LR2s keep “cleaning” up throughout 2021

What are the dynamics behind this dirty-to-clean shift and what is the impact on the product and crude tanker markets?

14 July, 2021

What are the dynamics behind this dirty-to-clean shift and what is the impact on the product and crude tanker markets?

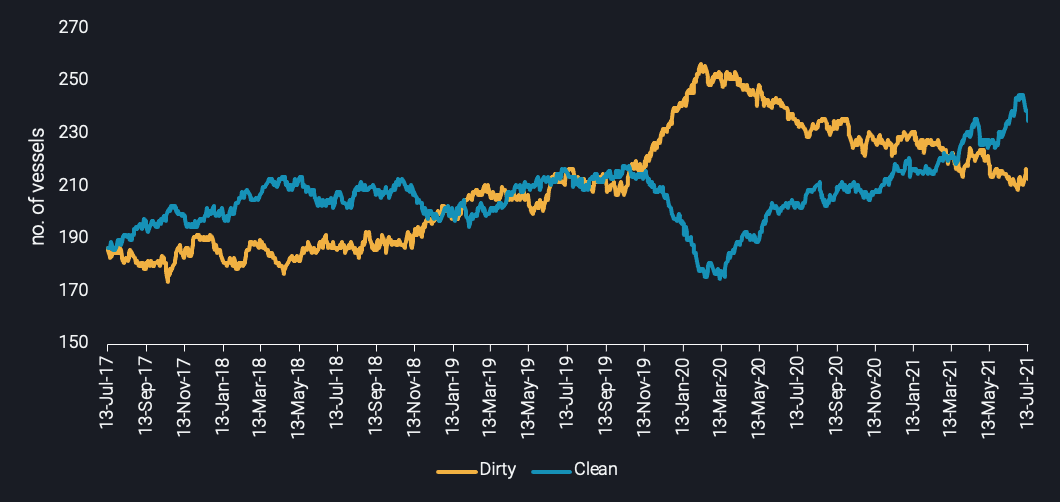

- Since Q2 2020, LR2 vessels have steadily shifted towards the CPP trade, eventually overtaking the amount of LR2 tankers trading in the “dirty” market at the end of Q1 2021.

- The shift is poised to have an upward impact on tanker rates by alleviating the Aframax supply-side, at a time where LR2 demand is on the path for recovery and can equalise an increase in tonnage.

LR2 tankers trading CPP vs trading Crude/DPP (no. of vessels)

- The initial phase of the shift towards clean products trading, in Q2 2020, was driven by economics – the spread between earnings on the benchmark LR2 (clean) Middle East-Far East route and average earnings for Aframax tankers globally (dirty) was assessed at a record $50,000/day in April and May 2020, according to shipbroker Braemar ACM.

- But since then, clean-dirty earnings spread has narrowed to less than $1,000/day, though LR2 earnings are still consistently outperforming their dirty counterparties. Even at the much narrower premium for clean tanker earnings, shipowners are still converting some of their remaining dirty fleet into clean trade.

- Utilisation of LR2 tankers has been gradually increasing since the last quarter of 2020, driven by firmer trade demand. Strong petrochemical demand from Japan and South Korea spurred naphtha flows mainly from the Mediterranean and the Middle East. This development boosted tonne-miles for LR2s towards the two Far Eastern countries, by 25% q-o-q.

- As a result, utilisation has climbed to record-highs of 134 vessels in Q2 2021, matching numbers last seen in Q2 2020. The key difference to last year being that elevated utilisation was previously sparked by a floating storage rush.

Global LR2 tanker tonne-miles (bn tonne-miles) vs. LR2 utilisation (no. of vessels – RHS)

- The switch to clean trading for LR2 tankers comes under the backdrop of utilisation rates remaining below 50%, while earnings for the majority of Aframax-dominated routes have remained in negative territory, according to Braemar ACM.

- Looking ahead, the uptake of LR2 tankers in clean trades is poised to continue. Firm naphtha prices underpin the resumption of strong demand stemming from the petrochemical industry in Asia. This development will continue to support utilisation of LR2 tankers, offsetting any prospective additional tonnage.

- At the same time, a decreasing number of LR2 tankers competing along with Aframaxes for dirty product or crude voyages, will relieve the pressure on the supply-side in that market which can ultimately contribute to lifting Aframax tanker freight rates.

- In other words, the continued shift of LR2 tankers from dirty to clean product trades could prove to be a win for owners with large exposure to Aframax and LR2 tankers.

Click here to register for a trial of Vortexa Freight Analytics

More from Vortexa Analysis

- Jul 14, 2021 China’s oil market cools post new policy changes

- Jul 7, 2021 Illustrations of naphtha and gasoline strength

- Jul 1, 2021 Q2 2021: Freight Market Update

- Jun 29, 2021 Two truths – why OPEC+ is hesitant

- Jun 24, 2021 Surging diesel flows – a pull or a push?

- Jun 23, 2021 $100 barrel of crude: boon or bust for tanker markets?