Q2 2021: Freight Market Update

Vortexa summarises the trends and dynamics that prevailed in the crude and product tanker market throughout Q2 2021.

At the end of last year we sought to identify the main trends that will shape the 2021 freight markets. Firstly we urged market participants to follow floating storage as the main balancing factor for freight markets with persistent oversupply carried into the new year. Furthermore, we decided to keep an eye on Chinese imports of crude oil as the main contributor to tanker tonne-miles in this market segment. When it comes to clean petroleum products (CPP) markets, we were hopeful this would be the tanker market bright spot, as refinery outages and closures would spur volumes of oil-on-water, boosting tonne-miles and utilisation. Throughout Q2, activity in freight markets overall remained tepid as market participants geared for an expected pick up in 2H 2021.

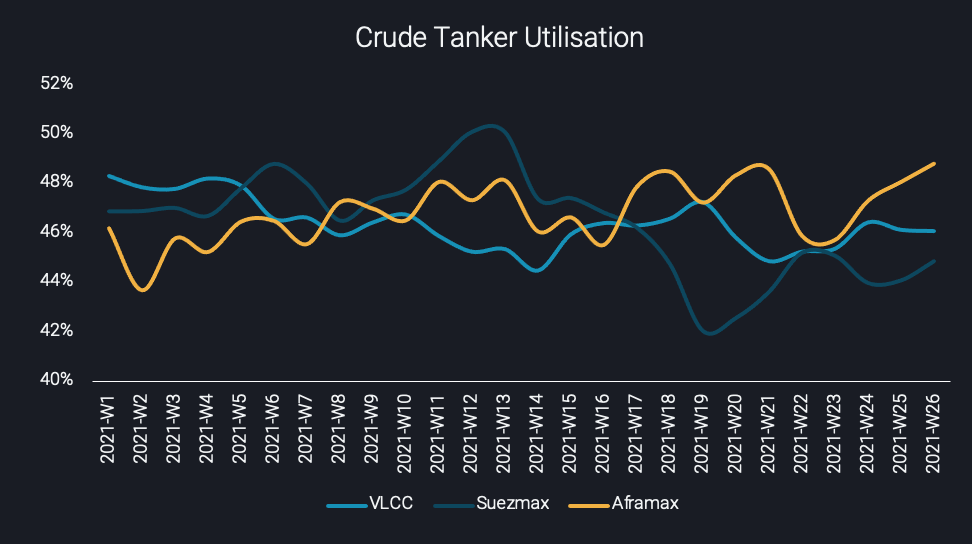

Crude tanker utilisation: The good, the bad and the stable

Looking at the big picture using Vortexa freight analytics, the development of utilisation for the main crude tanker segments for the first half of 2021 does not indicate any significant change that could signal a long-anticipated recovery. However, it does display three distinct patterns.

Starting with VLCCs, utilisation has remained relatively stable, indicating a mere 2% decrease on a quarterly basis. This can be explained by examining the two key routes that propel the VLCC trade: Middle East – Far East and West Africa to Far East. Tonne-days demand for these routes remains flat throughout Q2 2021, but is marginally underperforming when compared to Q1.

The Suezmax tanker class suffered the greatest q-o-q decrease in employment, when compared to its counterparts. The decline is estimated at 5% and commenced at the start of the quarter following tighter supply and demand fundamentals at the end of March.

Conversely, Aframax tanker utilisation fared the best, displaying an upwards trend since the start of the year. This trend is more distinctive throughout June, on the back of a tighter European market on the vessel supply side.

Crude tanker utilisation per crude vessel class (%)

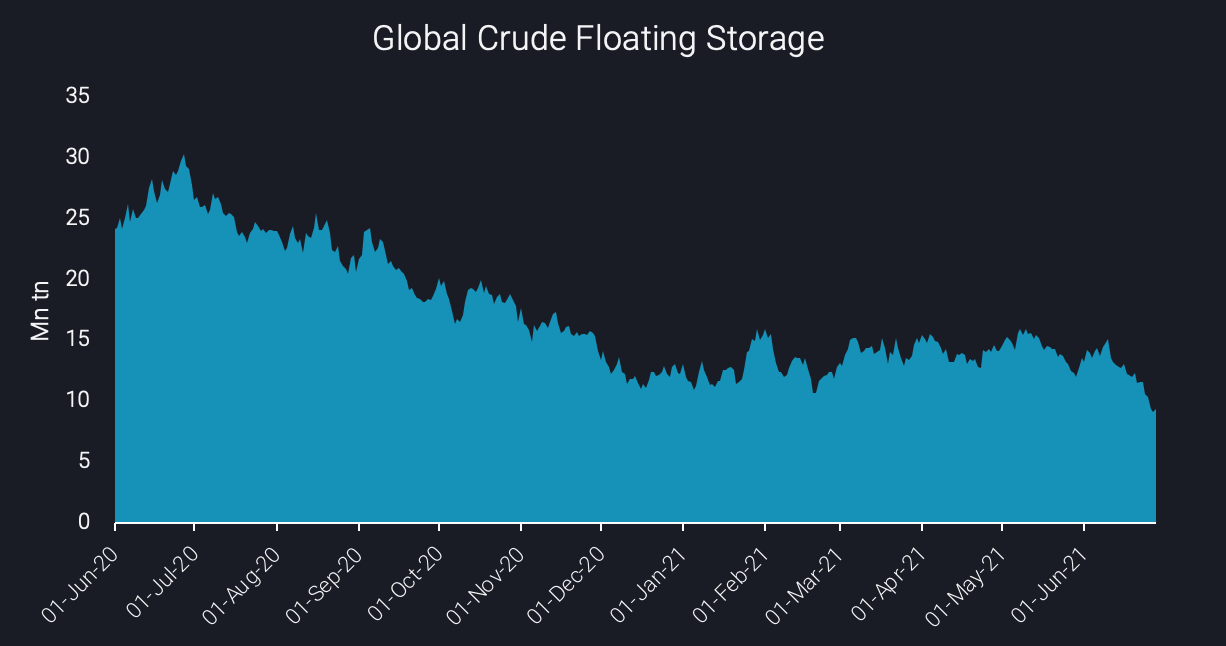

Global crude floating storage: from all-time highs to normal lows within a year

A year ago, at the end of June 2020, crude floating storage volumes were at all-time highs after the first wave of the pandemic, hitting 30mn tonnes. Fast-forward to today, at the end of June 2021, floating storage has shrunk to around 9mn tonnes, having declined by 36% q-o-q.

This development is aligned with a significant increase in crude prices over Q2, a result of limited supplies from OPEC+ – with exports remaining disciplined around 23 mn bpd in 2021 – along with gradual stock draws to satisfy increasing demand. Hence, the currently backwardated pricing structure of crude oil does not provide an economic rationale for traders to store oil and rather makes any delays in shipping a costly exercise.

This gradual reduction in floating storage is not a welcome development from a shipowner perspective, as it adds further pressure to the tanker oversupply that currently plagues the dirty tanker market, keeping rates low.

Global crude floating storage (mn tonnes)

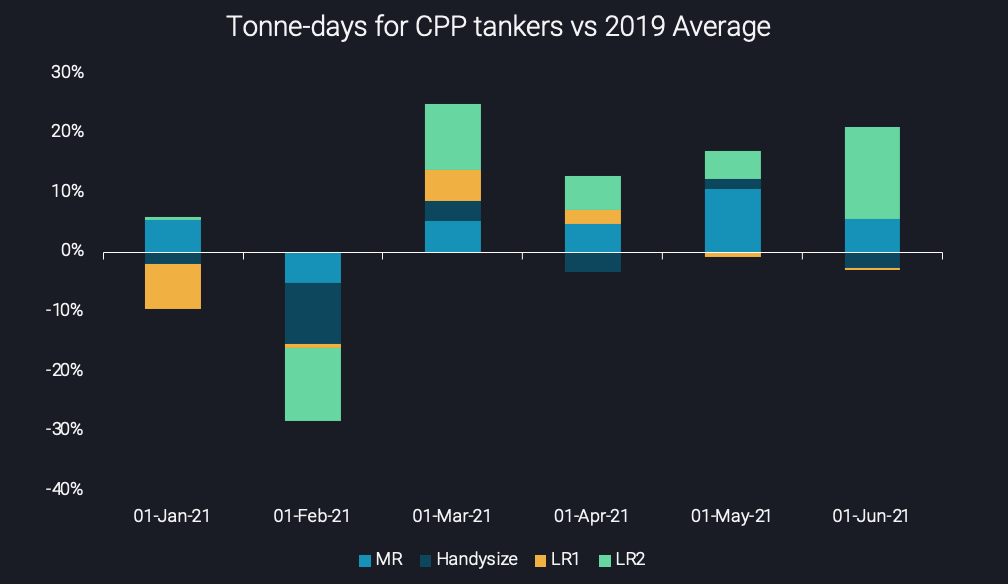

CPP tanker demand is improving as LR2 and MR tanker segments take the lead

The CPP tanker market has shown better performance. Overall tonne-days have improved from March onwards, when compared with the pre-pandemic period of 2019. The next chart shows that two tanker classes are displaying a consistent increase when compared to 2019 average levels: LR2 and MR tankers.

More specifically, LR2 tanker employment was supported by higher petrochemical demand and refinery maintenance schedules in Japan and South Korea. This development triggered a pull of naphtha cargoes carried from the Middle East but also from the Med and the Black Sea, leaving a positive impact on tonne-mile demand.

On the other hand, MR vessels were supported by the lifting of strict coronavirus measures in West of Suez markets, which in turn induced a stronger CPP demand in regions such as Europe and the Americas throughout Q2 2021.

Tonne-day demand for CPP tankers vs 2019 monthly average (% difference)

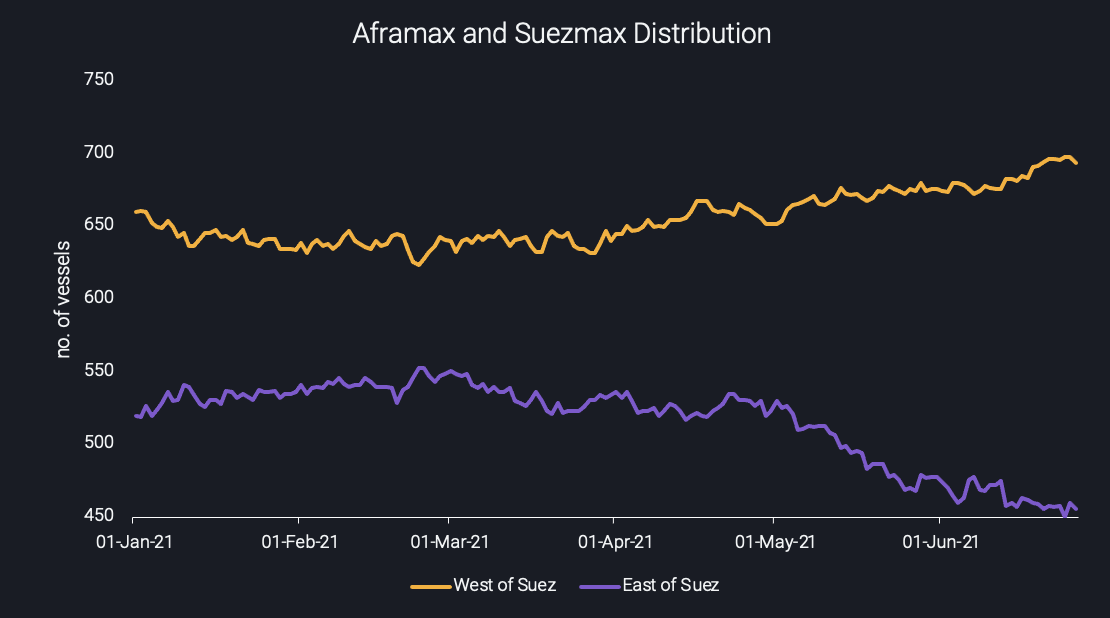

Aframax and Suezmax tankers are looking westwards for employment

From the start of Q2, an increasing divergence in activity is observed regarding Aframaxes and Suezmax tankers between West and East of Suez, as displayed in the graph below. This is a clear indication that an increasing number of tankers belonging to these classes is heading towards the West to seek employment.

Drilling deeper into Vortexa analytics, there is an evident imbalance in utilisation of tankers between the two areas throughout Q2. In the West, utilisation is usually hovering over 50%, while in contrast, in the East of Suez we see this consistently below 50%.

This divergence in fleet distribution is linked to the persistently strong crack spreads in the Atlantic Basin, which incentivised refineries to import higher levels of crude into the region. One the other hand, the weakness East of Suez is related to the lower margins on the back of surging Covid cases and a slowdown of crude imports from key markets such as China.

Aframax and Suezmax tanker distribution (no. of vessel)

Conclusion

Overall, the developments that unfolded in the East during Q2 curtailed crude trade towards the region, which ultimately forbid any increase in rates, particularly for VLCC and Suezmax tankers. On the other side of the globe, Western economies displayed increasingly healthier crude and product demand, which in turn drove Aframax and CPP tanker activity in the region.

Looking ahead towards Q3, demand in Asia is poised to recover, which in combination with a prospective increase in production from OPEC+ will potentially create a positive catalyst for freight. Nevertheless, as long as scrapping activity does not pick up to dent the supply side, a full-steam recovery seems an unlikely scenario.

Click here to register for a trial of Vortexa Freight Analytics

More from Vortexa Analysis

- Jun 29, 2021 Two truths – why OPEC+ is hesitant

- Jun 24, 2021 Surging diesel flows – a pull or a push?

- Jun 23, 2021 $100 barrel of crude: boon or bust for tanker markets?

- Jun 22, 2021 Global jet fuel recovery running late, US emerging as bright spot

- Jun 18, 2021 Crude markets diverging in Atlantic Basin

- Jun 16, 2021 Question marks for freight rates in a largely supportive global LNG picture