cuts and hence a cap on purchasing activity (read more here)

The outlook for Chinese crude imports is muted at best. Chinese-bound loadings increased over April and May, as China seasonally raises exposure on the longer-haul cargoes amidst refinery maintenance. However, these traditionally drop during the summer months, as China state-refineries return to their base load Middle Eastern and West African barrels. Currently, Chinese crude inventories are gradually building with a relatively unchanged rate of imports (read more here), indicating weak margins. Additionally, these margins are particularly weak for light distillates, thus deterring demand for light-sweet grades such as WTI. In this case it will be interesting to see whether the ripple effect from the TMX pipeline expansion could divert certain medium-sour crudes from WC Latam to China, providing a silver lining to VLCCs.

Conclusion

To summarise, there are numerous moving parts that can determine the fate of tankers for the second half of the year, as the volatility (in rates) has become the new normality. There are undoubtedly supporting pillars that will provide a floor to rates and will keep them away from 2021 realities (longer distances from reroutings caused by the EU ban on Russian oil and Red Sea attacks). However, there are certain aspects such as an oversupplied clean market in Europe and the Pacific, an effort of energy self-sufficiency from traditional net CPP importers, a mixed crude supply outlook amid poor refinery margins, as well as an uncertain outlook in China that could shake the current foundations and threaten current freight rate levels.