VLCC Clean Maiden Voyages: a trend coming to an end?

As CPP volumes on crude supertankers decline, Vortexa analyses the main factors of this occurrence and provides a view on the future of VLCC and Suezmax clean maiden voyages.

As CPP volumes on crude supertankers decline, Vortexa analyses the main factors of this occurrence and provides a view on the future of VLCC and Suezmax clean maiden voyages.

As the summer period comes to a close in the northern hemisphere, there are concrete conclusions that can be drawn with regards to the strength between crude and clean product flows in 2021.

On the one hand the alleviation of lockdown measures, especially in the Atlantic Basin saw a rise in transportation demand which in turn propelled higher CPP volumes. The imbalance in consumption and demand between regions due to the pandemic widened geographic pricing differentials that also supported trade demand. As a result, global CPP flows for 2021 are currently at 27.4 mn b/d, up 5% from last year while edging closer to pre-pandemic levels seen in 2019.

On the other hand, a multitude of factors such as the OPEC+ production cuts, elevated crude inventories and the recent introduction of lower crude import quotas from China, have put a ceiling on global crude flows. Evidently, these have decreased for the 3rd consecutive year, currently at 36.7 mn b/d, down just 2% from 2020 but 10% from the pre-covid era. Unavoidably the lower crude flows have impacted negatively the freight market. This can be reflected in the persistently low freight rates on supertankers, such as VLCCs and Suezmaxes.

The relative strength of CPP versus crude oil flows coupled with the lower crude freight rate environment has paved the way for an increased activity of maiden VLCC and Suezmax voyages that carry CPP cargoes, mainly diesel/gasoil from East of Suez to West Africa.

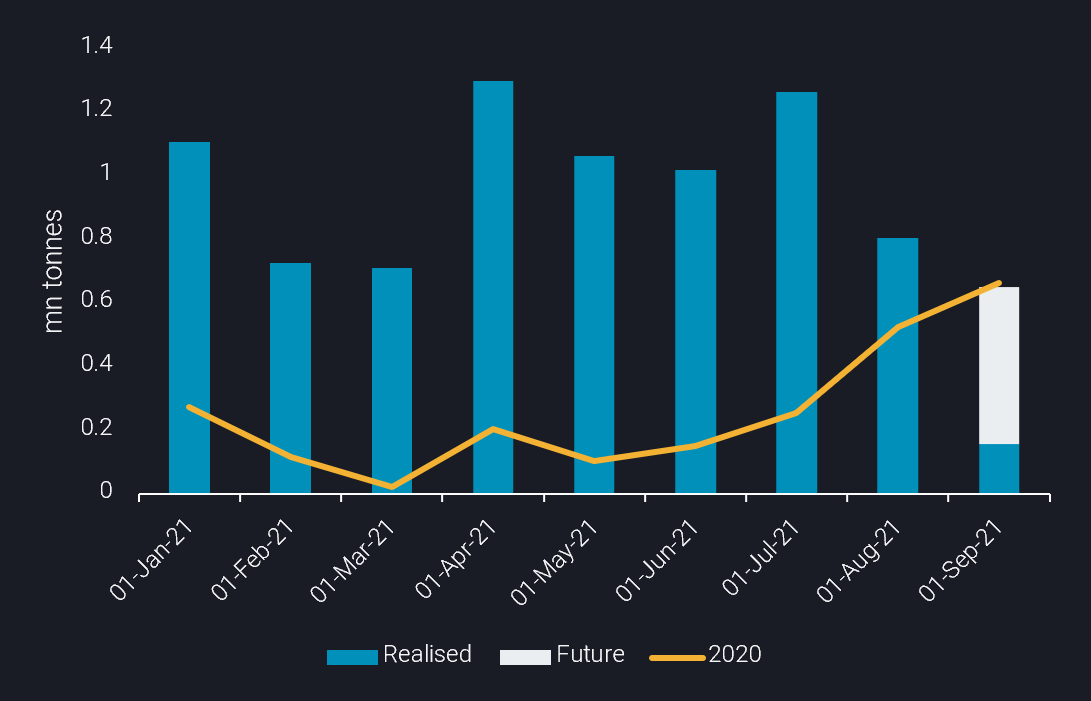

According to Vortexa data so far in 2021, 8.14 mn tonnes (or 61 mn bbls) of clean products have been carried on these tanker classes, corresponding to around 70-100 fully laden LR2s which were eventually displaced. For the sake of being more granular, the graph below indicates that the majority of the activity took place in Q2 2021 and continued strongly in July on the back of a strong diesel demand in Latin America before declining in August.

CPP Volumes carried on newbuild VLCC and Suezmax tankers (mn tonnes)

It begs the question whether this decline indicates the end of the clean maiden voyage trend? The answer tends towards the no, as the drop in CPP loadings on VLCC and Suezmax tankers is not due to economics of the trade. Instead, the reason behind the drop is the lower number of vessel deliveries that took place throughout the summer – a cyclical event in shipping – which had a direct impact on the CPP volumes onboard crude supertankers.

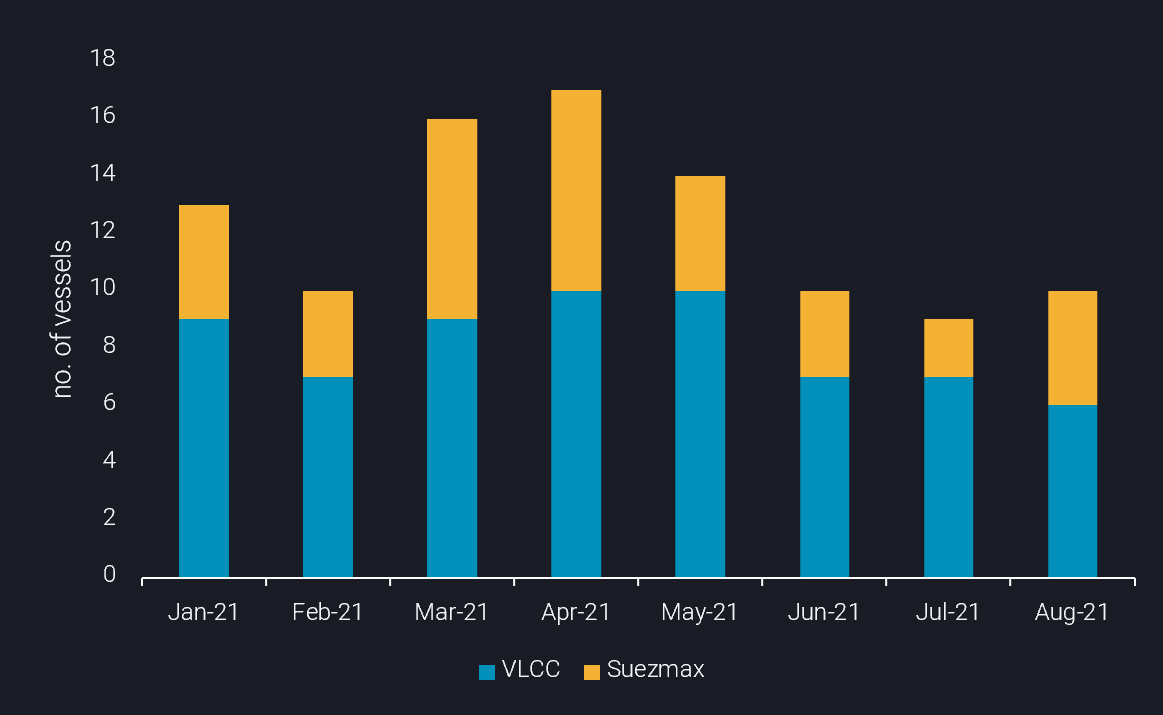

To put the perspective in numbers, 23 VLCC deliveries occurred in Q1 and Q2 2021 while just 4 deliveries took place in Q3. In a similar fashion 18 Suezmax tankers were materialised in Q1-Q2 2021 and only 2 in the current quarter. Currently, there are 5 VLCC and 4 Suezmax tankers in transit carrying clean products.

VLCC and Suezmax average utilisation per month (no. of vessels)

In addition, there are also a couple of indications sourced by the Vortexa platform showing that the CPP voyages on crude tankers are continuing apace:

- Two VLCCs that hit the waters in the month of August, NAVE ELECTRON and MARAN ANTIOPE are currently signalling Singapore. This is a traditional location where VLCCs are loading diesel/gasoil via STS before sailing westward, hence there is a likelihood that both vessels could be involved in CPP trades.

- On the back of the reduction on the newly-built VLCC deliveries, there are cases where vessels are performing more than one voyage carrying CPP. Such is the case of the HUNTER DISEN which loaded diesel/gasoil in Rotterdam and is expected to discharge in Lome, Togo.

So far, 13 out of the 25 VLCCs delivered in 2021 loaded a clean cargo. Looking ahead, 10 VLCCs are expected to enter the market for the remainder of the year, which is considerably less than the numbers achieved in H1 2021. However, current dynamics continue to signal a weak crude freight landscape. Import demand from China – the raison d’etre of VLCCs this century – remains limited, while on the supply side, scrapping activity is subdued throughout the year with only 5 VLCCs heading to scrapyards, despite high scrap prices, according to Braemar ACM. These two pillars will likely continue to exert a pressure on crude tanker employment and hence freight rates, setting the appropriate conditions for CPP maiden voyages on crude tankers to resume.

Vortexa customers can track newbuild vessels carrying CPP using the links below:

More from Vortexa Analysis

- Aug 31, 2021 Physical reality check: How strongly are Asian oil flows affected by COVID-19 waves?

- Aug 26, 2021 Summer of 2021 brings LNG players heatwaves, empty dams and a longing for Nord Stream 2

- Aug 25, 2021 Naphtha persistence lifts LR1 tanker rates in the Middle East

- Aug 24, 2021 Physical flow highlights: Signs of oversupply emerging

- Aug 19, 2021 WTI’s structural weakness despite Atlantic Basin strength

- Aug 18, 2021 Low crude import allocations fit well with dismal China oil picture

- Aug 17, 2021 Physical Reality Check: Gasoline vs diesel: will the fortunes turn?