Too many unknowns in “Zeitenwende”, but prices are set to rise

Oil prices are set to rise strongly, as Russian supplies to the market are getting delayed or cancelled down the line. We try to give an overview on crucial factors for rebalanced the market in unchartered territory.

The US and UK ban on imports of Russian oil are only the latest in a long chain of decisions that will keep parts of the 7.4mbd of seaborne Russian exports off the market, or at least delay deliveries significantly. With all the limitations on trading, shipping and financing, some gas stations may well run dry in the coming weeks or months. We are in unchartered territory, and prices will soon be there as well. In the following we try to bring some structure to relevant factors on the long way to rebalancing.

Three days after Russia’s invasion of Ukraine, the German chancellor Olaf Scholz held a widely noted speech in parliament, coining “Zeitenwende” as the word of the day. It means turning point in history or paradigm change. Within a couple of days, Germany had turned upside-down its stance on Russia, military spending, and deliveries of weapons into war zones, with adjustments on its nuclear and coal phase-out policies likely around the corner.

The overarching theme in the current reaction to the Ukraine war is something that has already been explored in the Covid-19 pandemic: income maximisation (GDP, sales) and cost minimisation (energy & resource spending) is not anymore the exclusive ultimate rationale. Human values, such as health and democracy, are guiding political and strategic decisions to a higher extent than in the past, with climate change and energy transition being a supportive game changer in the background.

Developments in Ukraine and the oil and gas markets are evidently extremely volatile, but most observers agree that the war action on the ground will likely be protracted. Two tail-end scenarios for a drastic change would be 1) WW III including the nuclear option, and 2) regime change in Russia. Otherwise, the market will remain challenged with digesting and replacing as much Russian supply as possible. The more it is the replacing rather than the digesting option, the higher prices will go.

Of course Russian supply is not the only variable when assessing the S/D balance and price patterns down the line. In fact it is fair to say that uncertainty about supply, demand, trading, and logistics has never been as high as right now, and that is across the barrel and all over the planet. So we are trying to briefly list key factors to watch out for in the following.

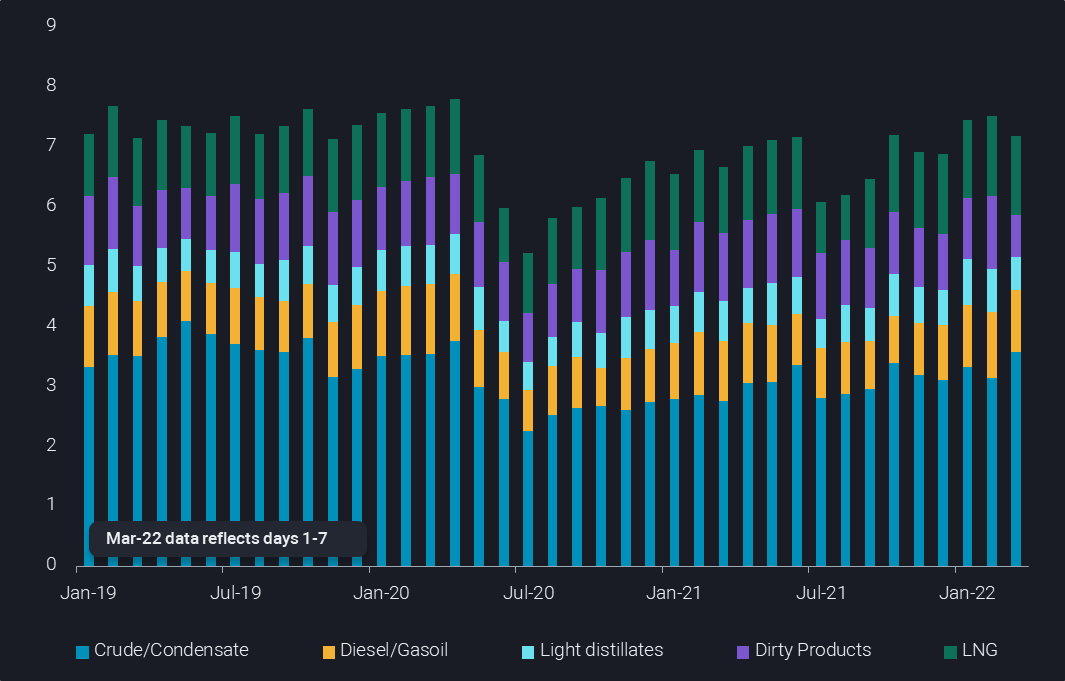

Russian oil and gas seaborne exports (mbd)

Supply:

- Russia: severe struggle to place any uncontracted barrels (crude, products, even LNG); the Putin regime is now also openly threatening with a shut-in of Nord Stream 1; 7.4mbd of crude oil and refined products seaborne exports are at stake, making up 10.4% global total (see chart)

- Iran: any deal may well be blocked by Russia, but market realities could allow Iran to resume exports, with up to 1mbd widely seen possible, albeit this figure is unlikely to be reached quickly

- Venezuela: US efforts are more about market psychology than a real chance for additional supplies (perhaps some re-routing to the US could take place)

- US shale: prices and policy push may help, but additional supply beyond base-case forecasts could well be limited to 200-400kbd over a 4-9 month frame

- OPEC: it remains to be seen how much additional supply will be made available – a big change is doubtful, when considered the largely stagnating export path since October

- Kazakhstan: up to 1.6mbd of CPC Blend at risk

Demand:

- Financial sanctions make it very difficult to trade cargoes and take care of logistics

- Spreading flow/vessel sanctions make deliveries to various countries impossible, with the US and the UK being the latest proponents

- Corporate demand curtailments: ever more players stop procuring Russian oil and gas on their own motivation (moral & social pressure)

- Without question there will be a fallout for global GDP growth and related demand destruction

- Also price-related demand destruction is set to come in, but likely in small steps

- Repercussions from a lack of natural gas, and related record pricing including electricity, make any substitutions unlikely, leaving efficiency and outright use as defining factors

- May final consumers show some voluntary restraints (especially driving, heating, aviation)?

System & timing questions:

- SPR releases may help but implementation is slow

- Delays in Russian shipments, full tanks and production fallout is increasingly likely

- Delays due to re-arrangement of global flows. Chinese and Indian buyers may come in ultimately, but apparently not very quickly

- Vessel speed could be cut due to bunker costs

- Credit line needs are soaring, but banks are very cautious

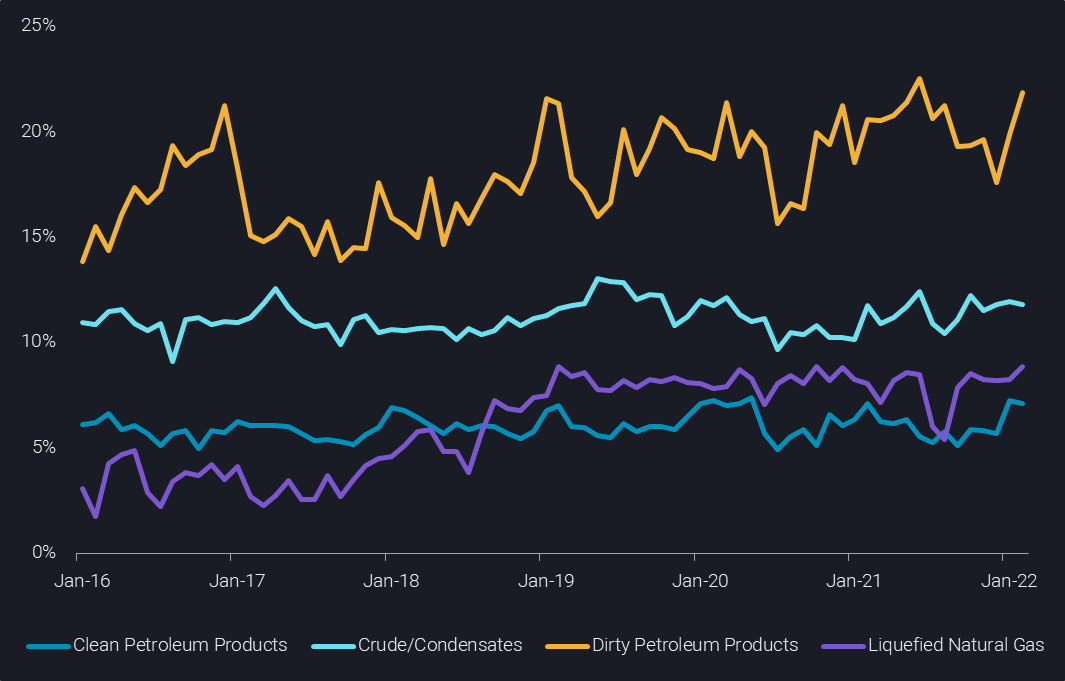

Share of Russian oil and gas exports in global seaborne oil and gas exports (%)

Trying to sum up everything in one paragraph: the oil and gas market was already very tight ahead of 24 February, with low stocks in crude, refined products and natural gas. While so far loadings at Russian ports are still taking place at normal rates, some of those cargoes already need to be redirected towards alternative offtakers. The market is now lacking close to two weeks of fresh deals, and sanctions/restrictions get tighter by the day. Alternative supplies as well as big repercussions on the demand side will only materialise over time and at a limited rate.

$200/b in sight as market is not anymore fully functioning

The market is simply not functioning anymore smoothly – with huge repercussions. Even Asian importers are struggling to place any new orders, and already the currently caused delays are likely to lead to actual physical supply shortages down the line. In spite of record refining margins, refiners are set to fail in crude or secondary feedstock procurement, with some of them bringing refinery maintenance forward. In this market environment, downstream players may simply give up on supplying the full market. At least temporarily and locally restricted, gas stations are likely to run out of gasoline and diesel over the coming weeks and months. The inability to sell oil will soon affect Russian output decisions, both upstream and downstream, if this is not already the case.

The demand destruction necessary down the line is easily big enough to have oil prices surpassing $200/b. Then the question is how quickly opportunistic buyers will show up, whether governments and corporations will reconsider sanctions, and what happened to the war parties in the meantime. This and all the other S/D reactions will define the inflection point and the persistency of record pricing, all of which appears impossible to forecast at this point in time.

More from Vortexa Analysis

- Mar 3, 2022 What would a reshuffle in flows mean for tanker demand?

- Mar 2, 2022 European refiners can live without Russian Urals

- Mar 1, 2022 New world order = new oil trade order?

- Feb 24, 2022 Light-sweet crude prices soar amid Europe’s thirst

- Feb 23, 2022 European diesel market stuck in tightness

- Feb 21, 2022 Is the surge in Atlantic MR freight rates sustainable?

- Feb 16, 2022 Supply is driving the Atlantic Basin gasoline market tightness

- Feb 15, 2022 Global refining industry struggles to stem growing market tightness

- Feb 10, 2022 Global sweet crude exports edge higher in January

- Feb 9, 2022 How much further will global crude inventories fall?

- Feb 8, 2022 How is Omicron impacting Asia’s oil demand so far?

- Feb 2, 2022 Can clean tanker markets benefit from surging diesel prices?

- Feb 1, 2022 Russian roulette being played out in Ukraine, leaving the gas market guessing