The curious case of declining VLGC rates – a blip or a trend?

Despite a really strong, unseasonal LPG price hike, VLGC rates are following a different path. Vortexa attempts to shed a light on this divergent pattern.

Despite a really strong, unseasonal LPG price hike, VLGC rates are following a different path. Vortexa attempts to shed a light on this divergent pattern.

As we enter Q3 2021, there is clear evidence of the products that are currently outperforming, and these belong to the lighter end of the barrel. More specifically, naphtha and gasoline cracks are on an upward trajectory across the globe. Apart from the uptick in driving, this is attributed to robust demand stemming from the petrochemical industry, which uses naphtha as a main feedstock. As a result, Asia naphtha prices have reached their highest values since October 2018.

Having said that, however, a surprising detail lies elsewhere. Unlike seasonal norms, a key competitor to naphtha in the petrochemical industry, LPG, is currently at a premium to naphtha. This is a clear indication that the demand for LPG is currently steaming hot and as a result has driven US LPG exports close to an all-time high, at 5.15 mn tonnes.

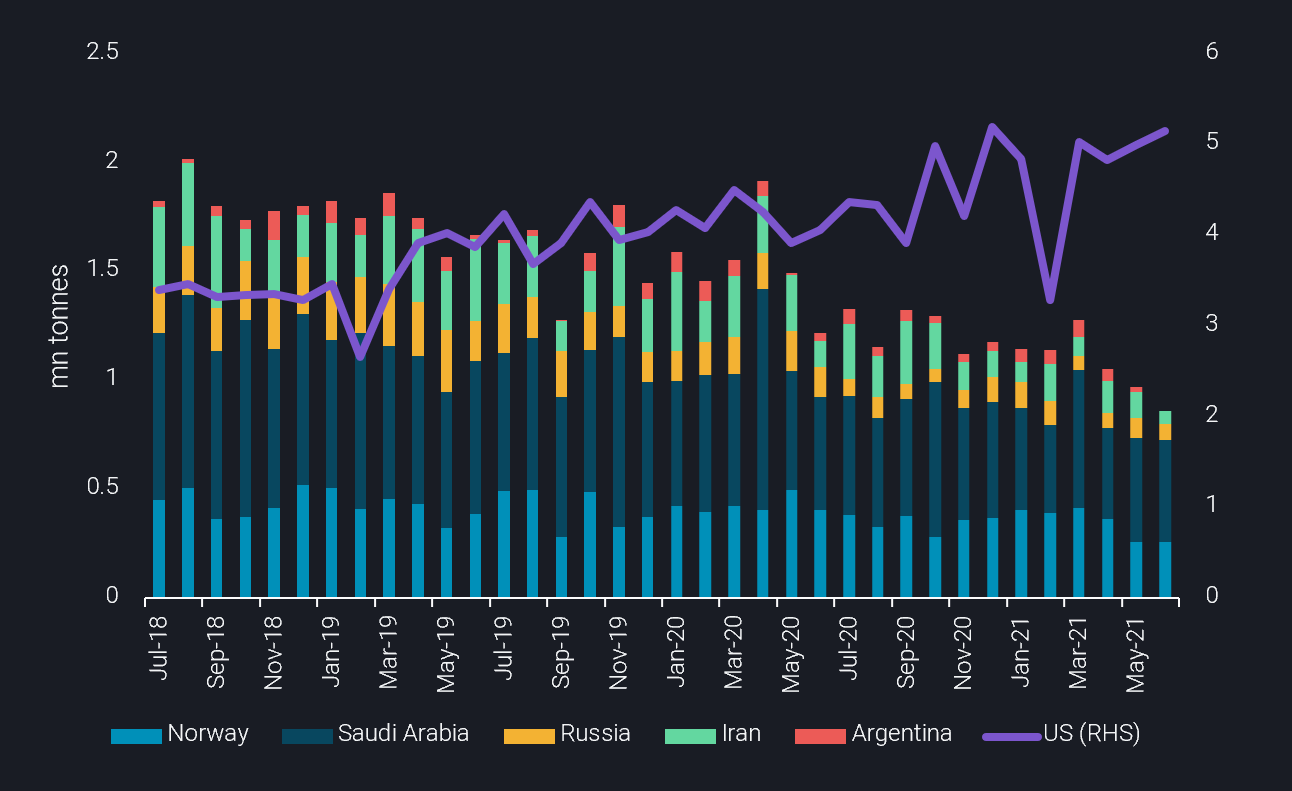

This development comes at a time where other key export markets located in different geographic locations have seen their volumes decline drastically over the past 3 years, as it is displayed in the graph below. Conversely in the US, according to EIA, LPG stocks are 15% below the 5-year average, as domestic and Asian players are scrambling to book supplies.

LPG exports for selected countries (mn tonnes)

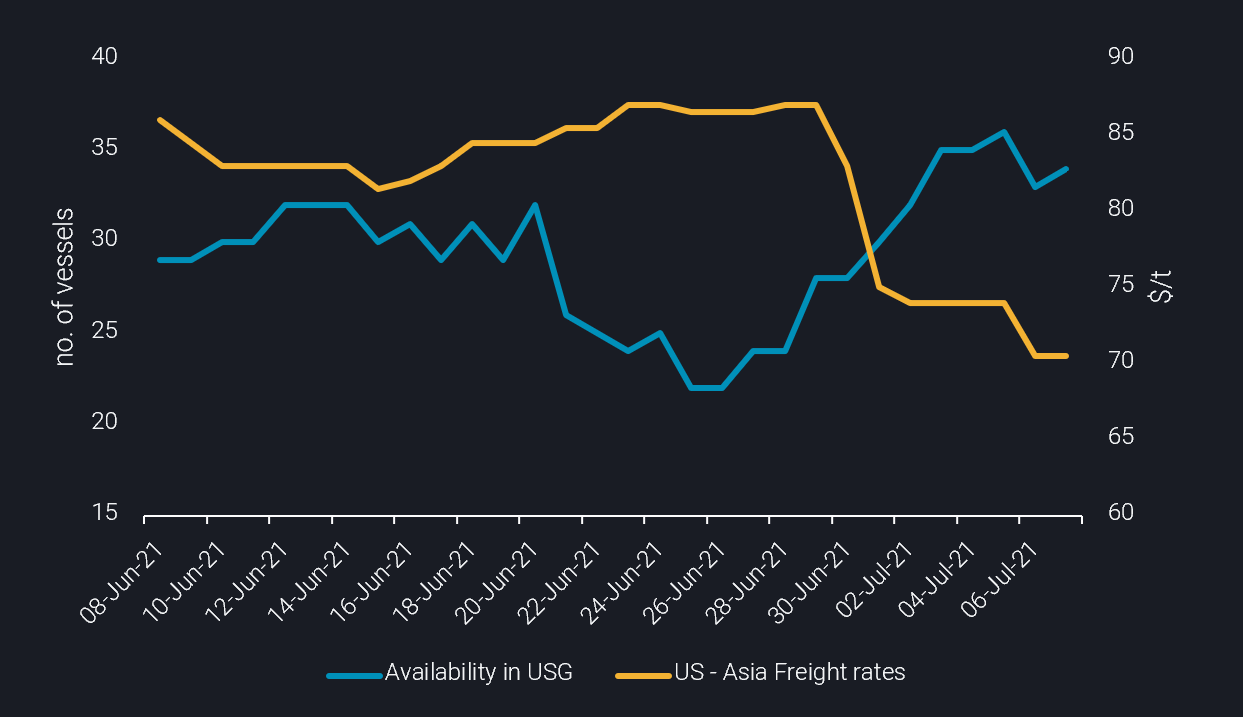

Despite the strong fundamentals present in the US market, freight rates showed a diverging behaviour since the end of June. In particular, VLGC rates from Houston to Chiba dipped by 15%, throughout the week ending July 4, according to Argus Media price assessments.

The reason behind this drop lies on the freight supply side. The 15-29 day forward availability of VLGCs in the US Gulf, which in essence captures carriers ballasting from East Asia or Europe towards the US, is on an upward trend since the end of June. This ultimately gave greater negotiating power to charterers in lowering the freight rates.

VLGC Availability in US Gulf (no. of vessels) vs. VLGC US – Asia Freight Rates ($/t – Argus Media)

Nevertheless, the rally in LPG prices – at a premium to naphtha – underpins the strong demand with increased competition from LPG buyers against a backdrop of limited supply globally. These factors signal sustained long-haul flows for the weeks and months to come. These flows will translate into continued strong VLGC demand, supporting rates once more, and indicating that this peculiar drop is likely just a temporary blip in a fundamentally strong LPG market environment.

Click here to register for a trial of Vortexa Freight Analytics

More from Vortexa Analysis

- Jul 7, 2021 Illustrations of naphtha and gasoline strength

- Jul 1, 2021 Q2 2021: Freight Market Update

- Jun 29, 2021 Two truths – why OPEC+ is hesitant

- Jun 24, 2021 Surging diesel flows – a pull or a push?

- Jun 23, 2021 $100 barrel of crude: boon or bust for tanker markets?

- Jun 22, 2021 Global jet fuel recovery running late, US emerging as bright spot