Naphtha & LPG: Falling freight rates suggest flows will remain curtailed

In this insight we’ll analyse the main drivers behind the decline on naphtha and LPG freight rates drop as well as what’s in store for the future.

Naphtha and LPG freight rates have been on a decline the last couple weeks, quite contrary of the performance seen during the last quarter of 2021. In this insight we’ll analyse the main drivers behind this drop as well as what’s in store for the future.

Vessels carrying the competing petchem feedstocks of naphtha and LPG saw a positive freight rate performance in Q4 2021. This joyful ride was appreciated by shipowners on the back of strong demand from Asia, and was underpinned by the multi-year high seen both on propane and naphtha prices. The main two vessel classes involved in these trades are the LR tankers and the VLGC carriers.

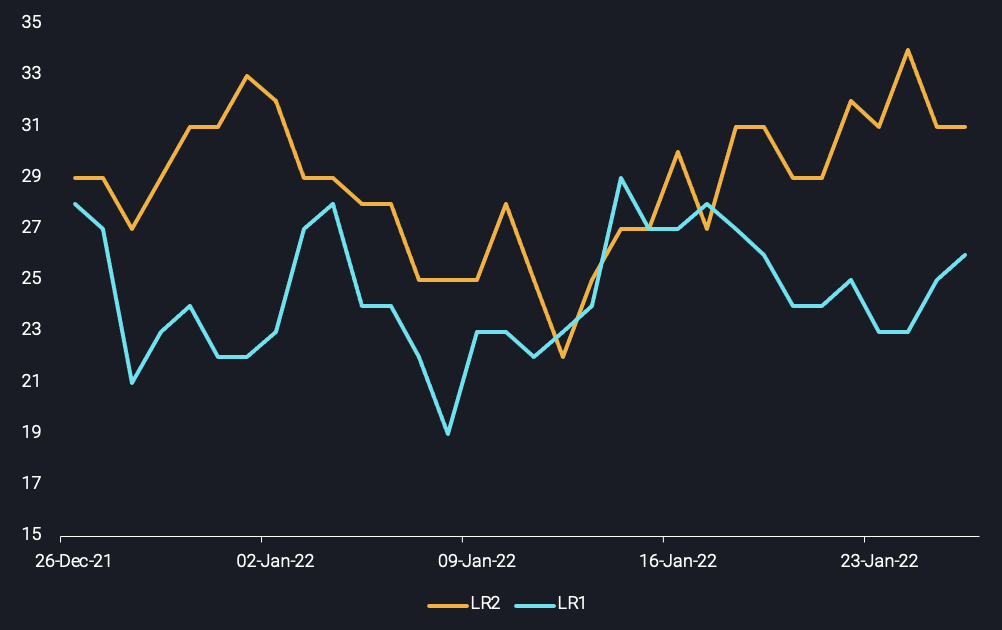

Yet both of them are experiencing a bumpy road in 2022. Looking at our Vortexa freight pricing screen:

- LR1 and LR2 freight rates for the Middle East Gulf – East Asia (TC1 & TC5) routes dropped by around 25% and 40% respectively from the mid-December peak

- VLGC rates for USG – East Asia and Middle East Gulf – East Asia declined by 15% and 20% respectively from the mid-January peak

This begs the question whether this ubiquitous freight rate decline is linked with a demand drop for the underlying cargo carried, or if any developments on the vessel supply side are to blame.

Demand – Falling exports on both fronts

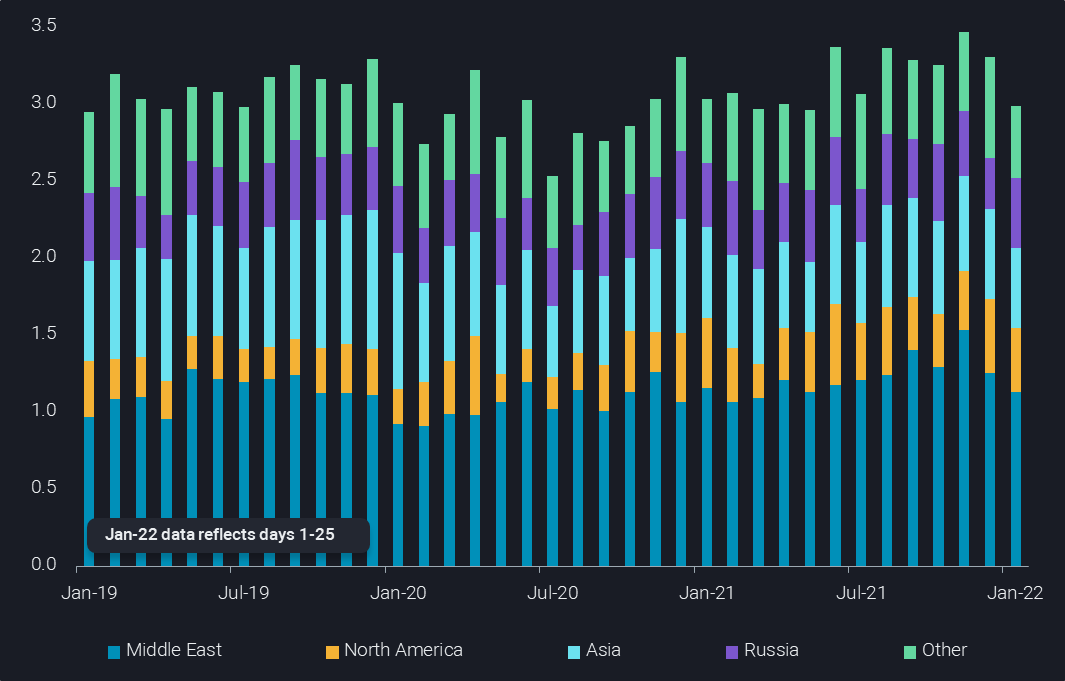

Global naphtha loadings are on a downward trajectory, when looking exclusively at the bigger ship classes of MR and LR tankers. The Middle East is the main culprit, with 1.1mbd of monthly liftings being close to a 1-year low, according to Vortexa’s preliminary data.

Global naphtha liftings on MR and LR vessels by origin (mbd)

Naphtha cracks are trending lower throughout January across the board (Argus Media). This in combination with falling exports gives validity to the reports of poor olefin and aromatic margins – below breakeven levels – which forces steam cracker operators to reduce their runs.

A drop in cracker runs is also a concern for LPG sellers, but this is not the only issue for VLGC owners. The arbitrage between the US Gulf and East Asia has narrowed recently. This is on the back of falling US propane stocks due to priorly higher levels of exports out of the US Gulf but also owing to domestic consumption. According to the EIA, propane stocks are on a downward trajectory since the end of October, currently at 20% below 5-year average levels. The drop in the arbitrage spread has limited spot chartering activity, with a respective knock-on effect on VLGC rates. This is also reflected in less LPG on water heading toward Asia, as displayed in the chart below.

LPG-on-water towards Asia, by origin (mb)

Supply: Increasing availability also pressures rates

While it is safe to say that cargo demand is the main contributing factor to the dip of both naphtha and LPG freight rates, the vessel supply-side has also had an active role, especially when it comes to LR2s and VLGCs.

Vessel availability for LR2s in the MEG continues to increase, exerting further pressure on TC1 freight rates. On the other hand, a more stable tonnage list on LR1 tankers out of the region has helped owners to display a level of resistance as TC5 rates have remained rather flat in recent weeks.

LR1 and LR2 availability in the Middle East (no. of vessels)

For VLGCs the situation is similar. US market participants are looking to resell rather than lift cargoes. As a result, vessels involved in term trades are becoming available for relets, entering the spot market and thus raising availability. At the same time, waiting times in Panama have been negligible in recent weeks when compared to the highs seen in Q4 2021, failing to provide any support on freight rates out of the USG. However, congestion has started to pick-up: 24 VLGCs are waiting in the Panama canal, a w-o-w increase from the 13 that were seen previously.

Outlook: Lower supplies will likely cap rates

Despite this pick-up, there are other hurdles in the way of a LPG and naphtha freight rate increase, which have a common denominator: lower cargo supplies. On naphtha, reports have surfaced on a strong Q1 2022 refinery maintenance schedule in the Middle East, which in turn will limit available naphtha and LPG volumes for exports. As for the US, the low propane inventory levels and still a number of weeks left with peak seasonal demand, limit supply for exports. This will weigh on LPG export activity and limit West – East arbitrage options.

More from Vortexa Analysis

- Jan 26, 2022 Reality check on Russian oil and gas sanctions

- Jan 25, 2022 China’s crude destocking pauses. Is it looking for a refill?

- Jan 20, 2022: Maiden Crude Tanker CPP Voyages: What happened and what to expect

- Jan 19, 2022: Oil price rally is driven by lack of supply right now

- Jan 18, 2022: Global diesel market pricing in tighter supplies ahead

- Jan 13, 2022: Omicron: pre-emptive supply cuts & resilient demand draw stocks and lift prices

- Jan 12, 2022: Mediterranean light crude: volumes limited and sold locally, weighing on freight demand

- Jan 11, 2022: China sets tone for refiners with tight oil quotas in the new year

- Jan 6, 2022: Global crude exports end 2021 on a high

- Dec 31, 2021: Making Waves: Looking back at a year of Freight

- Dec 22, 2021: Omicron infiltrates tankers in the Atlantic basin