Diesel remains surplus product in dire search for outlets around the globe

As global diesel loadings rise amid lagging demand, we explore how the supportive factors in the physical diesel market are not enough to withstand the pressure of a product in oversupply.

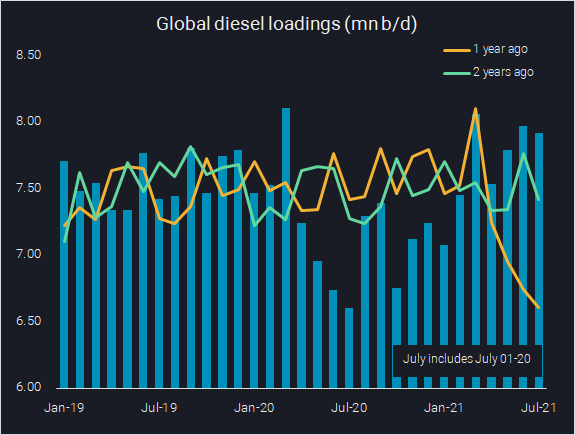

Global seaborne diesel flows are continuing their steady rise observed over the last five quarters and global diesel cracks are feeling the pressure. We could even be in for an all-time high above 8mn b/d in July (excl. intra-country flows), and are set to see the third month in a row above the respective 2019 level.

Not enough outlets

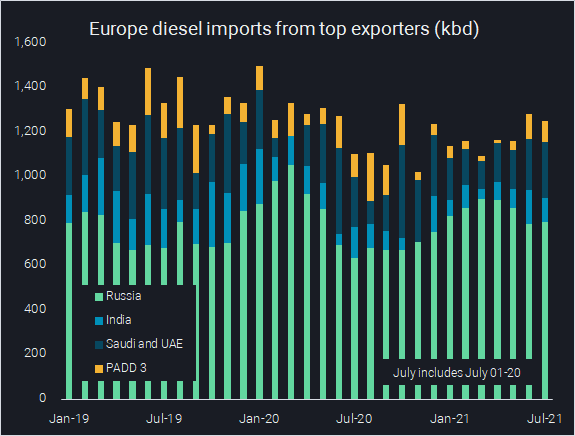

Despite some supportive physical factors, such as fewer Russian diesel imports into Europe, low European refinery runs, and increased exports to West African and South America, Atlantic Basin diesel margins are struggling. European diesel demand stays below pre-pandemic levels and middle distillate stocks continue to build. Jet and diesel imports into the ARA region are already set to reach a 9-month high on a b/d basis over July 1-20 and will likely continue to climb as it serves as a global outlet for excess barrels.

And even as refineries adjust to poor middle distillate margins and optimise higher performing products such as gasoline and naphtha, diesel continues to make up the largest percentage of the clean products seaborne barrel which has given way to the current contango structure, a sharp contrast to the other clean products.

In addition to the already oversupplied seaborne diesel exports, Asia and the Middle East lockdowns are further exacerbating the problem by pushing unwanted barrels towards Europe. Excess barrels combined with a slow uptick in European demand have been the strongest contributors to diesel’s demise.

For now diesel surplus will continue

High seaborne diesel exports will continue to put downward pressure on global diesel cracks and also refining margins, likely holding some players in Europe and other places back from restarting units or maximising runs. At the same time, rising seaborne imports of crude to Europe suggest higher refinery runs, while the recent surge in PADD 3 diesel exports to Latin America is reflective of increased runs and comparatively weak pricing in the Gulf Coast. The sustainability of these trends is questionable. The bigger picture is that until demand comes back in Southeast Asia and more consistently across the globe, the diesel outlook remains poor.

Click here to register for a trial of Vortexa Freight Analytics

More from Vortexa Analysis

- Jul 15, 2021 Middle East crude export surge-but for how long?

- Jul 14, 2021 LR2s keep “cleaning” up throughout 2021

- Jul 14, 2021 China’s oil market cools post new policy changes

- Jul 8, 2021 The curious case of declining VLGC rates – a blip or a trend?

- Jul 7, 2021 Illustrations of naphtha and gasoline strength

- Jul 1, 2021 Q2 2021: Freight Market Update

- Jun 29, 2021 Two truths – why OPEC+ is hesitant

- Jun 24, 2021 Surging diesel flows – a pull or a push?

- Jun 23, 2021 $100 barrel of crude: boon or bust for tanker markets?