OPEC+ decision: A zero-sum game for VLCCs

Is the OPEC+ output increase considered glad tidings or a false hope for the VLCC market?

Is the OPEC+ output increase considered glad tidings or a false hope for the VLCC market?

After initial tensions, OPEC+ managed to ink a deal to increase oil production by an additional 2mn b/d of oil until the end of 2021 – or 400,000 b/d each month. The news of OPEC bringing additional barrels sounds like music to the shipowners ears, especially for VLCC owners, who have seen their earnings in negative territory for a major part of 2021.

An increase in oil production could potentially translate into higher exports and in turn boost shipping demand. However, that will be true as long as this rise in production is met with the proportional demand from key consumption centres such as China. The following article will attempt to answer two key questions regarding the impact of OPEC’s oil output increase on freight:

- Is an increase in OPEC+ output a positive for VLCC tanker tonne-miles historically?

- Is the current freight supply environment prone to hinder or turbocharge a potential freight rate recovery?

Tonne-mile indications look ominous while China demand is frail

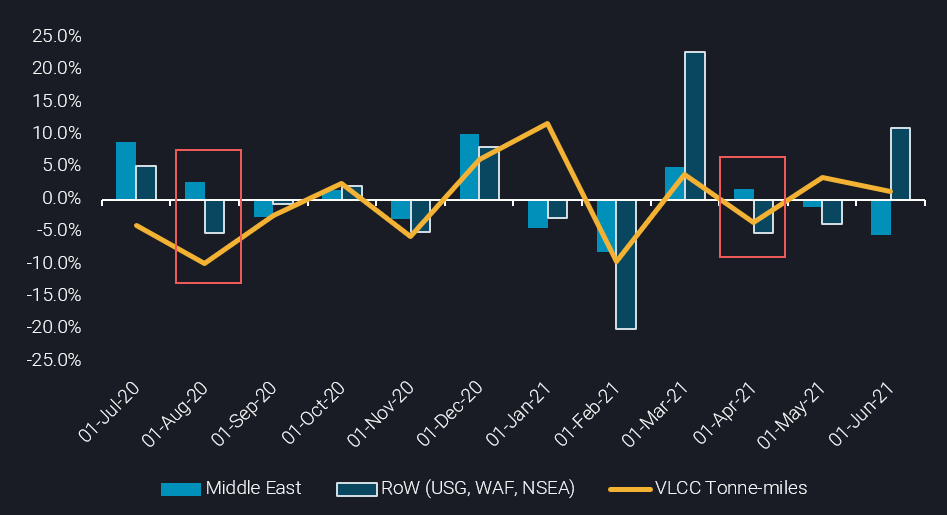

- At a first glance, by taking a look at the graph displayed below, the relationship between Middle Eastern exports and VLCC tonne-miles indicates a correlation for the majority of the timeframe. This at first gives the impression that an increase of the former boosts the latter.

- However, by adding more context it is evident that a correlation occurs only when exports from other traditional VLCC-originating markets such as the US Gulf, West Africa and North Sea are in sync with Middle Eastern flows.

- Yet limited Chinese crude appetite means that an increase in Middle Eastern exports could result in a drop of long-haul exports from other regions. Looking at the graph, it is evident that for the two occasions in the previous 12 months when Middle Eastern exports increased at the expense of the aforementioned regions, VLCC tonne-miles declined.

- The rationale behind this drop is that the distance traveled from the Middle East to China is smaller than for the other key VLCC routes. For most cases, travelling a shorter distance translates into shorter voyages and turnaround times for VLCCs, which in turn would trigger higher availability figures.

Monthly Change of Crude Exports from Selected regions vs VLCC tonne-miles (monthly % change)

Short-term supply growth outweighs demand

- To answer the second question, we first need to look at the impact of this oil production rise on VLCC demand. In a best case scenario, this 400,000 b/d monthly increase will be converted 100% to exports. If this is the case, an incremental demand of about 23 VLCCs would be created by the end of 2021.

- But what about the supply front? According to data from Braemar ACM, 11 newbuild VLCC tankers are expected to be added to the total fleet until the end of the year. To top it off, according to Vortexa, 13 VLCCs are currently employed for floating storage carrying either crude or DPP. Some of these vessels could potentially unwind their storage operations until the end of the year, ultimately largely neutralising any upside created from the incremental demand caused by the production lift.

Will scrapping come to the tanker’s market rescue?

- Any real chance for a VLCC market recovery hinges on a reduction on the supply side, that is an uptick of scrapping activity. Scrapping prices have been on a rally throughout the year, currently breaking the barrier of $580/t for tankers. Nevertheless, so far in 2021 only 4 VLCCs have been sent to the scrapyards.

- This has mostly to do with the fact that tanker secondhand prices are steaming hot, on the back of owners’ speculation for a prospective rebound of the tanker market, but also because older tonnage (15 years old +) is still attractive to perform shadow voyages from sanctioned countries at premium rates. In addition, uncertainty revolving around decarbonisation and related technological and regulatory aspects makes owners reluctant to invest in new tonnage, squeezing the economic life of the existing fleet.

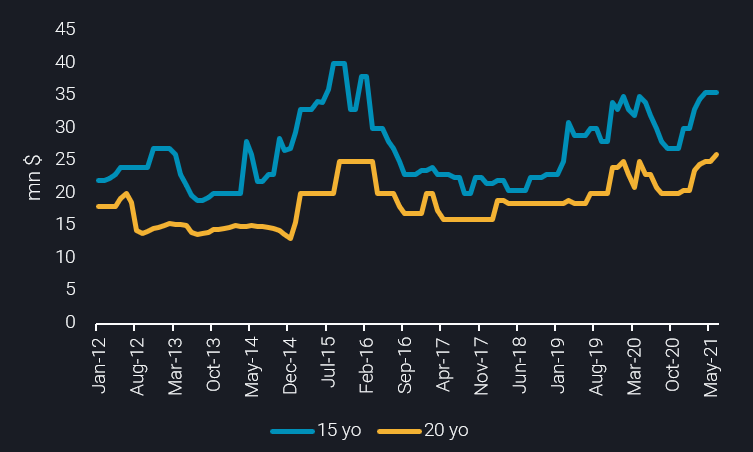

- Looking at the graph displayed below, 15-yo and 25-yo VLCC prices have been on an upward trend since December 2020. More importantly, asset values for 20-yo VLCCs are currently at a 9-year high, according to the data provided by Braemar ACM.

15-years old and 20-years old VLCC asset values (Million USD- Braemar ACM)

Hence, for now this “wait and see” approach collectively adopted from shipowners and operators is currently the key reason leading to an increase in secondhand values and a paralysis of demolition volumes. At the same time it is a key obstacle to any upside for freight rates in a market that is still far off pre-Covid demand levels. As things stand now, unless the US decides to remove sanctions from Iran, making the utilisation of older tonnage less attractive, a prompt and sizeable recovery looks like an improbable scenario.

Click here to register for a trial of Vortexa Freight Analytics

More from Vortexa Analysis

- Jul 21, 2021 Diesel remains surplus product in dire search for outlets around the globe

- Jul 20, 2021 Oil markets reality check: Seesaw between supply & demand disappointments

- Jul 15, 2021 High crude prices a double-edged sword for HSFO

- Jul 15, 2021 Middle East crude export surge – but for how long?

- Jul 14, 2021 China’s oil market cools post new policy changes

- Jul 7, 2021 Illustrations of naphtha and gasoline strength