Is the surge in Atlantic MR freight rates sustainable?

How CPP dynamics has shaped the MR freight market on the Atlantic as well as what is in store for the region in the short to medium term?

Resuming from last week’s theme, attention is shifted on how product dynamics has shaped the MR freight market on the Atlantic Basin as well as what is in store for the region in the short to medium term.

Strong US demand resurrects Atlantic rates

The Atlantic freight market shows a completely different picture from the one that was witnessed a month ago. TC2 rates have reached a 12-month high, rising around 20% from 30 days ago. Demand for products globally but especially in the US remains strong, reflected by the low levels of inventories as well as healthy product cracks.

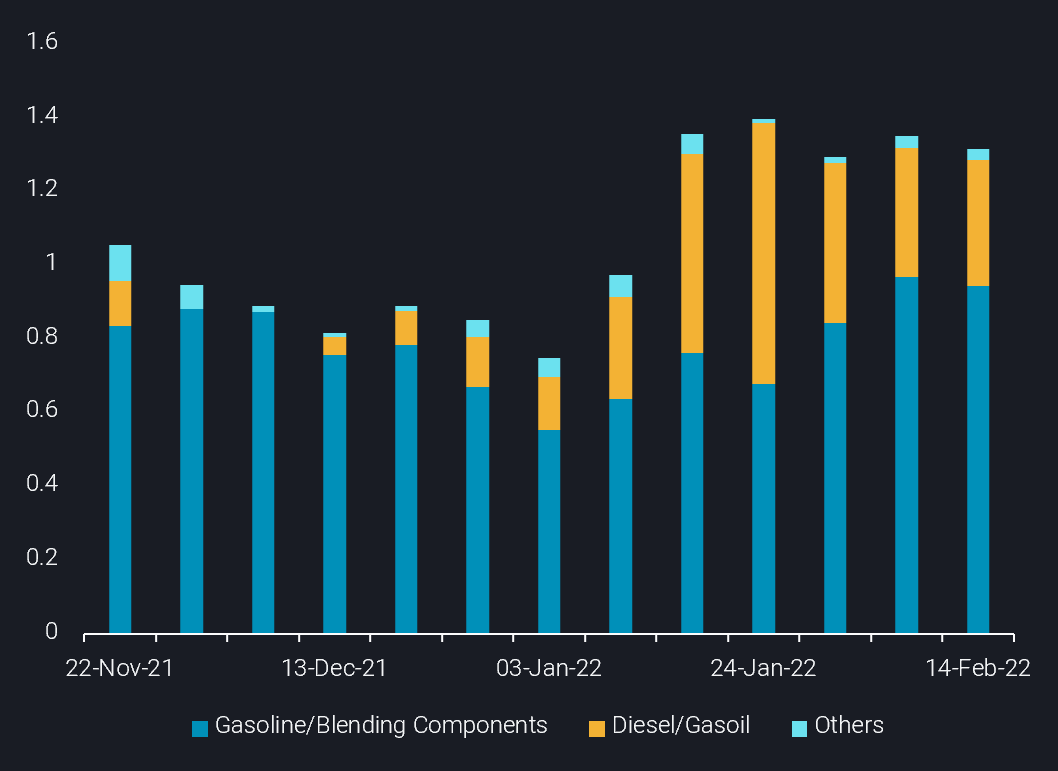

MR Tonne-miles for Europe – USG route by product (bn tonne-miles)

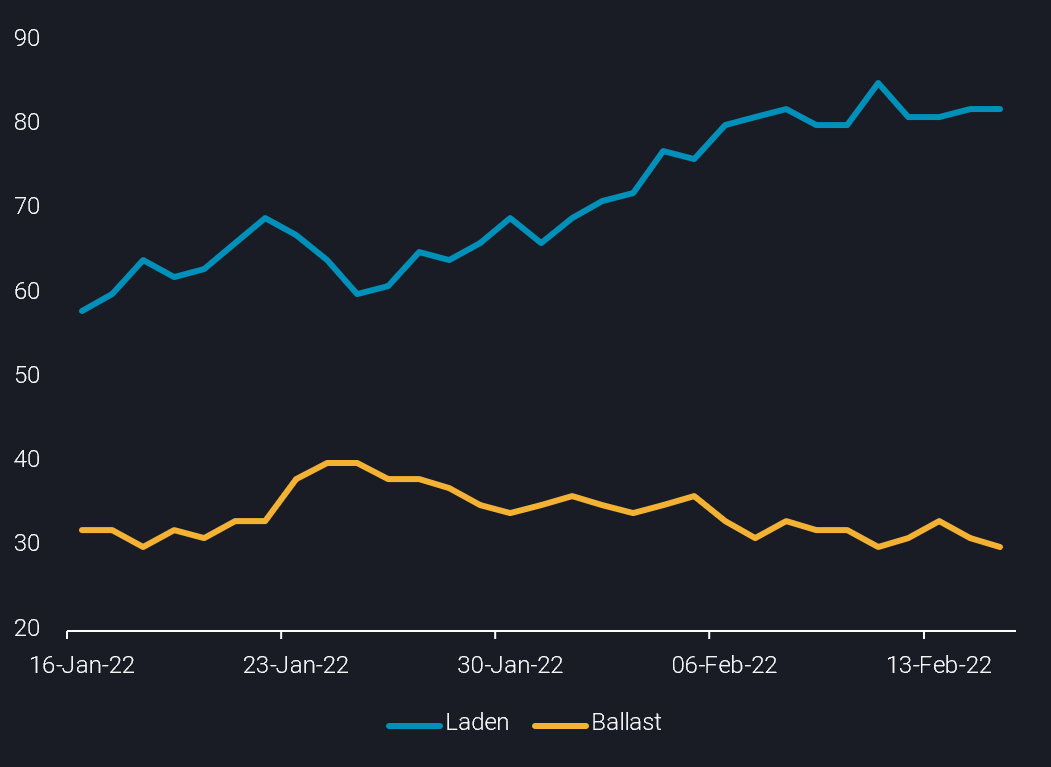

Rates were propelled by both diesel and gasoline cargoes sourced from Europe, which boosted tanker employment. The fleet distribution in Europe was also hinting at a tighter vessel supply prior to the pick up on rates as the number of laden vessels was increasing on the expense of the ballast vessels since the last week of January, as illustrated in the graph below.

MRs originating from UK Cont by status (no. of vessels)

This development has attracted more MRs on the Europe-to-US route, subsequently thinning the vessel tonnage list on other trademark Atlantic routes operating like the TC14 (US-to-Europe) as well as TC18 (USG-to-LatAm). Simultaneously, the tanker demand side was also supportive, as PADD 3 gasoline exports are on the rise for February m-o-m, according to preliminary data on the back of strong LatAm demand. These routes eventually experienced around a 15% freight rate increase since the start of the year.

Product supply constraints dim outlook for MRs

Looking forward, there are several factors at play which will shape the landscape of Atlantic Basin MRs. It is worth starting with a look at freight markets neighbouring the Atlantic, such as the Baltic-UKC. Freight rates for this route are hovering around 21-month highs keeping owners in intra-regional operations. This is also reflected by the higher y-o-y intra-European employment levels of Handysize and MR tankers, which suggest that MRs operating in that region will refrain from shifting towards the Atlantic Basin.

A concern for shipowners is coming from the US refining sector, as a heavy refinery maintenance schedule in PADD 3 is under way. This is not only likely to limit CPP volumes out of the Gulf but may also direct a portion of MRs operating on the affected routes, TC14 and TC18, towards the other side of the pond, thus adding to vessel supply on the TC2 route. Moreover, despite the fact that product demand in the US is poised to remain strong, this might not be matched from the supply side. A mix of refining maintenance, a temporary easing of diesel demand after peak winter, demand destruction risks, and a challenging operational environment could all join forces to hamper European product outflows, speaking against a sustained TC2 rise.

But a poorly supplied Atlantic market may also create opportunities, even if only brief ones. Imports towards the Caribbean, including shipments for storage purposes, have increased over the last year, as indicated from the rising number of MRs signaling towards this destination. The region can possibly contribute to satisfy the demand from neighbouring markets such as USG and LATAM. This however could only occur partially as the quantities stored in the region would not be able to completely replace European or US barrels. Nevertheless the Caribbean can provide some cargo demand for the market, adding a bit to CPP tanker tonnage.

Finally, looking at vessel deliveries, the situation looks discouraging for shipowners. 25 MR/Handysize vessels are expected to hit the water in Q2 2022 according to data from ACM Braemar (6% higher than the quarterly average of 2021). The issue here for the shipowners is that the East of Suez product market is equally limited in supplies as the West, as China’s product exports remain subdued. This generates doubts on whether the region can absorb a considerable share of this incoming tonnage.

All in all, while product demand is evident, a multitude of regional and worldwide factors point towards a limited supply-side which hampers trade demand. This will make vessel owners in the Atlantic competing for a smaller amount of cargoes, thus leaving a limited potential for any freight rate upside during the spring period. The silver lining is that this environment of persistent supply shortages and strong demand, rare opportunities and trade patterns could emerge briefly – like the one in the Caribbean region or to the US Atlantic Coast – which could provide support for rates.

More from Vortexa Analysis

- Feb 16, 2022 Supply is driving the Atlantic Basin gasoline market tightness

- Feb 15, 2022 Global refining industry struggles to stem growing market tightness

- Feb 10, 2022 Global sweet crude exports edge higher in January

- Feb 9, 2022 How much further will global crude inventories fall?

- Feb 8, 2022 How is Omicron impacting Asia’s oil demand so far?

- Feb 2, 2022 Can clean tanker markets benefit from surging diesel prices?

- Feb 1, 2022 Russian roulette being played out in Ukraine, leaving the gas market guessing

- Jan 27, 2022 Naphtha & LPG: Falling freight rates suggest flows will remain curtailed

- Jan 26, 2022 Reality check on Russian oil and gas sanctions

- Jan 25, 2022 China’s crude destocking pauses. Is it looking for a refill?

- Jan 20, 2022: Maiden Crude Tanker CPP Voyages: What happened and what to expect

- Jan 19, 2022: Oil price rally is driven by lack of supply right now

- Jan 18, 2022: Global diesel market pricing in tighter supplies ahead