Strong Med CPP import demand in Q1 may ease over April and May

The Wider Mediterranean outperformed the rest of the world in terms of clean product imports in Q1, but strong crude imports and limited refinery maintenance suggest regional supplies may be ample. This is likely to lead to lower imports in spite of strong supply potential from players east and west.

Over recent months, we have commented frequently on weak product import demand pretty much across the barrel and across regions. Overall this trend is still in place albeit March indications so far suggest that the development may have bottomed out in February (see right hand-chart below).

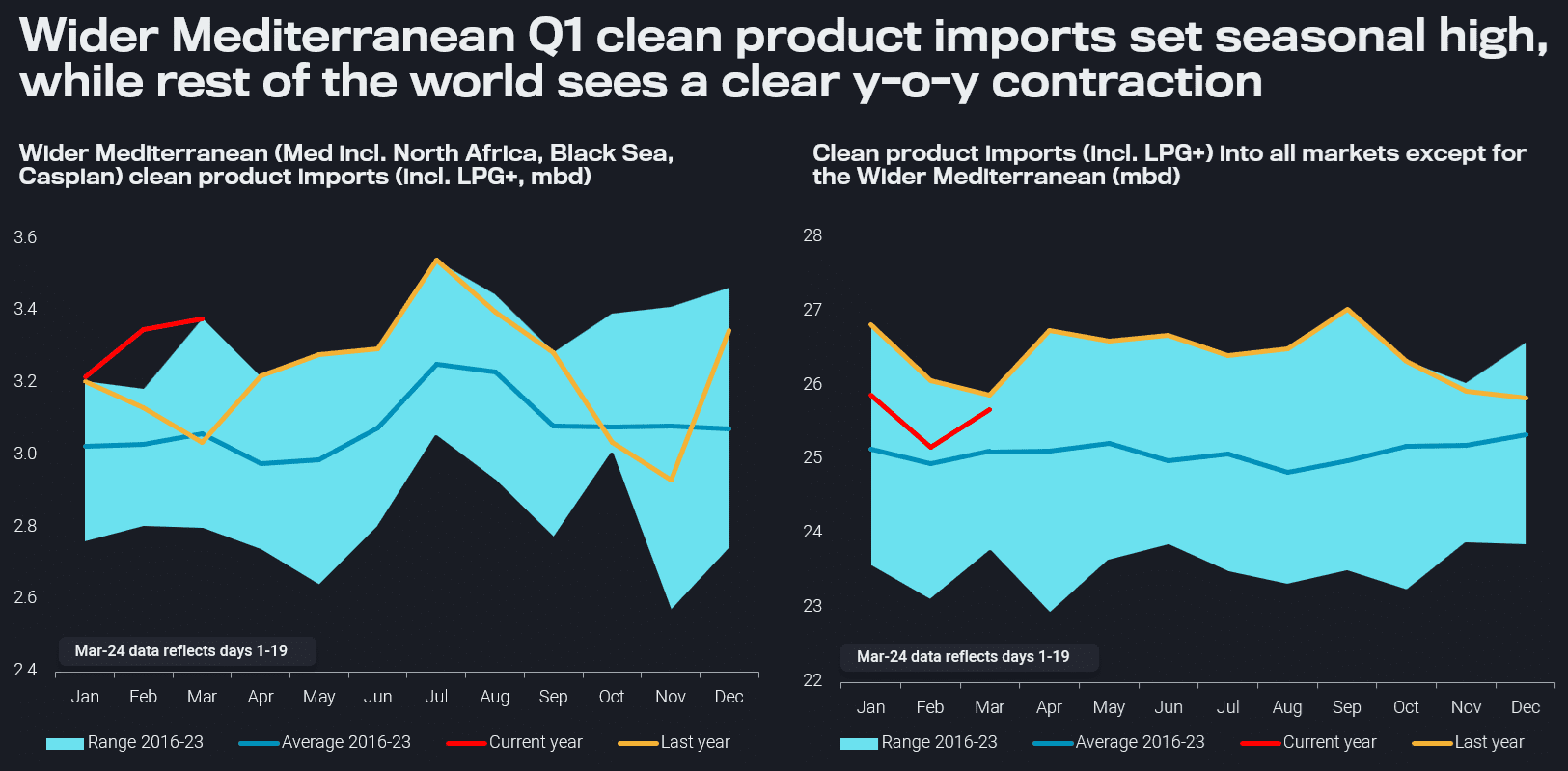

But one of our eight new wider shipping regions is clearly standing out in Q1 – the Wider Mediterranean (Med incl. North Africa, Black Sea and Caspian). After a weak Q4 2023 – especially in October and November clean product imports slumped below the seasonal norm – Q1 2024 registered much stronger values. Clean product imports for the Wider Med set or touched the seasonal high since 2016 in every month in Q1.

Clean product import demand into Wider Mediterranean and all other seaborne markets (mbd)

Meanwhile, looking at all other regions than the Wider Med shows that every month over Jan-Oct 2023 set a new seasonal high, but since then the trend is clearly southwards. On average, Q1 clean product imports have been down by 700kbd or 2.8% in these markets.

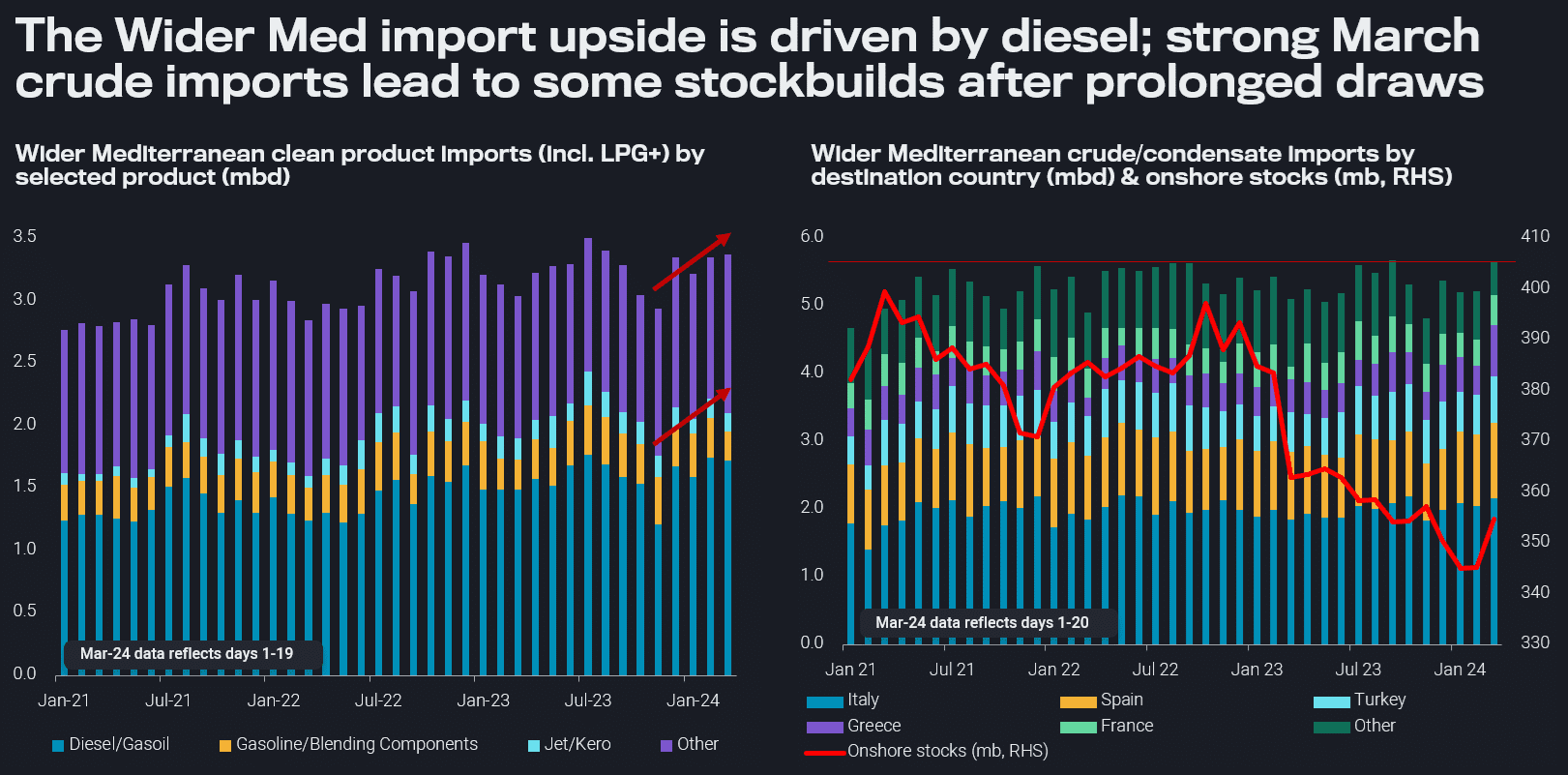

Coming back to the Wider Med, the pick-up in clean product imports has been driven by diesel. The start of the agricultural season may have played a role. Looking forward, seasonality heralds the lowest import levels in the months of April and May before imports surging in the summer, spiking around July.

Wider Mediterranean clean product imports (mbd), crude/condensate imports (mbd) and crude/condensate onshore inventories (mb)

There are some indications that product imports may drop lower also this year in April and May. Firstly there is not much refinery maintenance coming up. The extended works at the Priolo refinery in Sicily, Italy, only affect the minor 80kbd northern unit (Argus Media). Otherwise we are not aware of a lot of work coming up, albeit Argus points out that quite some refiners are working on heat exchangers to make units fitter for likely heatwaves over summer. Secondly, crude imports have surged to the high end of the historical range over March 1-19, leading to the first significant stockbuilds in a long stretch and suggesting higher refinery runs in the coming weeks.

However, product markets are much more competitive now than they used to be, so far in the Ukraine war era, and especially the Wider Arabian Sea is exporting growing levels of clean products. The US Gulf Coast refining system is also under stress to place its products amid deteriorated economics East of Panama, while any supplies from Dangote would add to ample supplies.

Accordingly, refining economics may be a bit more challenging, but European players enjoy two key facts:

1) The highest distillate prices in the world due to their massive short, with higher transportation costs from the Wider Arabian Sea via the Cape of Good Hope adding to the price level in Europe

2) Ample available crude supply options, with the boost in American supplies benefiting in particular players within the Atlantic Basin