European refiners can live without Russian Urals

In this insight we examine the pros and cons of some key grades that could see/are seeing a boost in demand as European buyers shy away from Russian crude.

European importers of Russian crude face big challenges if they want to continue buying Urals crude or refined products. And a growing number of European companies across the energy and shipping sectors are making statements of intent to reduce or halt exposure to Russian oil and/or shipping. But in doing so, what are the substitutes?

From the perspective of the European crude market, the substitution of Russian cargoes is already underway. Russian Urals – the flagship grade for exports – have dropped sharply in value as limited interest from European buyers has driven the grade’s discount to North Sea Dated to record levels (Argus Media).

With European buyers shying away from Urals, we examine the pros and cons of some key grades that could see/are seeing a boost in demand in the coming weeks or months.

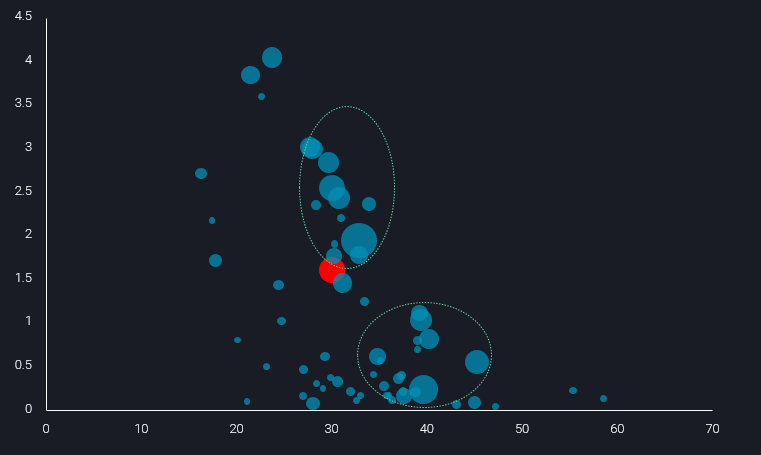

Unique Urals

Urals occupies a unique position in European crude supply, given its physical characteristics (API and sulphur content), load/delivery location (Baltic Sea, Black Sea, pipeline) and production volume.

Global crude grades API (x-axis) vs Sulphur (y-axis, %) vs seaborne exports (bubble size) – Urals in red

Given all these factors it is a tough challenge for a European refiner to find a good substitute for Urals. In reality, a stop of Urals flows to Europe will drive buyers to seek a variety of grades, from numerous locations and in varying amounts. The following grades are likely to be included in such considerations.

Johan Sverdrup

- + Production is stable and growing

- + Location is primed for the European market

- + Very low in sulphur

- +/- Lower gasoline yield benefits some but not all buyers

- – Would have to compete with Chinese buyers for cargoes

- – Most of the European imports of Johan Sverdrup have discharged in Netherlands or Turkey, suggesting that it would be a new crude for many refiners in the region

Azeri Light

- + Stable production, already regularly imported in the Med

- + Attractive pricing – diffs to north sea crudes have widened recently (Argus media)

- – Already over 80% of Azeri light goes to Europe, therefore not much room to go higher

WTI

- + One of the fastest growing seaborne crude streams as of now

- + Low sulphur makes it relatively cheap to process

- + Europe in a relatively good position/location to take prompt cargoes, limited VLCC export infrastructure in PADD 3 benefits European Aframax cargo buyers

- – Lower middle distillate yield than Urals

Mars

- + Exports have resumed after disappearing in October but only to about 100-250 kbd

- +/- Close in density but higher in sulphur than Urals

- +/- Close to 90% of seaborne exports head toward Asian markets on VLCCs, i.e. South Korea, China and India – though the latter two may purchase more Urals

- – Would be competing with US refiners that are seeking medium sour crudes, at a time where they are pivoting away from taking Russian crude and dirty feedstocks (Fuel Oil/VGO)

Es Sider

- + Very close proximity to Mediterranean refiners

- + Very low sulfur content will be viewed favourably by refiners

- + Yields a good amount of middle distillates and gasoline

- – 80% of Es Sider exports already head towards Europe, so not much upside for incremental flows

West African grades – Key grades include Forcados, Qua Iboe

- + Foracdos exports to Europe – the most popular West African stream in Europe hit a 28- month high in February.

- + Over 50% of West Africa’s exports head to Asia so there is upside potential for more European imports

- + Relatively close to Europe compared to Middle East

- + Low sulphur content

- – Reliability in production and export schedules is a long running concern among buyers

Basrah Medium

- + Large production base

- + Relatively cheap and may become cheaper if key buyers (e.g. India?) prefer to recieve cheaper Urals without the same fear or risk of sanctions impact

- +/- Lower gasoline yield benefits some but not all buyers

- – Relatively high transport costs, i.e. bringing a VLCC from the Middle East to Europe – many European buyers may prefer Afra/Suez, though Med buyers could pick up cargoes via Sumed pipeline (Sidi Kerir)

- – Export volumes could be threatened by the recent production declines (approx 480kbd) due to ongoing field maintenance and disruption from protests

- – High sulphur content amid spiking hydrogen/desulphurisation costs

Arab Light (/Medium?)

- + Largest production base, Saudi Arabia probably most capable of adding more oil to the market

- + Similar API to Urals

- + Most cargoes go to Asia (over 70%), suggesting some leeway to shift supplies to the European market

- – Very high sulphur content, not ideal if gas prices remain high

Oman Blend

- + Probably the most similar grade to Urals, on the basis of API and sulphur, which has large seaborne exports (900kbd)

- + The grade can be purchased via physically deliverable futures (DME), making it theoretically easier to source prompt cargoes

- – Almost always heads to Asia, so would require main buyers (China, and to a lesser extent India) to trim purchasing

Iranian Light/Heavy

- + A sizable chunk of supply (potentially up to 1mbd) could be added to the market relatively quickly, if there is a change in sanctions

- + Quality is quite similar to Urals, only marginally higher in sulphur

- + Mediterranean refiners were historical buyers, so there is some familiarity with it in refining setup

- – Highly speculative if/how quickly any European buyers would load or be willing to recieve cargoes

Having outlined the pros and cons of a few grades, it’s clear that no single grade perfectly fits the bill as a direct replacement. However it is important to note that both Northwest European and Mediterranean refiners are on the whole less reliant on Urals now than they were pre-pandemic.

In February, Urals accounted for around 8% of all crude arrivals into Northwest Europe and the Mediterranean (combined), down from a peak of around 14% in June-July 2019.

While there is a higher reliance upon Urals by northwest European refiners than in the Mediterranean, for both regions the trend is pointing lower m-o-m in February (see chart). This underlines the case made in our previous insight that for Europe, the impact of Russian sanctions would be far higher for diesel supplies than crude.

NWE, Med seaborne imports of Urals and Siberian Light (mbd) vs share of total arrivals (%, RHS)

More from Vortexa Analysis

- Mar 1, 2022 New world order = new oil trade order?

- Feb 24, 2022 Light-sweet crude prices soar amid Europe’s thirst

- Feb 23, 2022 European diesel market stuck in tightness

- Feb 21, 2022 Is the surge in Atlantic MR freight rates sustainable?

- Feb 16, 2022 Supply is driving the Atlantic Basin gasoline market tightness

- Feb 15, 2022 Global refining industry struggles to stem growing market tightness

- Feb 10, 2022 Global sweet crude exports edge higher in January

- Feb 9, 2022 How much further will global crude inventories fall?

- Feb 8, 2022 How is Omicron impacting Asia’s oil demand so far?

- Feb 2, 2022 Can clean tanker markets benefit from surging diesel prices?

- Feb 1, 2022 Russian roulette being played out in Ukraine, leaving the gas market guessing

- Jan 27, 2022 Naphtha & LPG: Falling freight rates suggest flows will remain curtailed

- Jan 26, 2022 Reality check on Russian oil and gas sanctions

- Jan 25, 2022 China’s crude destocking pauses. Is it looking for a refill?

- Jan 20, 2022: Maiden Crude Tanker CPP Voyages: What happened and what to expect